At a Glance

Each year, the Congressional Budget Office publishes a report presenting its projections of what the federal budget and the economy would look like over the next 30 years if current laws generally remained unchanged. The long-term budget projections typically follow CBO’s 10-year baseline budget projections and then extend most of the concepts underlying them for an additional 20 years. This year, the long-term projections are based on CBO’s May 2023 baseline projections but also reflect the estimated budgetary effects of the Fiscal Responsibility Act of 2023 (Public Law 118-5), which was enacted on June 3, 2023.

Deficits. In CBO’s projections, the deficit equals 5.8 percent of gross domestic product (GDP) in 2023, declines to 5.0 percent by 2027, and then grows in every year, reaching 10.0 percent of GDP in 2053. Over the past century, that level has been exceeded only during World War II and the coronavirus pandemic. The increase in the total deficit results from faster growth in spending than in revenues. The primary deficit, which excludes interest costs, equals 3.3 percent of GDP in both 2023 and 2053, but the total deficit is boosted by rising interest costs.

Debt. By the end of 2023, federal debt held by the public equals 98 percent of GDP. Debt then rises in relation to GDP: It surpasses its historical high in 2029, when it reaches 107 percent of GDP, and climbs to 181 percent of GDP by 2053. Such high and rising debt would slow economic growth, push up interest payments to foreign holders of U.S. debt, and pose significant risks to the fiscal and economic outlook; it could also cause lawmakers to feel more constrained in their policy choices.

Spending. In 2023, outlays fall to 24.2 percent of GDP as federal spending in response to the pandemic diminishes. Outlays continue to decline through 2026 but increase thereafter, reaching 29.1 percent of GDP in 2053. (By comparison, from 1993 to 2022, outlays averaged 21.0 percent of GDP.) Rising interest rates and persistently large primary deficits cause interest costs to almost triple in relation to GDP between 2023 and 2053. Spending on the major health care programs and Social Security—driven by the aging of the population and growing health care costs—also boosts federal outlays significantly over the next 30 years.

Revenues. Revenues fall to 18.4 percent of GDP in 2023 and continue to drop until 2026, when the scheduled expiration of certain provisions of the 2017 tax act causes tax receipts to increase. Revenues generally rise thereafter, reaching 19.1 percent of GDP in 2053, as an increasing share of income is pushed into higher tax brackets. (By comparison, from 1993 to 2022, revenues averaged 17.2 percent of GDP.)

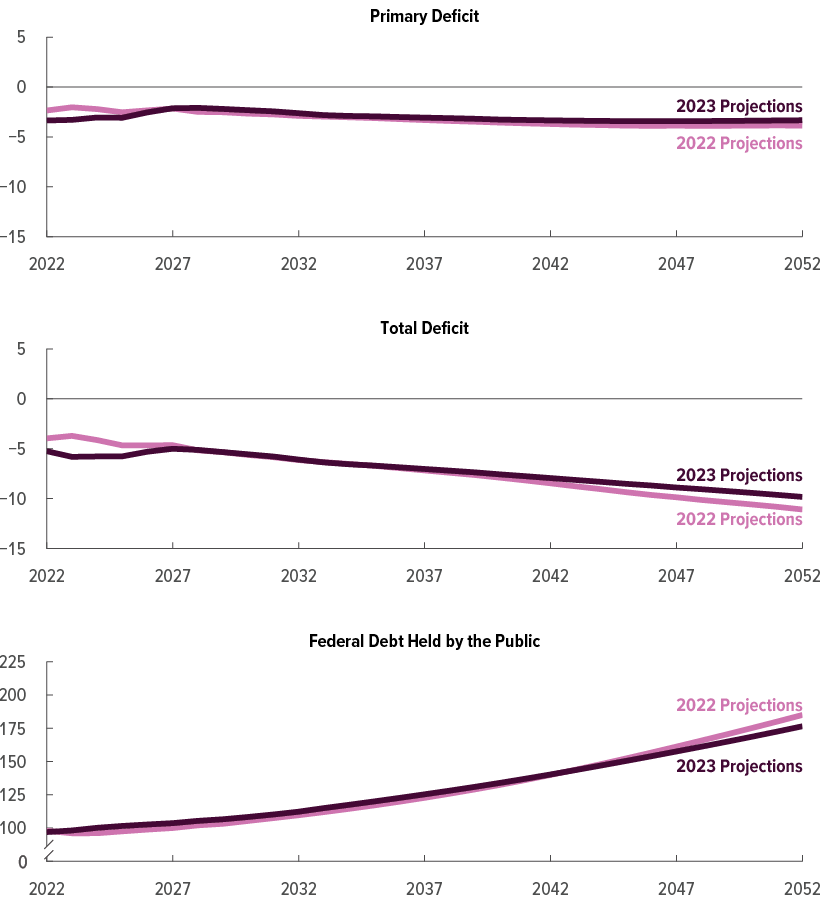

Changes From Previous Projections. Measured as a percentage of GDP, federal debt is now projected to be 2 percentage points higher in 2023 and 9 percentage points lower in 2052 than it was in last year’s report. Overall, CBO’s projections of debt have increased through 2042 and decreased in later years.

By the Numbers

Long-Term Budget Outlook, June 2023, by Fiscal Year

Percentage of Gross Domestic Product

See Chapter 1 and Chapter 2. Deficits and outlays have been adjusted to exclude the effects of shifts in the timing of certain payments when October 1, the first day of the fiscal year, falls on a weekend.

Long-Term Economic Outlook, June 2023, by Calendar Year

Percent

See Chapter 3 and Appendix C.

Notes

The Congressional Budget Office’s long-term budget projections, referred to as the extended baseline, typically follow the agency’s 10-year baseline budget projections and then extend most of the concepts underlying those projections for an additional 20 years. This year, however, the long-term projections are based on the agency’s May 2023 baseline projections but also reflect the estimated budgetary effects of the Fiscal Responsibility Act of 2023 (FRA, Public Law 118-5), enacted on June 3, 2023. Other legislation enacted between March 30, 2023 (when CBO finalized its May baseline), and June 3, 2023, did not have significant budgetary effects.

Those projections are consistent with the demographic projections that the agency published on January 24, 2023, and the economic forecast that it published on February 15, 2023. They do not reflect the economic effects of administrative actions, regulatory changes, legislation, or economic developments after December 6, 2022, when that forecast was finalized. Nor do they reflect the budgetary effects of any developments after March 30, 2023, except for the enactment of the FRA.

