In this report, CBO assesses the usefulness of cash and accrual accounting for several federal insurance programs—including deposit, flood, and pension insurance—and considers ways to increase use of accrual measures in the budget process.

CBO Blog

In its June 2017 projections, CBO overestimated federal outlays and revenues for fiscal year 2018 by 1.7 percent and 1.2 percent, respectively. The projected federal budget deficit for 2018 was 3.7 percent more than the actual amount.

This week, CBO was recognized by the Partnership for Public Service as one of the best places to work in the federal government. CBO ranked third among 29 agencies in the small-agency category.

Options for Reducing the Deficit: 2019 to 2028 is the latest edition of a report that CBO publishes periodically and describes 121 policy options that would decrease federal spending or increase federal revenues over the next decade.

CBO projects that the annual cost (in 2018 dollars) of replacing the aircraft in the current fleet, essentially one-for-one, would average $15 billion in the 2020s, $23 billion in the 2030s, and $15 billion in the 2040s.

The federal budget deficit was $303 billion for the first two months of fiscal year 2019, CBO estimates, $102 billion more than the deficit recorded during the same period last year.

The share of international affairs funding that was provided outside of agencies’ base budget for ongoing activities—that is, “nonbase” funding—increased markedly from 2014 to 2017, mostly for overseas contingency operations.

-

On Thursday, December 13, CBO will release Options for Reducing the Deficit: 2019 to 2028. This report will describe 121 policy options that would decrease federal spending or increase federal revenues over the next decade.

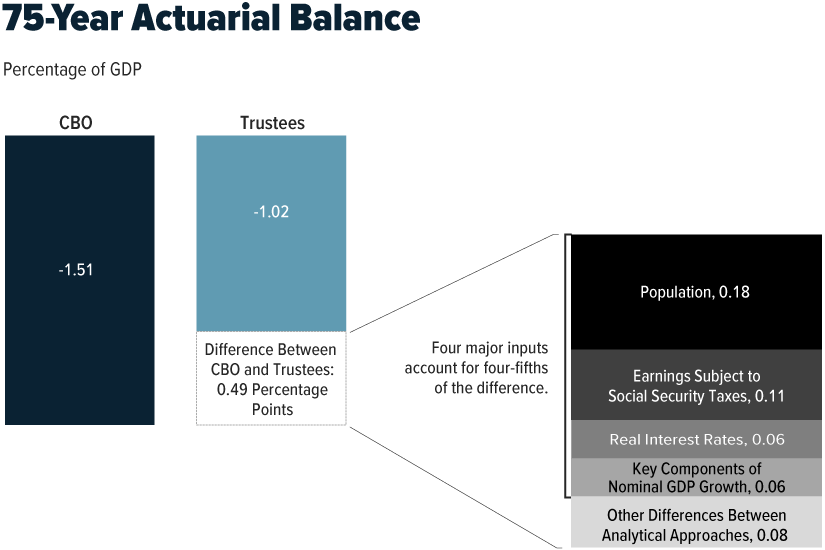

This report explains the changes to CBO’s long-term Social Security projections since last year and compares CBO’s projections with those of the Social Security Trustees.

CBO found that the tax burden on intangible assets is lower than that on tangible assets. In CBO’s estimation, the 2017 tax act increases the tax burden on research and development but reduces it on most other intangible assets.