Last Monday, the Congressional Budget Office released The Budget and Economic Outlook: 2018 to 2028, the latest installment of an annual report explaining the agency’s budget and economic projections. This week, CBO is publishing daily blog posts to share key excerpts from the report. Today’s post describes how some important recent legislation affects the agency’s projections. (CBO has also posted a series of slides on that subject.)

In December 2017, Public Law 115-97, referred to here as the 2017 tax act, was enacted. The act made important changes to the tax system that apply to both businesses and individuals. Consequently, CBO had to estimate its effects when preparing its new baseline projections, which incorporate the assumption that current laws affecting taxes and spending generally do not change. In those projections for the 2018–2028 period, the act’s changes boost economic output and increase budget deficits, on net.

What Are the Act’s Major Provisions?

The 2017 tax act changes corporate and individual tax rates and includes various provisions that affect how businesses and individuals calculate their taxable income. Among other things, the act lowers the top corporate income tax rate to 21 percent. It changes the way that the foreign income of U.S. corporations is taxed, and it reduces incentives for corporations to shift profits outside the United States. For the next eight years, the act lowers individual income tax rates and broadens the total amount of income subject to that tax. Also for the next eight years, it increases the tax exemptions for property transferred at death and for certain gifts. Starting next year, it eliminates the penalty for not having health insurance—a penalty imposed under a provision of the Affordable Care Act generally called the individual mandate. And it changes the measure of inflation that is used to adjust certain tax parameters.

What Are the Act’s Projected Economic Effects?

In CBO’s assessment, the 2017 tax act changes businesses’ and individuals’ incentives in various ways. On net, those changes are expected to encourage saving, investment, and work.

CBO projects that the act’s effects on the U.S. economy over the 2018–2028 period will include higher levels of investment, employment, and gross domestic product (GDP). For example, in CBO’s projections, the act boosts average annual real GDP by 0.7 percent over the 2018–2028 period. Analysis of the act’s economic effects is complicated by its mix of permanent and temporary provisions; of particular note is that it lowers the corporate income tax rate permanently but individual income tax rates only through 2025. As a result, the projected economic effects vary over the 11-year period; the largest effects on the economy occur during the period’s middle years.

CBO’s projections of the act’s economic effects are based partly on projections of the act’s effects on potential GDP—the economy’s maximum sustainable level of production. In the agency’s projections, the act increases the level of potential GDP by boosting investment and labor. By lowering the corporate income tax rate, the act gives businesses incentives to increase investment, and by lowering individual income tax rates through 2025, it gives people incentives to increase their participation in the labor force and their hours worked, expanding the potential labor supply and employment. Other provisions of the tax act, including a limit on deductions for state and local taxes and for mortgage interest, will push down residential investment, but the overall effect on investment is positive. One result of the act will dampen those positive effects on potential output: It will increase federal deficits and therefore increase federal borrowing and interest rates, crowding out some private investment.

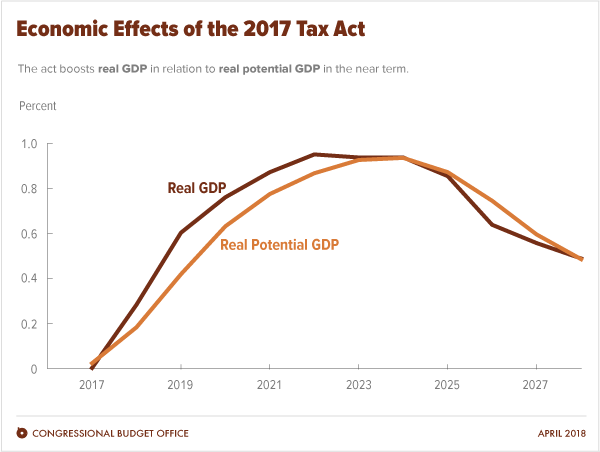

In CBO’s projections, the act initially boosts real GDP (that is, GDP adjusted to remove the effects of inflation) in relation to real potential GDP, influencing other economic variables, such as inflation and interest rates. GDP is pushed up in relation to potential GDP because the act increases overall demand for goods and services (by raising households’ and businesses’ after-tax income). The heightened economic activity subsequently generates more demand for labor and consequently higher wages. In response, the labor force participation rate (which is the percentage of people in the civilian noninstitutionalized population who are at least 16 years old and either working or seeking work) rises, as do the number of hours worked, and the unemployment rate goes down. The largest positive effects occur during the 2018–2023 period. After income tax rates rise as scheduled at the close of 2025, the growth of overall demand is dampened in relation to the growth of potential output.

Among the effects of the initially stronger output growth are slightly higher inflation and an increase in the exchange value of the dollar. Furthermore, CBO expects the Federal Reserve to respond to the stronger labor market and increases in inflationary pressure by pushing short-term interest rates higher over the next few years. Long-term interest rates are also expected to rise.

Just as the tax act is projected to boost real GDP, it is expected to increase income for labor and business over the 2018–2028 period. The act will also affect the relationship between GDP and gross national product (GNP). GNP differs from GDP by including the income that U.S. residents earn from abroad and excluding the income that nonresidents earn from domestic sources; it is therefore a better measure of the income available to U.S. residents. Because the act reduces the amount of net foreign income earned by U.S. residents in CBO’s projections, it increases GNP less than it increases GDP. Over the 11-year period, the act raises the projected level of real GNP by an annual average of about $470 per person (in 2018 dollars); real GDP, by contrast, increases by about $710 per person.

What Are the Act’s Projected Budgetary Effects?

To construct its baseline budget projections, CBO incorporated the effects of the tax act, taking into account economic feedback—that is, the ways in which the act is likely to affect the economy and in turn affect the budget. Doing so raised the 11-year projection of the cumulative primary deficit (that is, the deficit excluding the costs of servicing the debt) by $1.3 trillion and raised projected debt-service costs by roughly $600 billion. The act therefore increases the total projected deficit over the 2018–2028 period by about $1.9 trillion.

Before taking economic feedback into account, CBO estimated that the tax act would increase the primary deficit by $1.8 trillion and debt-service costs by roughly $450 billion. The feedback is estimated to lower the cumulative primary deficit by about $550 billion, mostly because the act is projected to increase taxable income and thus push tax revenues up. And that feedback raises projected debt-service costs, because even though the reduction in primary deficits means that less borrowing is necessary, the act is expected to result in higher interest rates on debt, which are projected to more than offset the effects on debt-service costs of the smaller debt. On net, economic feedback from the act raises debt-service costs in CBO’s projections by about $100 billion.

What Uncertainty Surrounds CBO’s Estimates?

CBO’s estimates of the economic and budgetary effects of the 2017 tax act are subject to a good deal of uncertainty. The agency is uncertain about various issues—for example, the way the act will be implemented by the Treasury; how households and businesses will rearrange their finances in the face of the act; and how households, businesses, and foreign investors will respond to changes in incentives to work, save, and invest in the United States. That uncertainty implies that the actual outcomes may differ substantially from the projected ones.

John McClelland is CBO’s Assistant Director for Tax Analysis and Jeffrey Werling is CBO’s Assistant Director for Macroeconomic Analysis. This post describes the work of about 20 people at CBO.