Earlier this month, the Congressional Budget Office published The 2016 Long-Term Budget Outlook, describing the agency’s projections of federal spending, revenues, deficits, and debt over the next 30 years. Yesterday we highlighted key factors underlying the projected growth in spending for Social Security and the major health care programs. Today we’ll focus on interest costs.

The government’s net interest costs are projected to more than double as a share of the economy over the next decade—from 1.4 percent of GDP in 2016 to 3.0 percent by 2026. By 2046, if current laws governing taxes and spending generally did not change, those costs would reach 5.8 percent of GDP—increasing from 6 percent of federal spending to 21 percent over the next 30 years.

Net interest costs are projected to increase as interest rates rise from unusually low levels and as greater federal borrowing directly leads to greater debt-service costs. In addition, greater federal borrowing is projected to put further upward pressure on interest rates and thus on interest costs. Growth in net interest costs and growth in debt reinforce each other: Rising interest costs push up deficits and debt, and rising debt pushes up interest costs.

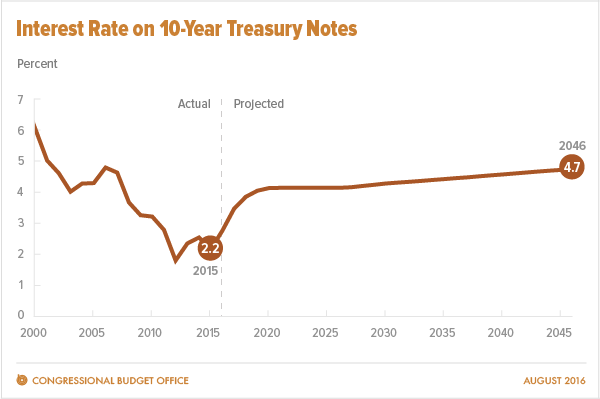

CBO projects that interest rates will rise from today’s low rates as the economy grows but that they still will be lower than they have been, on average, during the past few decades. Over the long term, interest rates are projected to rise to levels consistent with factors such as labor force growth, productivity growth, the demand for investment, and federal deficits. According to CBO’s projections, factors that push interest rates down from their historical levels—such as slower growth of the labor force—would outweigh factors that push interest rates up from their historical levels—such as rising federal debt. For example, in CBO’s latest 10-year economic projections, the interest rate on 10-year Treasury notes rises from 2.2 percent at the end of 2015 to 4.1 percent in 2026. In CBO’s long-term projections, the rate on those notes rises to 4.7 percent in 2046—still below the average of 5.8 percent between 1990 and 2007. (CBO uses the 1990–2007 period for comparison because it featured stable expectations for inflation and no significant financial crises or severe economic downturns.)

The average interest rate on all federal debt held by the public tends to be lower than the rate on 10-year Treasury notes. (In general, interest rates are lower on shorter-term debt than on longer-term debt; since the 1950s, the average maturity of federal debt has been shorter than 10 years.) On the basis of the agency’s projected spreads of interest rates and the term structure of federal debt, beyond 2026, CBO anticipates that the average interest rate on federal debt will be about 0.4 percentage points lower than the interest rate on 10-year Treasury notes. As a result, CBO projects that the rate will rise to 4.4 percent in 2046.

Rising rates will add significantly to interest costs and thus increase federal debt (as a share of the economy). Although interest rates are projected to remain notably below their average in recent decades, anticipated increases in rates account for roughly three-quarters of the projected increase in debt as a percentage of GDP by 2046. A growing gap between revenues and noninterest spending—which is projected to rise from about 1.5 percent of GDP in 2016 to 3.0 percent of GDP in 2046—accounts for the rest.

Stephanie Barello and Michael Simpson are analysts in the Long-Term Analysis Unit at CBO.