In accordance with statutory requirements, CBO’s projections reflect the assumptions that current laws generally remain unchanged, that some mandatory programs are extended after their authorizations lapse, and that spending on Medicare and Social Security continues as scheduled even if their trust funds are exhausted.

Unless this report indicates otherwise, all years referred to in describing budget projections are federal fiscal years, which run from October 1 to September 30 and are designated by the calendar year in which they end. Years referred to in describing economic projections are calendar years.

When October 1 (the first day of the fiscal year) falls on a weekend, certain payments that ordinarily would have been made on that day are instead made at the end of September and thus are shifted into the previous fiscal year. In this report, budget projections have been adjusted to exclude the effects of those timing shifts.

Unless this report notes otherwise, Medicare outlays are presented net of premiums paid by beneficiaries and other offsetting receipts, which reduce outlays for the program.

Numbers in the text, tables, and figures may not add up to totals because of rounding.

Supplemental information files—the data underlying the tables and figures in this report, supplemental budget projections, and the economic variables underlying those projections—are posted on CBO’s website at www.cbo.gov/publication/59014#data. Previous editions of this report are available at https://go.usa.gov/xmezZ.

Visual Summary

The United States faces a challenging fiscal outlook. If current laws generally remained unchanged, budget deficits and federal debt would grow in relation to gross domestic product (GDP) over the next three decades, according to the Congressional Budget Office’s projections. The figures below present highlights from those projections and the economic forecast underlying them.

Deficits and Debt

In CBO’s projections, federal deficits increase from 6 percent of GDP in 2023 to 10 percent in 2053. Such persistently large deficits cause federal debt, which is already high, to rise even further: Debt held by the public reaches 181 percent of GDP in 2053.

Deficits

Percentage of GDP

Primary deficits, which exclude interest costs, equal 3.3 percent of GDP in both 2023 and 2053. Combined with rising interest rates, those large and sustained primary deficits cause net outlays for interest to almost triple in relation to GDP.

Federal Debt Held by the Public

Percentage of GDP

Debt rises in relation to GDP over the next three decades, exceeding any previously recorded level—and it is on track to continue growing after 2053.

Spending and Revenues

Federal spending grows from 24 percent of GDP in 2023 to 29 percent of GDP in 2053. Federal revenues increase less over that period—from 18 percent to 19 percent of GDP.

Total Outlays and Revenues

Percentage of GDP

Outlays increase faster than revenues—mainly because of rising interest costs and growth in spending on the major health care programs and Social Security. The result is ever-larger budget deficits over the long term.

Outlays, by Category

Percentage of GDP

Rising interest rates and mounting debt cause net outlays for interest to increase from 2.5 percent of GDP in 2023 to 6.7 percent in 2053.

Outlays for the major health care programs rise from 5.8 percent of GDP to 8.6 percent as the average age of the population increases and health care costs grow.

The aging of the population also pushes up outlays for Social Security, which increase from 5.1 percent of GDP to 6.2 percent.

Revenues, by Source

Percentage of GDP

From 2023 to 2053, total revenues, measured as a percentage of GDP, grow by about 1 percentage point. Individual income taxes account for nearly all of that growth.

Receipts from payroll and corporate taxes decline by small amounts in relation to GDP over the 30-year period.

Key Factors Contributing to Changes in Revenues

Percentage of GDP

Over the long term, the largest source of growth in revenues is real bracket creep: As income rises faster than prices, a larger proportion of income becomes subject to higher tax rates.

After 2025, another significant source of growth in revenues is the scheduled expiration of certain provisions of the 2017 tax act.

Other factors partially offset those effects. In 2023 and 2024, for example, revenues fall in relation to GDP as a temporary boost to tax receipts observed in recent years abates.

The Economy

The state of the U.S. economy in coming decades will affect the federal government’s budget deficits and debt. Key components of CBO’s long-term economic forecast are its projections of real potential GDP—the maximum sustainable output of the economy, adjusted to remove the effects of inflation—and interest rates.

Average Annual Growth of Real Potential GDP and Its Components

Percent

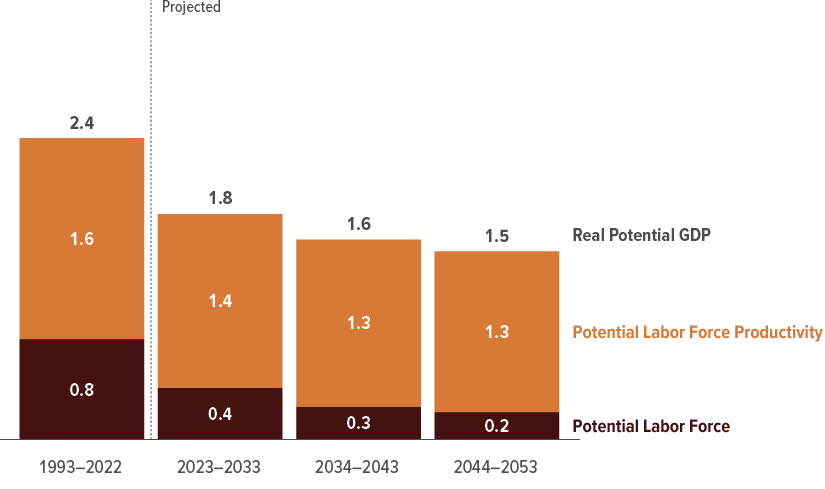

Real potential GDP grows more slowly throughout the 2023–2053 period than it has, on average, over the past 30 years.

That slower growth is explained by slower growth in the potential labor force and in potential labor force productivity.

