Learn more about CBO, its work, and its processes in an introduction to the agency that is typically updated at the start of each Congress or a new session.

Budget Concepts and Process

Report

ReportRescissions are provisions of law that cancel budget authority previously provided to federal agencies before it would otherwise expire. This document provides answers to key questions about how CBO estimates savings from rescissions.

-

Report

As defined by the Unfunded Mandates Reform Act of 1995, mandates generally require a nonfederal entity to take an action or comply with a prohibition. This primer describes the principles that CBO follows to identify mandates in legislation.

Report

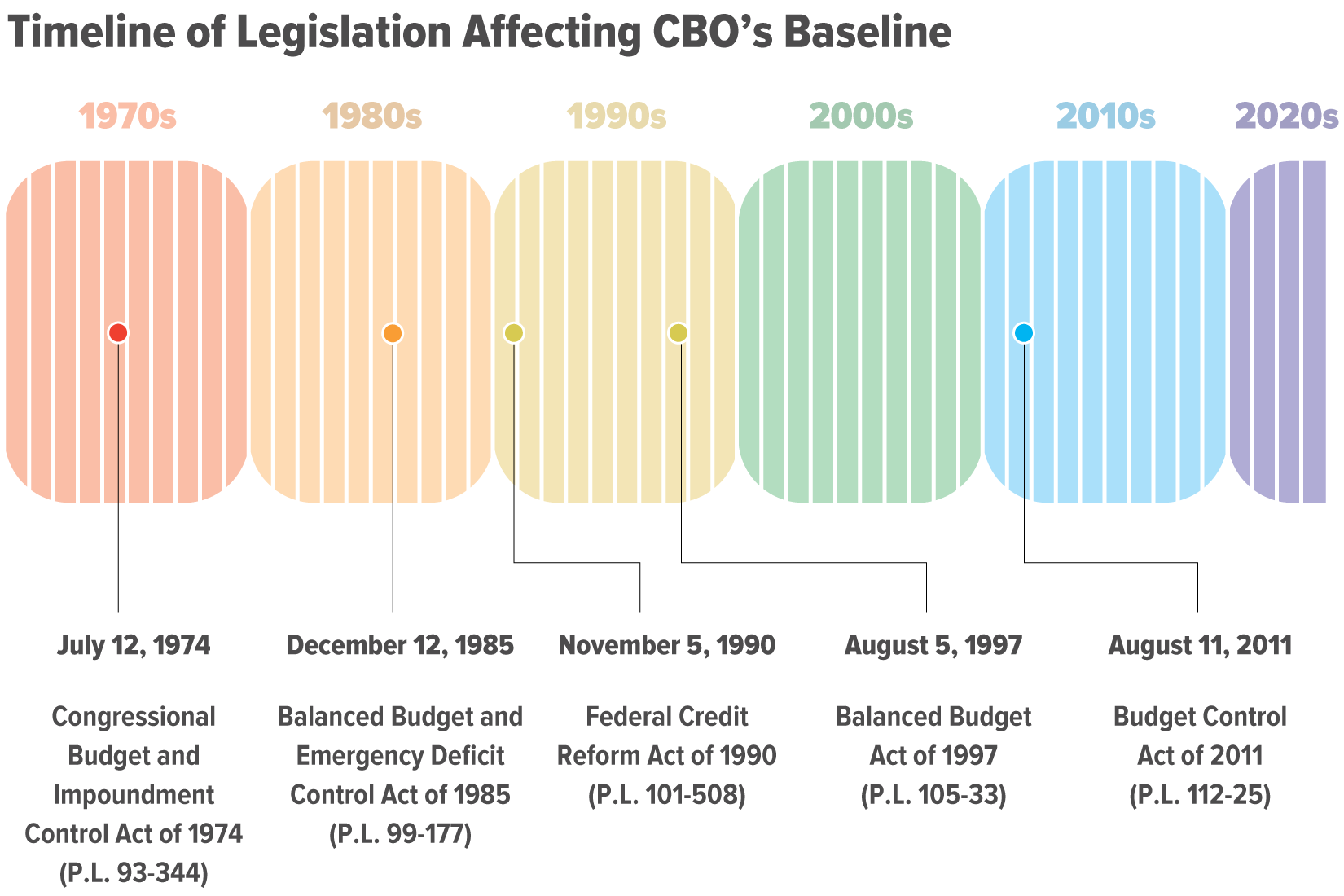

ReportCBO is required to regularly prepare a baseline consisting of projections of federal revenues, spending, deficits or surpluses, and debt under current law. This document describes the laws that govern how CBO prepares those projections.

Report

ReportCBO describes features of the Medicare and Medicaid improvement funds and how the funds are accounted for in CBO’s baseline and cost estimates.

Report

ReportThe Congressional Budget Act of 1974 requires CBO to prepare estimates of the cost of legislation at certain points in the legislative process. This document provides answers to questions about how CBO prepares those cost estimates.

Report

ReportThe Congressional Budget Act of 1974 requires CBO to produce an annual report on federal spending, revenues, and deficits or surpluses. This document provides answers to questions about how CBO prepares those baseline budget projections.

