To assess the full costs of federal loans and loan guarantees, CBO has developed a method for estimating the present value of the lifetime administrative costs of certain federal credit programs.

Federal Credit Programs

Report

ReportCBO estimates the costs of federal credit programs in 2024 in two ways—following procedures prescribed by the Federal Credit Reform Act and using a fair-value approach, which measures the market value of the government’s obligations.

Report

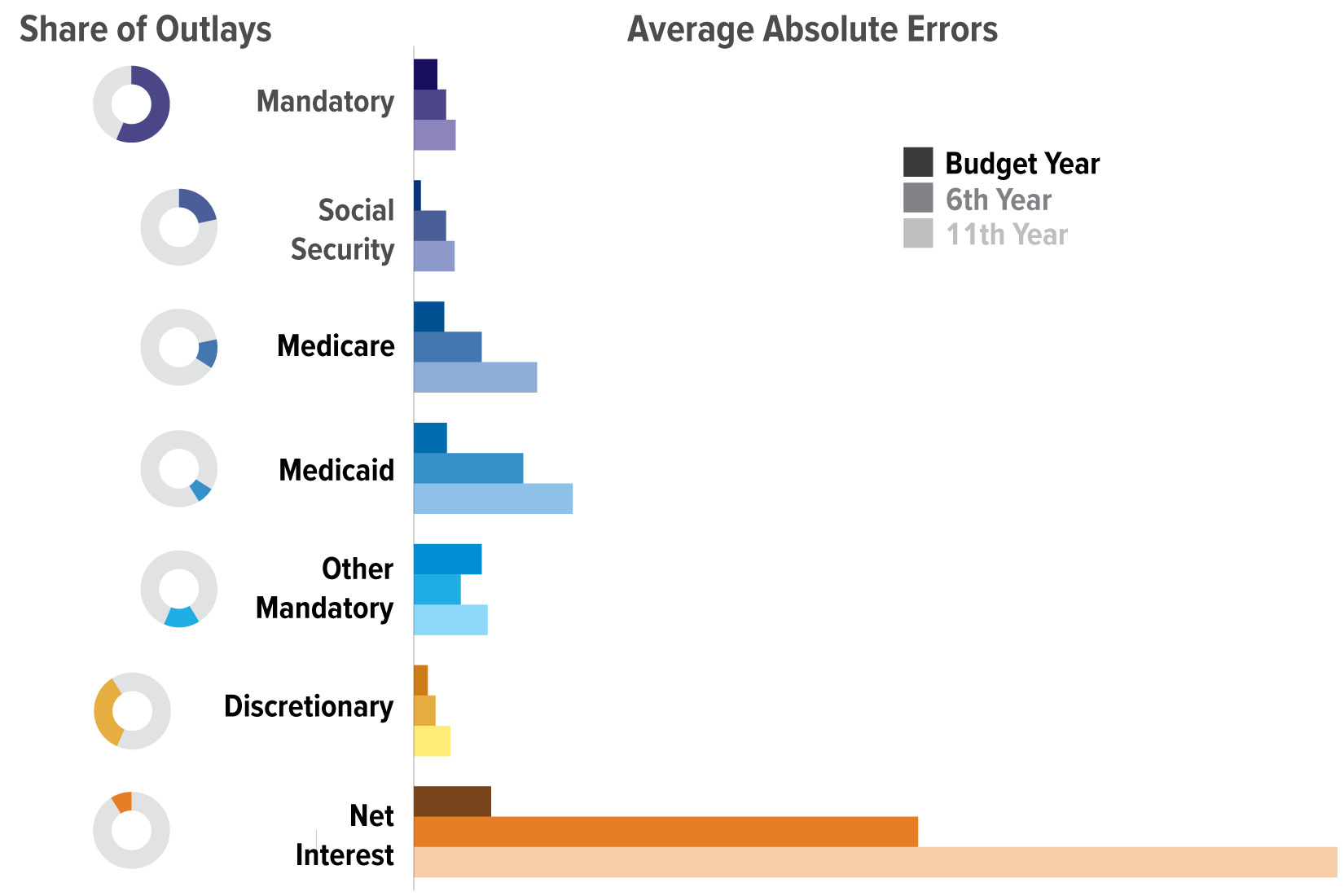

ReportIn this report, CBO uses various measures to assess the quality of its past projections of federal outlays. The analysis focuses on three fiscal years within each projection period: the budget year, the 6th year, and the 11th year.

Report

ReportCBO describes the commitments the federal government has made through its credit and insurance programs, including housing, real estate, and student loan programs, deposit insurance, insurance for private pensions, and flood and crop insurance.

Report

ReportCBO describes the Housing Trust Fund's and Capital Magnet Fund's income, spending, and budgetary impact, how their grants are used in the production of low-income housing, and how the funds compare with other support for affordable housing.

Report

ReportCBO describes the securitization programs of the Government National Mortgage Association (Ginnie Mae) and compares its baseline budget projections for Ginnie Mae with outcomes under a scenario of severe economic stress.

Report

ReportCBO describes VA’s mortgage guarantee program, provides estimates of the budgetary costs of the program, and compares those costs with expenditures for other federal guarantees.

Report

ReportThis report examines approaches to budgeting that would distinguish expenditures for investment in physical capital, education, and research and development from other expenditures.

-

Report

This report explains the details of two approaches to measuring the cost of government activities that involve financial risk, the qualitative differences between them, and their application to various activities and programs.

Report

ReportCBO examines how recapitalizing Fannie Mae and Freddie Mac through administrative actions would affect such factors as CBO’s budget projections and cash flows between the two enterprises and their shareholders, including the Treasury.

Report

ReportIn this primer, CBO discusses the methodological differences between the FCRA and fair-value approaches and how those differences affect estimates of the cost of federal credit programs.

Report

ReportWhat roles do cash and accrual measures play in the federal budget process? This report discusses the relative merits of those measures and explores the implications of expanding the use of accrual measures for decisionmaking purposes.

Report

ReportCBO reviews Fannie Mae and Freddie Mac’s program to transfer some of the credit risk of their guarantees to investors and analyzes two approaches for expanding those efforts.

Report

ReportCBO analyzes options to reduce FHA’s exposure to risk from its program to guarantee single-family mortgages, including creating a larger role for private lenders and restricting the availability of FHA’s guarantees.