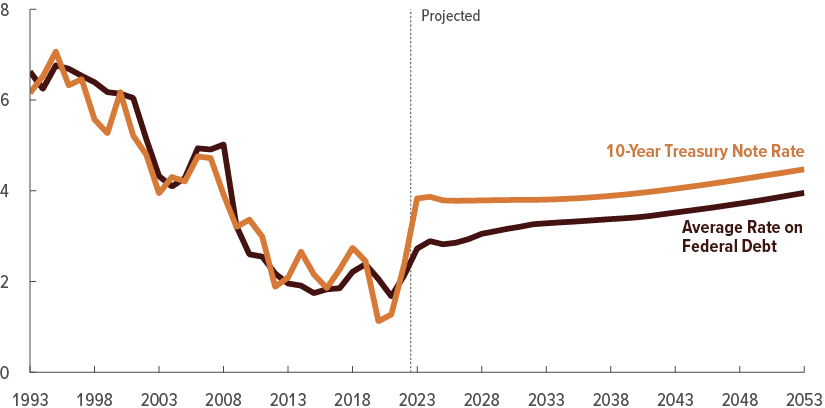

Average Interest Rates on Federal Debt and on 10-Year Treasury Notes

Percent

Interest rates—which, along with primary deficits, help determine net outlays for interest—rise through 2053 but remain lower than they have been, on average, over the past three decades.

Projected interest rates remain below that average for several reasons, including slower growth of the labor force, an increase in savings available for investment, and slower growth of total factor productivity.

Chapter 1Deficits and Debt

Overview

If current laws governing taxes and spending generally remained unchanged, the federal budget deficit would increase significantly in relation to gross domestic product (GDP) over the next 30 years, the Congressional Budget Office projects. Those growing deficits are projected to drive up federal debt held by the public. In 2053, such debt would exceed any previously recorded level—and would be on track to increase further (see Figure 1-1).

Figure 1-1.

Deficits and Debt

Percentage of GDP

In CBO’s projections, primary deficits exceed their historical 50-year average of 1.5 percent of GDP throughout the projection period. In 2053, the primary deficit equals 3.3 percent of GDP. Driven up by large and sustained primary deficits and by rising interest rates, net interest outlays reach 6.7 percent of GDP in 2053.

Growing deficits push federal debt held by the public, which is already high, further up throughout the 30-year period. Such debt reaches 181 percent of GDP in 2053—and would continue to rise thereafter.

Data source: Congressional Budget Office. See www.cbo.gov/publication/59014#data.

Primary deficits exclude net outlays for interest.

GDP = gross domestic product.

Measured in relation to the size of the economy, this year’s budget deficit is comparable to last year’s deficit and smaller than the shortfalls recorded in 2020 and 2021, when federal spending spiked in response to the coronavirus pandemic. Nevertheless, in CBO’s projections, federal deficits are large by historical standards: From 2023 to 2053, deficits average 7.3 percent of GDP, more than double their average over the past half-century. And deficits are projected to grow almost every year over the next three decades, reaching 10.0 percent of GDP in 2053.1 In the past 100 years, deficits have been that large only during World War II and the pandemic. The growth in deficits over the next three decades occurs as increases in spending—especially spending on interest, the major health care programs, and Social Security—outpace increases in revenues.

Persistently large deficits would lead to substantial increases in federal debt. In CBO’s projections, federal debt held by the public, measured in relation to GDP, surpasses its highest level in history in 2029, reaching 107 percent. Debt continues to climb thereafter and reaches 181 percent of GDP at the end of 2053.

Such high and rising debt would have significant economic and financial consequences. It would, among other things, slow economic growth, drive up interest payments to foreign holders of U.S. debt, elevate the risk of a fiscal crisis, increase the likelihood of other adverse effects that could occur more gradually, and make the nation’s fiscal position more vulnerable to an increase in interest rates. In addition, it could cause lawmakers to feel more constrained in their policy choices.

Budgetary outcomes are hard to predict, particularly over the long run. Even if federal laws remained unchanged, CBO’s budget projections would be subject to considerable uncertainty. If developments in the economy, demographics, or other factors that affect revenues and outlays diverged from the agency’s projections, budgetary outcomes would diverge as well. That uncertainty increases over time because changes in factors that affect the budget are difficult to anticipate over long time horizons.

Deficits and Debt Through 2053

In CBO’s projections, deficits generally rise through 2053. As deficits grow in relation to the size of the economy, so does federal debt.

Deficits

The total deficit—including net outlays for interest—is estimated to be 5.8 percent of GDP in 2023, comparable to what it was in 2022. In CBO’s projections, the deficit declines through 2027 before increasing steadily through 2053. At that point, the deficit—equal to 10.0 percent of GDP—is significantly larger than the 3.6 percent of GDP that deficits averaged over the past 50 years (see Table 1-1). Moreover, in years in the past half-century when unemployment was relatively low, as it is in CBO’s projections, the average deficit was even smaller.

Table 1-1.

Key Projections for Selected Years

Percentage of Gross Domestic Product

Data source: Congressional Budget Office. See www.cbo.gov/publication/59014#data.

This table provides the information specified in section 3111 of S. Con. Res. 11, the Concurrent Resolution on the Budget for Fiscal Year 2016.

CBO’s long-term budget projections, referred to as the extended baseline, typically follow the agency’s 10-year baseline budget projections and then extend most of the concepts underlying those projections for an additional 20 years. This year, however, the long-term projections are based on the agency’s May 2023 baseline projections but also reflect the estimated budgetary effects of the Fiscal Responsibility Act of 2023 (Public Law 118-5), enacted on June 3, 2023.

When October 1 (the first day of the fiscal year) falls on a weekend, certain payments that ordinarily would have been made on that day are instead made at the end of September and thus are shifted into the previous fiscal year. All projections have been adjusted to exclude the effects of those timing shifts.

a. Consists of excise taxes, remittances to the Treasury from the Federal Reserve System, customs duties, estate and gift taxes, and miscellaneous fees and fines.

b. Consists of outlays for Medicare (net of premiums and other offsetting receipts), Medicaid, and the Children’s Health Insurance Program, as well as subsidies for health insurance purchased through the marketplaces established under the Affordable Care Act and related spending.

c. Includes payroll taxes other than those paid by the federal government on behalf of its employees; those payments are intragovernmental transactions. Also includes income taxes paid on Social Security benefits, which are credited to the Social Security trust funds.

d. Does not include outlays related to the administration of the program, which are discretionary. For Social Security, outlays do not include intragovernmental offsetting receipts stemming from the employer’s share of payroll taxes paid to the Social Security trust funds by federal agencies on behalf of their employees.

e. The net increase in the deficit shown here differs from the change in the trust fund balance for the program. It does not include intragovernmental transactions, interest earned on balances, or outlays related to the administration of the program.

