This morning I testified before the Joint Select Committee on Deficit Reduction—the body created under the Budget Control Act to propose further deficit reductions totaling at least $1.5 trillion over 10 years. I focused on CBO’s August publication, the Budget and Economic Outlook: An Update, what we have learned about performance of the U.S. economy since those last projections were prepared, and CBO’s analysis of the fiscal policy choices facing the Committee and the Congress.

If current policies are continued in coming years, the aging of the population and the rising cost of health care will boost federal spending, as a share of the economy, well above the amount of revenues that the federal government has collected in the past. Putting the budget on a sustainable path will require significant changes in spending policies, tax policies, or both.

Addressing that formidable challenge is complicated by the weakness of the economy and the large numbers of unemployed workers, empty houses, and underused factories and offices. Changes that might be made to federal spending or tax policies could have a substantial impact on the pace of economic recovery during the next few years as well as on the nation’s output and people’s income over the longer term.

The Economic Outlook

The financial crisis and recession have cast a long shadow on the U.S. economy. Although output began to expand again two years ago, the pace of the recovery has been slow, and the economy remains in a severe slump. CBO published its most recent economic forecast in August; that forecast was initially completed in early July and was updated in August only to reflect the policy changes enacted in the Budget Control Act. Looking at incoming data and other developments since early July, our current assessment is as follows:

- Current economic indicators are not pointing to the kinds of imbalances that have preceded previous recessions. We expect that the economic recovery will continue, but at a weaker pace than we had anticipated—with growth in the vicinity of 1½ percent this year and around 2½ percent next year.

- With output growing at only a modest rate, we expect employment to expand very slowly, leaving the unemployment rate close to 9 percent through the end of 2012.

- A large portion of the economic and human costs of this downturn remain ahead of us. Since late 2007, the cumulative difference between output and our estimate of the potential level of output—a level that corresponds to a high rate of use of labor and capital—amounted to about $2½ trillion; by the time output rises back to its potential, probably several years from now, we expect the cumulative shortfall to equal about $5 trillion. Not only are the costs associated with the output gap immense, but they fall disproportionately on people who lose their jobs, are displaced from their homes, or own businesses that fail.

The recent recession was unusual compared with previous ones in terms of its causes, depth, and duration—and the recovery has had unusual features that have been hard to predict. Consequently, the economic outlook remains highly uncertain. Many developments could cause economic outcomes to differ substantially, in one direction or the other, from those we currently anticipate.

The Budget Outlook

If the recovery continues as CBO expects, and if tax and spending policies unfold as specified in current law, deficits will drop markedly as a share of gross domestic product (GDP) over the next few years. Under CBO’s baseline projections, which generally reflect the assumption that current law will not change, deficits fall to 6.2 percent of GDP in 2012 and to 3.2 percent in 2013, and then fluctuate within a range of 1.0 percent to 1.6 percent of GDP from 2014 through 2021.

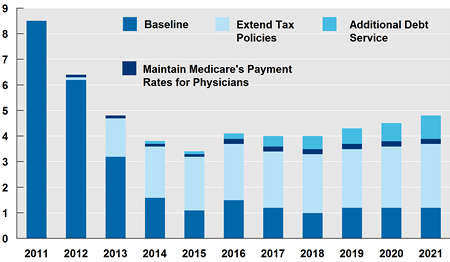

But those baseline projections understate the budgetary challenges facing the nation, because changes in policy that will take effect under current law will produce a federal tax system and spending for some federal programs that differ noticeably from what people have become accustomed to. Changing provisions of current law to maintain major policies would produce markedly different budget outcomes. For example, if most of the tax cuts that were extended through 2011 or 2012 in the 2010 tax legislation were extended indefinitely, the alternative minimum tax (AMT) was indexed for inflation, and Medicare’s payment rates for physicians’ services were held constant, then cumulative deficits over the coming decade—shown by the entire bars in the figure below—would total $8.5 trillion rather than $3.5 trillion in the baseline. By the end of 2021, debt held by the public would reach 82 percent of GDP—considerably more than the 67 percent anticipated at the end of the current fiscal year and higher than in any year since 1948.

Deficits in CBO's Baseline and Assuming a Continuation of Certain Policies (Percent of GDP)

Beyond the coming decade, the fiscal outlook worsens, because the aging of the population and rising costs for health care will exert significant and increasing pressure on the budget under current law. If current policies are extended, federal borrowing to finance the resulting deficits would clearly be unsustainable. Interest payments on the debt would rise dramatically and consume an ever-growing share of the federal budget. Even before the interest burden became unsupportable, a fiscal crisis could arise if participants in financial markets lost confidence in the government’s ability to manage its budget and became unwilling to lend to the government at affordable rates. Thus, under current policies, the federal budget is quickly heading into territory that is unfamiliar to the United States and to most other developed countries as well. (See CBO’s Long-Term Budget Outlook released in June.)

