About 60 million people received Social Security benefits in 2014, CBO estimates. Up to 85 percent of a recipient’s benefits are subject to the individual income tax, depending on the recipient’s overall income. CBO estimates that income taxes on Social Security benefits totaled $51 billion in 2014, an amount that will be credited to the Social Security and Medicare trust funds after the tax returns for 2014 have been filed and analyzed. (CBO expects that those taxes will account for only about 4 percent of the tax revenues received by those trust funds, which receive the other 96 percent of their tax revenues from payroll taxes.)

About half of all Social Security beneficiaries owed some income tax on their benefits in 2014, CBO estimates. Of total Social Security benefits received last year, 6½ percent were owed in income taxes, with smaller percentages owed by many beneficiaries and much larger percentages owed by high-income beneficiaries. Because of legislation and changes in the economy, the share of benefits subject to tax has risen over the past several decades.

Like Social Security, defined benefit pensions typically augment retirees’ income by paying out specified benefits whose size is related to the retirees’ past earnings. However, the share of benefits that is taxed is generally smaller for Social Security than for defined benefit pensions. That difference is minimal for high-income taxpayers but large for low- and moderate-income taxpayers.

How Are Taxes on Social Security Benefits Determined?

Under current law, the share of Social Security benefits that is subject to the individual income tax is determined by a three-tiered tax structure:

- Social Security beneficiaries with income equal to or below $25,000 (for unmarried taxpayers) or $32,000 (for married couples filing jointly) pay no taxes on their benefits. About half of all recipients were in that tier in 2014.

- Beneficiaries with income that is higher than those thresholds but no higher than a second set of thresholds—$34,000 for unmarried filers and $44,000 for joint filers—pay taxes on up to 50 percent of their benefits (with the percentage increasing from 0 percent to 50 percent as income rises).

- For beneficiaries with income that is above those higher thresholds, as much as 85 percent of the benefits are taxed (again, with the percentage increasing as income rises).

The income measure that is used to determine how much of a recipient’s benefits are taxed is a modified version of adjusted gross income (AGI). AGI includes income from all sources not specifically excluded by the tax code, minus certain deductions; modified AGI differs from AGI in that it also includes nontaxable interest income, as well as one-half of a recipient’s Social Security benefits, even if those benefits are ultimately determined not to be taxable.

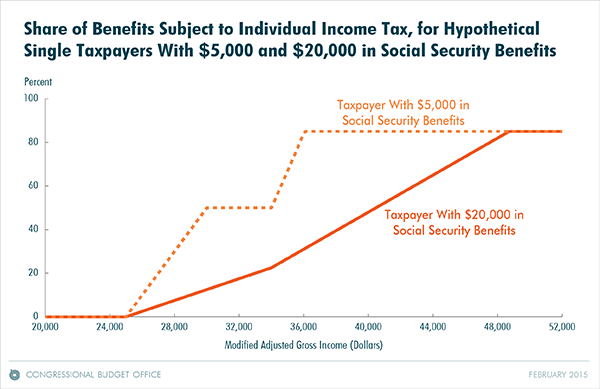

Under that structure, the share of a taxpayer’s benefits that is taxed varies with both the taxpayer’s Social Security benefits and the taxpayer’s other income. For example, an unmarried taxpayer who received $5,000 in Social Security benefits would owe no taxes on those benefits until his or her modified AGI was above $25,000; once modified AGI exceeded about $36,000, that taxpayer would owe taxes on 85 percent of those benefits. By contrast, an unmarried taxpayer who received $20,000 in Social Security benefits would owe taxes on 85 percent of his or her benefits only after his or her modified AGI exceeded about $49,000 (see the figure below).