Primary deficits exclude net outlays for interest, reflecting the difference between noninterest spending and revenues—the main mechanisms through which lawmakers can directly influence the trajectory of the federal debt and interest costs. In CBO’s projections, primary deficits exceed their historical 50-year average of 1.5 percent of GDP in every year. In both 2023 and 2053, the primary deficit equals 3.3 percent of GDP, though such deficits vary in the interim; they generally decline through 2028, when the primary deficit drops to 2.1 percent of GDP, before increasing in most subsequent years. That later growth in primary deficits occurs because increases in noninterest spending—chiefly increases in spending on the major health care programs and Social Security attributable to the aging of the population and rising health care costs—outstrip increases in revenues.

Combined with rising interest rates, large and sustained primary deficits cause net outlays for interest to increase significantly in relation to the size of the economy, from 2.5 percent of GDP in 2023 to 6.7 percent of GDP in 2053. On average, primary deficits account for about one-third of the projected rise in net interest costs over the 2023–2053 period; higher interest rates account for the rest.

Federal Debt Held by the Public

Debt held by the public rises from 97 percent of GDP at the end of 2022 to 98 percent of GDP in 2023 in CBO’s projections.2 By 2029, debt held by the public climbs to 107 percent of GDP, exceeding the historical peak of 106 percent reached in 1946, immediately after World War II. In 2053, debt reaches 181 percent of GDP and is on track to rise higher still.

Consequences of High and Rising Federal Debt

If federal debt continued to rise in relation to GDP at the pace that CBO projects it would under current law, it would have far-reaching implications for the fiscal and economic outlook.3 The consequences of that high and rising debt would include the following:

- Borrowing costs throughout the economy would rise, reducing private investment and slowing the growth of economic output.

- Rising interest costs associated with that debt would drive up interest payments to foreign holders of U.S. debt, decreasing the nation’s net international income.

- There would be an elevated risk of a fiscal crisis—that is, a situation in which investors lose confidence in the U.S. government’s ability to service and repay its debt, causing interest rates to increase abruptly, inflation to spiral upward, or other disruptions to occur.

- The likelihood of other adverse effects would also increase. For example, expectations of higher rates of inflation could become widespread, which could erode confidence in the U.S. dollar as the dominant international reserve currency.

- The United States’ fiscal position would be more vulnerable to an increase in interest rates, because the higher debt is, the more an increase in interest rates raises debt-service costs.

- Lawmakers might feel constrained in using fiscal policy to respond to unforeseen events or for other purposes, such as to promote economic activity or strengthen national defense.

Nevertheless, policies that drive up debt by increasing spending or reducing revenues can benefit people and provide support to the economy, especially during challenging times. And federal investment—including investment financed by deficits—can boost private-sector productivity and output (although that increased output would only partially mitigate the adverse fiscal consequences of increased federal borrowing).

Higher debt itself can also have beneficial consequences. Higher interest rates on Treasury securities can help workers save for retirement by increasing the return they can earn on those assets. Similarly, higher interest rates on Treasury securities can help businesses by increasing their return on a liquid asset that can be used to cover payroll and other expenses (though their borrowing costs would be higher, and an increase in the rate of return on newly issued Treasury securities would reduce the value of existing securities of the same maturity).

Slower Economic Growth

High and rising federal debt would, over time, push up the cost of borrowing, reduce private investment, and slow the growth of GDP, all else being equal.

Higher debt tends to increase borrowing costs in both the public and private sectors by driving up interest rates. As a result, investment in productive capital, such as housing and commercial structures, decreases. That reduction in private investment would slow economic growth: As investment in capital goods declined, workers would, on average, have fewer resources to do their jobs; as a result, they would be less productive, their compensation would be lower, and they would therefore be less inclined to work. Those effects would increase over time as federal borrowing grew.

In CBO’s projections, the reduction in private investment stemming from higher debt is partially offset by at least three effects. First, additional government borrowing strengthens people’s incentive to save, partly by driving up interest rates.4 Second, higher interest rates tend to attract more foreign capital to the United States, and some of those funds become available for private investment. And third, federal borrowing that supports effective federal investment typically increases private-sector productivity and, therefore, private investment.5 (However, spending on such investment accounts for little of the increasing deficits and debt in CBO’s projections.) In CBO’s assessment, the increase in private investment stemming from those three factors would not be as large as the reduction in private investment resulting from higher debt.

Increased Interest Payments to Foreign Holders of U.S. Debt

If federal debt held by the public continued to rise, the government would spend more on interest payments—including payments to foreign investors, who currently hold roughly one-third of that debt overall (and 41 percent of such debt not held by the Federal Reserve). Increases in interest payments to foreign investors would, in turn, reduce the nation’s net international income—the difference between the nation’s income (as measured by its gross national product, or GNP) and its total output (as measured by GDP)—by reducing national income.6 When net international income declines, national income also declines, all else being equal.7

Greater Risk of a Fiscal Crisis

The likelihood of a fiscal crisis would increase as federal debt continued to rise, because mounting debt could erode investors’ confidence in the U.S. government’s fiscal position. Such an erosion of confidence would undermine the value of Treasury securities and would drive up interest rates on federal debt as investors demanded higher yields to purchase those securities. Concerns about the government’s fiscal position could lead to a sudden and potentially spiraling increase in people’s expectations for inflation, a large drop in the value of the dollar, or a loss of confidence in the government’s ability or commitment to repay its debt in full, all of which would make a fiscal crisis more likely.

A fiscal crisis could lead to a financial crisis. In a fiscal crisis, dramatic increases in Treasury rates would reduce the market value of outstanding government securities, and the resulting losses incurred by institutions and businesses that held those securities—including mutual funds, pension funds, insurance companies, and banks—could be large enough to cause some financial institutions to fail. Because the United States plays a central role in the international financial system, such a crisis could spread globally.

Risk Factors. The risk of a fiscal crisis depends on more than the amount of federal debt. Ultimately, it is the cost of servicing the debt and the ability to refinance it as needed that matter. Among the factors affecting those two things are investors’ expectations—about the outlook for the budget and the economy and about domestic and international financial conditions, including interest rates and exchange rates.

CBO does not have sufficient information to reliably quantify the probability of a fiscal crisis. In CBO’s assessment, no tipping point can be identified at which the debt-to-GDP ratio would become so high that it made a crisis likely or imminent, nor is there a fixed point at which interest costs would become so high in relation to GDP that they were unsustainable.