Fiscal Policy Choices

As the Committee considers its charge to recommend policies that would reduce future budget deficits, its key choices fall into three broad categories.

How much deficit reduction should be accomplished?

There is no commonly agreed upon level of federal debt that is sustainable or optimal. At a minimum, federal debt cannot continually increase as a share of the economy because the interest payments on that debt would then continually grow relative to the size of the tax base that would be available for generating revenues to cover those payments and all of the other activities of the government. Under CBO’s current-law baseline, debt held by the public is projected to fall from 67 percent of GDP this year to 61 percent by 2021. However, stabilizing the debt at that level would leave it larger than in any year between 1953 and 2009.

Lawmakers might determine that debt should be reduced to amounts closer to those we have experienced in the past, relieving some of the long-term pressures on the budget diminishing the risk of a fiscal crisis, and enhancing the government’s flexibility to respond to unanticipated developments. If, for example, the Committee chose to make recommendations that would lower debt held by the public in 2021 to 50 percent of GDP, roughly the level recorded in the mid-1990s, it would need to propose changes in policies—relative to those embodied in current law, which underlie CBO’s baseline projections—that reduced deficits by a total of about $3.8 trillion over the coming decade, rather than the $1.2 trillion needed to avoid automatic budget cuts.

Furthermore, lawmakers might decide that some of the current tax and Medicare payment rate policies (described above) scheduled to expire under current law should be continued. In that case, reducing debt in 2021 to the 61 percent of GDP projected under current law would require other changes in policy to reduce deficits over the next 10 years by a total of $6.2 trillion.

How quickly should deficit reduction be implemented?

Determining the timing of deficit reduction involves difficult trade-offs:

- Cutting spending or increasing taxes slowly would lead to a greater accumulation of government debt and might raise doubts about whether the longer-term deficit reductions would ultimately take effect.

- Implementing spending cuts or tax increases abruptly would give people little time to plan and adjust, and would be an added drag on the weak economic expansion.

Credible policy changes that would substantially reduce deficits later in the coming decade and beyond—without immediate spending cuts or tax increases—would both support the economic expansion in the next few years and strengthen the economy over the longer term.

Moreover, there is no inherent contradiction between using fiscal policy to support the economy today and imposing fiscal restraint several years from now. If policymakers wanted to achieve both a short-term economic boost and longer-term fiscal sustainability, a combination of policies would be required: changes in taxes and spending that would widen the deficit now but reduce it later in the decade.

What forms should deficit reduction take?

Federal spending and revenues affect the total amount and types of output that are produced, the distribution of that output among various segments of society, and people’s well-being. Many observers wonder whether it is possible to return to previous policies regarding federal spending and revenues. Unfortunately, the past combination of policies cannot be repeated: The aging of the population and rising costs for health care have changed the backdrop for budget policy in a fundamental way.

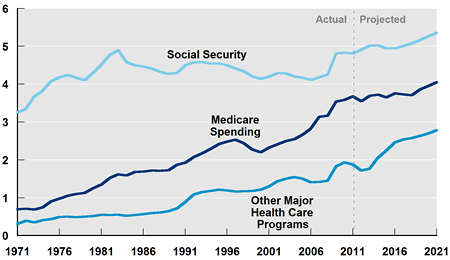

Under current law, spending on Social Security, Medicare, and other major health care programs—Medicaid, the Children’s Health Insurance Program, and insurance subsidies to be provided through exchanges (the darkest line in the figure below)—is projected to reach about 12 percent of GDP in 2021, compared with an average of about 7 percent during the past 40 years.

Spending for Social Security, Medicare, and Other Major Health Care Programs (Percent of GDP)

If the laws governing Social Security and the major health care programs were unchanged, and all other programs were operated in line with their average relationship to the size of the economy during the past 40 years (more than 11 percent of GDP), total federal spending excluding net interest would be nearly 24 percent of GDP. That amount exceeds the 40-year average for revenues as a share of GDP by nearly 6 percentage points—even before interest payments on the debt have been included.

At the same time, the sharp increase in federal debt and a return to more-normal interest rates will boost the government’s net interest costs. They are projected to reach 2.8 percent of GDP in 2021, compared with only 1.5 percent of GDP in 2011 and an average of 2.2 percent of GDP during the past 40 years.

What do those numbers imply about the choices that policymakers—and citizens—confront about future policies? Attaining a sustainable budget for the federal government will require the United States to deviate from the policies of the past 40 years in at least one of the following ways:

- Raise federal revenues significantly above their average share of GDP;

- Make major changes to the sorts of benefits provided for Americans when they become older; or

- Substantially reduce the role of the rest of the federal government relative to the size of the economy.

The nation cannot continue to sustain the spending programs and policies of the past with the tax revenues it has been accustomed to paying. Citizens will either have to pay more for their government, accept less in government services and benefits, or both.