Report

ReportCBO examines trends in funding and spending for the Army Corps of Engineers and explains how CBO treats that agency’s activities in its baseline and cost estimates.

Report

ReportCBO examines trends in funding and spending for the Federal Emergency Management Agency's Disaster Relief Fund and provides information about how CBO treats that program in its baseline and cost estimates.

Report

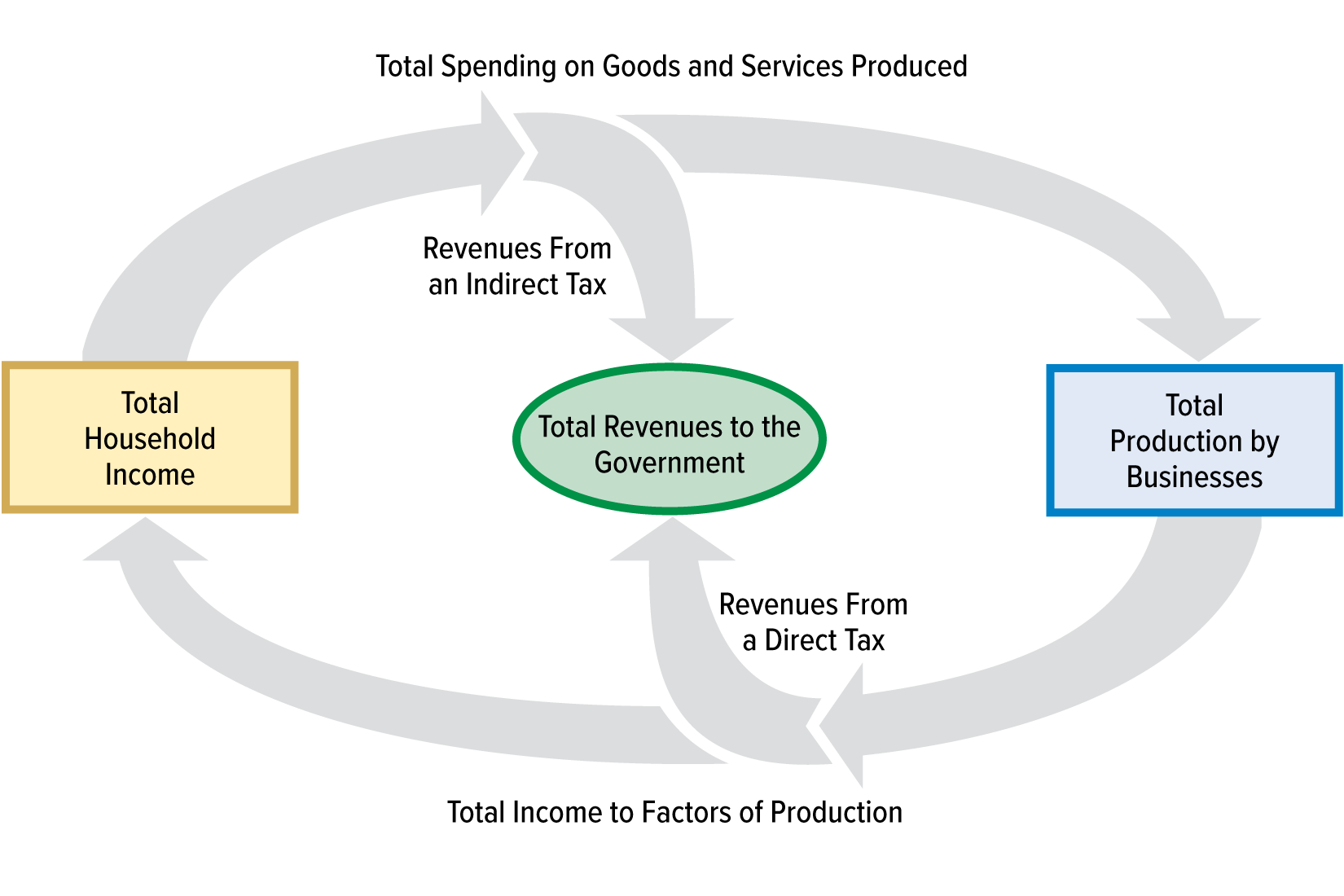

ReportCBO explains why it uses an income and payroll tax offset when estimating the budgetary effects of changes in indirect taxes, how the rate of the offset is set, and how it is applied in cost estimates and in baseline projections of revenues.

Report

ReportThis guide briefly explains—in plain language—the differences between some common budgetary terms.

Report

ReportCBO explains some of the guidelines it follows when providing information to the Congress about the budgetary effects of proposed legislation.

Report

ReportCBO describes how estimates of the budgetary effects of enacted legislation are recorded and used to meet requirements for budget enforcement under the Statutory Pay-As-You-Go Act of 2010.

Report

ReportFrom the end of 2008 to 2019, the amount of federal debt held by the public nearly tripled. This report describes federal debt, various ways to measure it, CBO’s projections for the coming decade, and the consequences of its growth.

Presentation

PresentationPresentation by Wendy Edelberg, an Associate Director for Economic Analysis at CBO, at the University of Chicago Booth School of Business