Risk of a Crisis in the Near Term. The risk of a fiscal crisis in the near term appears to be low despite the current large amount of federal debt. The near-term risk is mitigated by certain characteristics of the U.S. financial system that tend to sustain demand for Treasury securities. For example, the Federal Reserve conducts independent monetary policy, government debt is issued in U.S. dollars, the dollar holds a central place in the global financial system, and few investments can provide returns comparable to those of Treasury securities at similarly low levels of credit risk.

In addition, concern about a fiscal crisis in the near term is not currently apparent in financial markets. However, financial markets do not always fully reflect risks on the horizon, and the risk of a fiscal crisis could change suddenly in the wake of unexpected events. For example, a sudden rise in interest rates that persists for an extended period could cause investors to become concerned about the government’s fiscal position over the long term.

Increased Likelihood of Other Adverse Effects

Even in the absence of an abrupt fiscal crisis, high and rising debt could have adverse effects on the economy beyond those incorporated into CBO’s projections, including a gradual decline in the value of Treasury securities and other domestic assets, heightened expectations of inflation, and a loss of confidence in the U.S. dollar as the dominant international reserve currency. Such developments would, among other things, make it more difficult to finance public and private activity.

Greater Vulnerability of U.S. Fiscal Position to an Increase in Interest Rates

Higher debt makes the United States’ fiscal position more vulnerable to an increase in interest rates. Debt of the amounts in CBO’s projections increases the risk that interest costs would be substantially greater than projected—even without a fiscal crisis—if interest rates were higher than projected. (The average interest rate on federal debt in CBO’s projections increases from 2.7 percent in 2023 to 3.3 percent in 2033 and to 4.0 percent in 2053. If, for example, that average rate followed CBO’s projections through 2052 but was 1 percentage point higher in 2053, net interest costs measured as a percentage of GDP would be 1.7 percentage points higher in that year, all else being equal.) Conversely, lower interest rates would result in lower-than-projected interest costs.

Increased Perception of Fiscal Constraints Among Policymakers

The size of budget deficits and debt could influence policymakers’ choices. If debt was already high, policymakers might feel constrained from using deficit-financed fiscal policy to respond to unforeseen events, promote economic activity, or further other goals. High debt could also undermine the international geopolitical role of the United States if policymakers were reluctant to increase spending to prepare for or respond to an international crisis.

Uncertainty of CBO’s Long-Term Projections

CBO’s long-term budget projections give lawmakers a point of comparison from which to measure the effects of policy options or proposed legislation; they are not predictions of budgetary outcomes. Moreover, the budget projections are uncertain because they depend on the agency’s economic and demographic projections, which are themselves uncertain. Developments that differ from the historical experiences on which the projections are based could significantly increase or decrease federal debt in relation to CBO’s projections.

Uncertainty About Budgetary Outcomes

CBO’s budget projections are intended to show what would happen to federal spending, revenues, deficits, and debt if current laws governing spending and taxes generally remained the same. But even if federal laws remained unchanged over the next three decades, actual budgetary outcomes would differ from CBO’s projections because of unanticipated changes in economic conditions and in other factors that affect federal spending and revenues. Moreover, those outcomes will depend on future legislative action, which could increase or decrease budget deficits.

The uncertainty in CBO’s budget projections increases in later years of the projection period because changes in the economy, demographics, and a variety of other factors are more difficult to anticipate over longer time horizons.

Uncertainty About the Economic Outlook

CBO’s economic projections are subject to a high degree of uncertainty. For instance, the possibility that growth in the labor force or in productivity could be faster or slower than expected makes CBO’s projections of labor market conditions and economic output uncertain. Other key sources of uncertainty are future monetary policy and the path of interest rates. For example, uncertainty about the path of interest rates contributes to uncertainty about the impact that higher deficits and debt would have on the economy. And geopolitical events, such as the war in Ukraine, add to the uncertainty of the economic outlook.

Uncertainty About the Demographic Outlook

CBO’s long-term demographic projections are subject to significant uncertainty because, compounded over many years, even small changes in rates of fertility, mortality, or net immigration could greatly affect outcomes later in the projection period.8 For example, because many immigrants are of working age, higher-than-projected net immigration would result in a larger-than-projected labor force, and lower-than-projected net immigration would have the opposite effect. Changes in fertility rates would have larger effects once members of the affected generations reached working age. Changes in mortality rates, which would probably most affect the size of the older population, would cause outlays for the major health care programs and Social Security to diverge from CBO’s projections.

Uncertainty About Other Potential Developments

Because CBO’s projections are based on historical trends, developments that have few historical precedents or are otherwise difficult to predict constitute a significant source of uncertainty. Such developments—for example, a severe economic downturn, unexpectedly strong and sustained economic growth, the discovery or development of natural resources, or unanticipated effects of climate change—could lead to budgetary outcomes that are much better or worse than CBO projects.

A Severe Economic Downturn. CBO’s long-term projections of output and unemployment reflect trends from the end of World War II to the present—a period that included several economic downturns that were not fully offset by upturns of similar magnitude. But particularly severe and protracted economic downturns are rare.

If such a downturn occurred, budgetary outcomes could significantly diverge from CBO’s projections. Economic downturns can reduce revenues and raise outlays for unemployment insurance, nutrition assistance, or other programs that provide support to people and businesses. In addition, downturns have historically prompted policymakers to enact legislation that further reduces revenues and increases federal spending—to increase people’s incomes, bolster the financial position of state and local governments, and stimulate economic activity and employment. Such developments can lead to substantial increases in federal debt. For example, in the aftermath of the 2007–2008 financial crisis, federal debt held by the public rose from 39 percent of GDP at the end of fiscal year 2008 to 70 percent of GDP at the end of 2012.

Unexpectedly Strong Economic Growth. Likewise, a source of uncertainty in CBO’s projections is the possibility that economic growth could be much stronger than the agency expects on the basis of historical trends. A substantial increase in productivity—for example, because of technological advances—could cause such a development. As a result, revenues could be higher than CBO projects, and outlays, including those for support programs, could be lower.