For taxpayers with income in the ranges over which a larger percentage of Social Security benefits become subject to tax, marginal tax rates on income other than Social Security benefits (that is, the additional amount paid in taxes for each additional dollar of such income) are higher because of the tax treatment of Social Security benefits. For example, those single taxpayers with $5,000 of Social Security benefits in the example above would see their marginal tax rate on non–Social Security income boosted by 50 percent if their modified AGI was between $25,000 and $30,000 and by 85 percent if their modified AGI was between $34,000 and $36,000. Those higher marginal tax rates reduce people’s incentives to work and save.

How Are Taxes on Social Security Benefits Distributed Among Taxpayers?

As noted above, CBO estimates that taxpayers owed 6½ percent of their Social Security benefits in income taxes in 2014. The shares of benefits owed in taxes were much higher for high-income taxpayers than for low-income taxpayers, both because larger shares of benefits were subject to tax for high-income taxpayers and because those taxpayers were in higher income tax brackets. For example, Social Security beneficiaries with income below the first thresholds, who made up roughly half of all beneficiaries, did not pay any taxes on those benefits. By contrast, some beneficiaries in the highest tax bracket owed income taxes on their benefits equal to 33 percent of the benefits—that is, the 85 percent of benefits that were taxable multiplied by the top income tax rate, which was 39.6 percent.

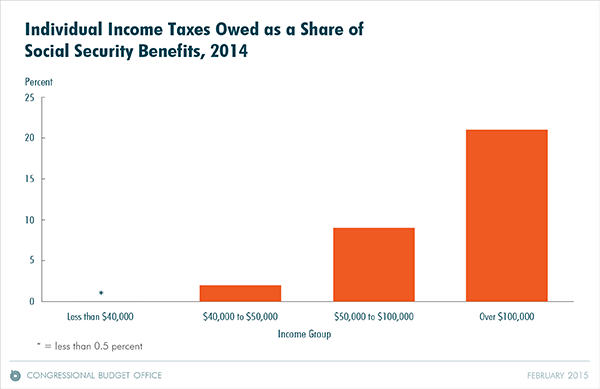

In 2014, CBO estimates, Social Security beneficiaries with income under $40,000 owed less than 0.5 percent of their benefits in income taxes, on average, while those with income over $100,000 owed 21 percent, as the figure below shows. (The measure of income used to group taxpayers in that analysis is broader than modified AGI; it is AGI plus statutory adjustments, tax-exempt interest, and nontaxable Social Security benefits. Additional detail about the estimates is available.)

How Have Taxes on Social Security Benefits Changed Over Time?

The shares of Social Security benefits subject to the individual income tax have grown rapidly since 1984, when benefits first became taxable. Initially, no more than 50 percent of benefits were subject to tax for higher-income taxpayers, and all of those taxes were credited to the Social Security trust funds. That limit was raised in 1994 to the current limit of 85 percent, with the additional taxes resulting from higher amounts credited to the Medicare trust fund.

In addition, the shares of benefits subject to tax have grown because the income thresholds above which benefits are taxable are not indexed for inflation or real income growth. As a result, under current law, those shares will continue to grow in future years. CBO projects that income taxes paid on Social Security benefits will rise from 6½ percent of those benefits in 2014 to more than 8 percent by 2024 and more than 9 percent by 2039.

How Does the Treatment of Taxes on Social Security Benefits Compare With the Treatment of Taxes on Other Pension Income?

Less than 30 percent of all Social Security benefits paid out in 2014 were subject to income tax. By contrast, distributions from defined benefit pension plans were entirely taxable, except for the part of each distribution that represented the recovery of an employee’s “basis”—that is, his or her after-tax contributions to the plan. If benefits paid by the Social Security program were treated the same way—by taxing all benefits that exceeded the basis—federal revenues would be more than $400 billion higher over the next 10 years, the staff of the Joint Committee on Taxation estimates. For additional information, see Options for Reducing the Deficit: 2015 to 2024—Option 55.

Joshua Shakin and Kurt Seibert are analysts in CBO’s Tax Analysis Division. CBO regularly provides analysis that is used in the Green Book, which is published by the House Committee on Ways and Means, and this blog post provides additional information about that analysis.