The Discovery and Development of Natural Resources. CBO’s projections reflect the effects of previous advances in the development of natural resources—for example, increases in federal tax revenues that stemmed from an increase in the production of oil and natural gas from shale. However, it is impossible to predict the discovery of natural resources or new ways to extract them, and the effects of any such discovery on the federal budget would depend on private investment, government regulations, the infrastructure necessary to access and transport those resources, and other factors.

Unanticipated Effects of Climate Change. On net, CBO expects climate change to reduce economic growth and increase budget deficits. The budgetary effects of climate change are expected to increase over time, but because climate change is an evolving phenomenon, the nature and extent of those changes are uncertain. (For a discussion of the effects of climate change on CBO’s projections of economic growth, see Appendix C.)

In CBO’s projections, revenues fall as climate change reduces output. The effects on spending are more complex. For instance, spending on Medicare and other health programs is expected to rise amid an increase in climate-related health conditions, such as illnesses related to heat exposure or air pollution and injuries related to storms, floods, and wildfires. Conversely, spending on health care programs would decline to the extent that participants died at younger ages than they otherwise would have or illnesses related to cold exposure decreased.9 Climate change could also prompt lawmakers to increase spending on discretionary programs, such as programs that provide disaster relief or repair and rebuild military facilities that would be damaged by increasingly frequent or severe storms.

1. The long-term budget projections in this report are based on CBO’s May 2023 baseline projections but also reflect the estimated budgetary effects of the Fiscal Responsibility Act of 2023 (Public Law 118-5), enacted on June 3, 2023. See Congressional Budget Office, How the Fiscal Responsibility Act of 2023 Affects CBO’s Projections of Federal Debt (June 2023), www.cbo.gov/publication/59235; letter to the Honorable Kevin McCarthy providing CBO’s estimate of the budgetary effects of H.R. 3746, the Fiscal Responsibility Act of 2023 (May 30, 2023), www.cbo.gov/publication/59225; and An Update to the Budget Outlook: 2023 to 2033 (May 2023), www.cbo.gov/publication/59096.

2. Debt held by the public is a measure that indicates the extent to which federal borrowing affects the availability of private funds for other borrowers. All else being equal, an increase in government borrowing reduces the amount of money available to other borrowers, putting upward pressure on interest rates and reducing private investment. It is the measure of debt that CBO uses most often in its reports on the budget.

3. For more details on federal debt and the consequences of its growth, see Congressional Budget Office, Federal Debt: A Primer (March 2020), www.cbo.gov/publication/56165.

4. Some people might also expect policymakers to raise taxes or cut spending to cover the cost of the additional debt, and they might increase their saving to prepare for paying higher taxes or receiving less in benefits. See Jonathan Huntley, The Long-Run Effects of Federal Budget Deficits on National Saving and Private Domestic Investment, Working Paper 2014-02 (Congressional Budget Office, February 2014), www.cbo.gov/publication/45140.

5. See Congressional Budget Office, Effects of Physical Infrastructure Spending on the Economy and the Budget Under Two Illustrative Scenarios (August 2021), www.cbo.gov/publication/57327, and The Macroeconomic and Budgetary Effects of Federal Investment (June 2016), www.cbo.gov/publication/51628.

6. Whereas GDP is the value of all final goods and services produced within U.S. borders (whether the labor and capital used to produce them are supplied by residents or nonresidents), GNP is the value of all final goods and services produced with U.S. residents’ labor and capital (either domestically or abroad).

7. The net effect on national income of a reduction in purchases of federal debt by foreign investors is unclear. When foreign holdings of U.S. debt decline, interest payments to foreign investors decrease. That leads to an increase in net international income as national income rises. However, that increase in net international income is offset by decreases resulting from higher interest rates.

8. For the agency’s latest demographic projections, see Congressional Budget Office, The Demographic Outlook: 2023 to 2053 (January 2023), www.cbo.gov/publication/58612.

9. See Congressional Budget Office, Budgetary Effects of Climate Change and of Potential Legislative Responses to It (April 2021), www.cbo.gov/publication/57019.

Chapter 2Spending and Revenues

Overview

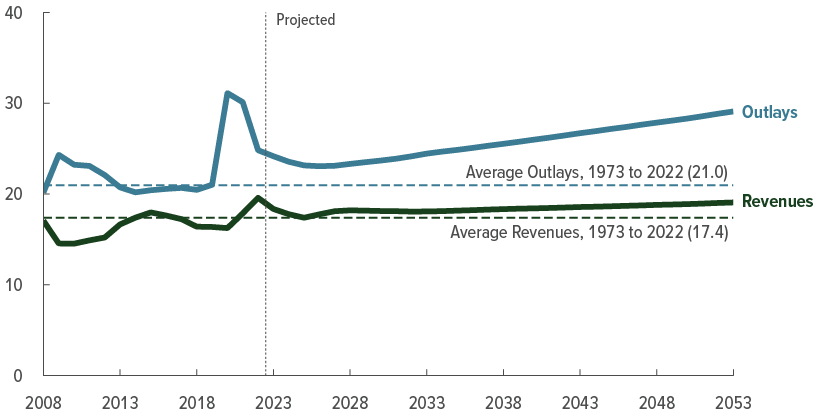

Under current law, federal spending is projected to represent a larger percentage of the nation’s gross domestic product (GDP) in coming years than it did, on average, during the past 50 years. From 1973 to 2022, total federal outlays averaged 21.0 percent of GDP; over the 2023–2053 period, projected outlays average 25.7 percent of GDP (see Figure 2-1).

Figure 2-1.

Total Outlays and Revenues

Percentage of Gross Domestic Product

In most years, growth in outlays is projected to outpace growth in revenues, resulting in widening budget deficits.

Data source: Congressional Budget Office. See www.cbo.gov/publication/59014#data.

In the Congressional Budget Office’s projections, outlays amount to 24.2 percent of GDP in 2023—less than the 24.8 percent recorded in 2022—as federal spending in response to the coronavirus pandemic continues to wane.1 Outlays continue to decrease through 2026 but steadily increase thereafter for three reasons: Rising interest rates and growing federal debt boost net interest costs; the growing cost of health care and the increase in the average age of the population boost spending on the major health care programs; and that same demographic trend increases spending on Social Security. Total spending reaches 24.4 percent of GDP in 2033 and continues to rise to 29.1 percent in 2053. Spending in the United States has exceeded that level in only two periods—for a three-year span during World War II and for two years amid the coronavirus pandemic. From 1943 to 1945, when defense expenditures increased sharply, total federal spending topped 40 percent of GDP. In 2020 and 2021, pandemic-related spending boosted total outlays to roughly 31 percent of GDP.

Over the 2023–2053 period, revenues measured as a percentage of GDP are projected to be higher than they have been, on average, in recent decades. Revenues averaged 17.4 percent of GDP over the past 50 years. Over the next 30 years, projected revenues average 18.4 percent of GDP.

CBO develops its extended baseline projections according to certain assumptions, some of which are specified in law. For a description of the assumptions underlying the projections, see Appendix A.

Spending

Total spending comprises mandatory and discretionary spending, as well as net outlays for interest.2 In CBO’s projections:

- Mandatory spending measured in relation to the size of the economy initially decreases through 2026 (to 14.0 percent of GDP) as pandemic-related mandatory outlays continue to decline. Mandatory spending then rises steadily to 16.9 percent of GDP in 2053, largely driven by growth in outlays for the major health care programs.

- Discretionary outlays amount to 6.5 percent of GDP in 2023, decline to 5.4 percent by 2037, and then are assumed to remain constant (as a percentage of GDP) through 2053 (see Figure 2-2).

- Net outlays for interest increase significantly during that period—from 2.5 percent of GDP in 2023 to 6.7 percent in 2053. If such outlays followed their projected path, they would exceed all mandatory spending other than that for the major health care programs and Social Security by 2027, all discretionary outlays by 2047, and all spending on Social Security by 2051.

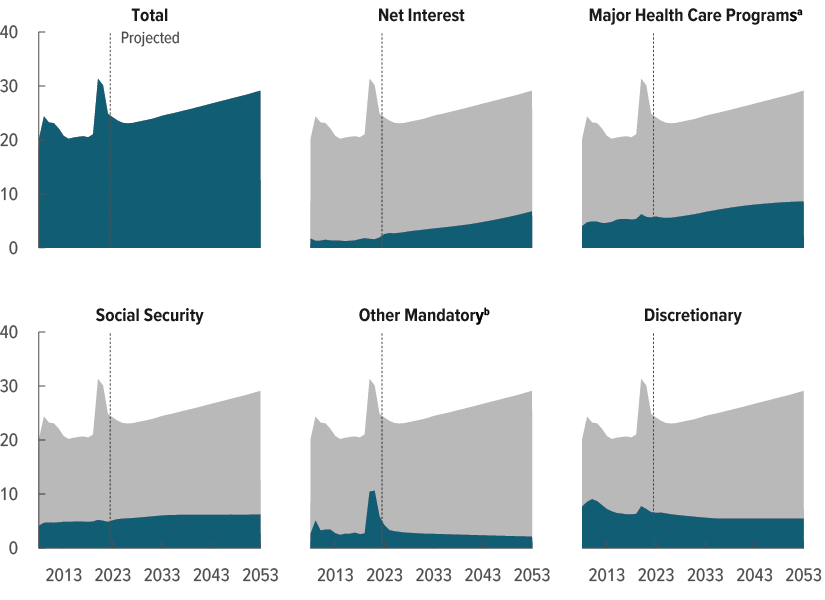

Figure 2-2.

Outlays, by Category

Percentage of GDP

Over the long term, net outlays for interest and spending on the major health care programs and Social Security are projected to rise in relation to GDP; other spending, in total, is projected to decline.

Data source: Congressional Budget Office. See www.cbo.gov/publication/59014#data.

GDP = gross domestic product.

a. Consists of spending on Medicare (net of premiums and other offsetting receipts), Medicaid, and the Children’s Health Insurance Program, as well as outlays to subsidize health insurance purchased through the marketplaces established under the Affordable Care Act and related spending.

b. Consists of all mandatory spending other than that for Social Security and the major health care programs. “Other Mandatory” includes the refundable portions of the earned income tax credit, the child tax credit, and the American Opportunity Tax Credit.

CBO projects that by 2053, growth in outlays for the major health care programs and for interest would reshape the spending patterns of the U.S. government (see Figure 2-3). Net interest costs would account for a much greater portion of total federal spending in 2053 than in 2023, as would spending on the major health care programs.

Figure 2-3.

Composition of Outlays, 2023 and 2053

Percent

Under current law, net outlays for interest would account for a greater portion of total federal outlays in 2053 than they will in 2023, and spending on the major health care programs would account for a much larger share of all federal noninterest spending.

Data source: Congressional Budget Office. See www.cbo.gov/publication/59014#data.

a. Consists of all mandatory spending other than that for Social Security and the major health care programs. “Other Mandatory” includes the refundable portions of the earned income tax credit, the child tax credit, and the American Opportunity Tax Credit.

b. Consists of spending on Medicare (net of premiums and other offsetting receipts), Medicaid, and the Children’s Health Insurance Program, as well as outlays to subsidize health insurance purchased through the marketplaces established under the Affordable Care Act and related spending.

Mandatory Spending

In CBO’s extended baseline projections, the growth in mandatory spending is driven by increased spending on the major health care programs and, especially in the first decade, on Social Security. Other mandatory spending declines in relation to GDP over the next 30 years, particularly in the first decade of the period.3 Spending on the major health care programs climbs largely because, in CBO’s estimation, health care costs per person will continue to rise. The aging of the population also contributes to growth in spending on health care programs and on Social Security. In 2023, outlays for Social Security, Medicare, and Medicaid, for people age 65 or older, amount to less than 30 percent of all federal noninterest spending; but in 2053, such outlays amount to more than 40 percent of all noninterest spending.

Major Health Care Programs. The major health care programs consist of Medicare, Medicaid, the Children’s Health Insurance Program (CHIP), and subsidies for health insurance purchased through the marketplaces established under the Affordable Care Act.4 Spending on Medicare, which provides health insurance to roughly 65 million people (86 percent of whom are at least 65 years old), will account for over half of all spending on those programs in 2023 and over 60 percent of it in 2053, CBO projects.

Over the past five decades, spending on the major health care programs has grown faster than the economy—a trend that persists in CBO’s projections. Net federal spending on those programs amounts to 5.8 percent of GDP in 2023 and increases to 8.6 percent in 2053.

The primary driver of that increase is spending on Medicare. Such spending (net of offsetting receipts, which are mostly premiums paid by enrollees) grows as a share of GDP by 2.4 percentage points during the period, reaching 5.5 percent of GDP in 2053 (see Figure 2-4). The growth in Medicare spending over the next three decades stems largely from rising health care costs per person and demographic trends. As a share of GDP, spending on the other major health care programs—Medicaid and CHIP, combined with subsidies for health insurance purchased through the marketplaces established under the Affordable Care Act and related spending—grows by 0.4 percentage points over the next three decades, reaching 3.1 percent of GDP in 2053.

Figure 2-4.

Composition of Outlays for the Major Health Care Programs

Percentage of Gross Domestic Product

Spending on Medicare is projected to account for more than four-fifths of the increase in spending on the major health care programs over the next 30 years.

Data source: Congressional Budget Office. See www.cbo.gov/publication/59014#data.

CHIP = Children’s Health Insurance Program.

a. Net of premiums and other offsetting receipts.

b. “Marketplace Subsidies” refers to outlays to subsidize health insurance purchased through the marketplaces established under the Affordable Care Act and related spending.

The Hospital Insurance (HI) Trust Fund is used to pay for benefits under Medicare Part A, which covers inpatient hospital services, care provided in skilled nursing facilities, home health care, and hospice care.5 The HI trust fund derives income from several sources but mainly from the Medicare payroll tax. One measure of the sustainability of Part A is the projected timing of the HI trust fund’s exhaustion. In CBO’s projections, the fund’s balance generally increases through 2029, after which time expenditures begin to outstrip income. As a result, the HI trust fund would be exhausted in 2035.

Once the HI trust fund was exhausted, total payments to health plans and providers for services covered under Part A would be limited to the amount of revenues subsequently credited to the fund. It is unclear what changes the Centers for Medicare & Medicaid Services could make in order to operate the Part A program under those circumstances.6

Another measure of the sustainability of the HI trust fund is its actuarial balance, which summarizes the fund’s current balance and annual future streams of revenues and outlays as a single number.7 (A negative actuarial balance is called an actuarial deficit.) In CBO’s projections, the HI trust fund’s 25-year actuarial deficit amounts to 0.6 percent of taxable payroll (or 0.3 percent of GDP). In other words, the government could pay for the services prescribed by current law and maintain the necessary trust fund balance through 2047 if the HI payroll tax rate, which is currently 2.9 percent, was raised immediately and permanently by 0.6 percentage points. Other ways to maintain the necessary trust fund balance include reducing payments by an amount equivalent to 0.6 percent of taxable payroll, combining tax increases with payment reductions, or transferring money to the trust fund.

Social Security. In CBO’s projections, spending on Social Security generally increases as a percentage of GDP over the next 30 years, continuing the trend of the past five decades. The number of Social Security beneficiaries rises from 67 million (or about 20 percent of the population) in 2023 to 79 million in 2033 and then to 97 million (or over 25 percent of the projected population) in 2053. Spending on the program increases from 5.1 percent of GDP in 2023 to 6.0 percent in 2033. That growth continues but slows along with the pace of the aging of the population, as members of the large baby-boom generation die and people from younger and smaller generations become eligible for Social Security; spending on Social Security reaches 6.2 percent of GDP in 2053.8

The Social Security program is funded by dedicated tax revenues from two sources. Currently, 96 percent of the funding comes from a payroll tax on earnings up to a certain limit; the rest is collected from an income tax on Social Security benefits. Revenues from the payroll tax and the income tax on benefits are credited to the Old-Age and Survivors Insurance (OASI) Trust Fund and the Disability Insurance (DI) Trust Fund, which finance the program’s benefits. In CBO’s extended baseline projections, dedicated tax revenues for the combined trust funds decline from 4.6 percent of GDP in 2023 to 4.4 percent in 2053. The decline occurs in part because projected earnings grow faster for high earners than for low earners, so a larger share of earnings exceeds the maximum taxable amount for Social Security and a smaller share is taxable.

A commonly used measure of Social Security’s financial position is the dates by which the trust funds would be exhausted.9 CBO projects that the OASI trust fund would be exhausted in fiscal year 2032 and the DI trust fund would be exhausted in calendar year 2052. If their balances were combined, the Old-Age, Survivors, and Disability Insurance (OASDI) trust funds would be exhausted in fiscal year 2033. CBO estimated the amounts by which annual benefits would have to be reduced for the trust funds’ outlays to match their revenues in each year after the combined trust funds were exhausted. Benefits would need to be reduced (in relation to CBO’s baseline projections) by 25 percent in 2034, an amount that would climb to 28 percent in 2053.

Other Mandatory Programs. Before the pandemic, mandatory spending excluding outlays for the major health care programs and Social Security had generally remained between 2 percent and 4 percent of GDP since the mid-1960s (it was 2.7 percent of GDP in 2019, for example). Such spending includes outlays for the Supplemental Nutrition Assistance Program (SNAP), unemployment compensation, retirement programs for federal civilian and military employees, certain programs for veterans, Supplemental Security Income, and certain refundable tax credits.10 That spending increased significantly in 2020 and 2021—to 10.4 percent and 10.6 percent of GDP, respectively—mainly because of policies enacted in response to the pandemic and related economic downturn. As spending associated with those policies decreased, outlays for the category “other mandatory programs” fell to 5.8 percent of GDP in 2022.

In CBO’s projections, spending on other mandatory programs totals 4.2 percent of GDP in 2023. It then declines as a share of the economy, falling to 2.6 percent of GDP in 2033 and 2.1 percent in 2053.11 The projected decline through 2033 occurs in part because the amounts of benefits for many of the programs are adjusted for inflation each year—and in CBO’s economic forecast, inflation is projected to be less than the rate of growth in nominal GDP (that is, GDP measured in current-year dollars). The decline from 2033 to 2053 is partly attributable to rising income, which decreases the number of people who qualify for refundable tax credits (in turn decreasing the government’s outlays for those credits). Over that period, outlays for the remainder of other mandatory programs are assumed to decline as a percentage of GDP at roughly the same annual rate at which they are projected to decline between 2030 and 2033.

Causes of Growth in Mandatory Spending. Rising health care costs per person and the aging of the population are the main reasons for the sharp increase in projected spending on the major health care programs over the next 30 years. The aging of the population also leads to an increase in spending on Social Security.

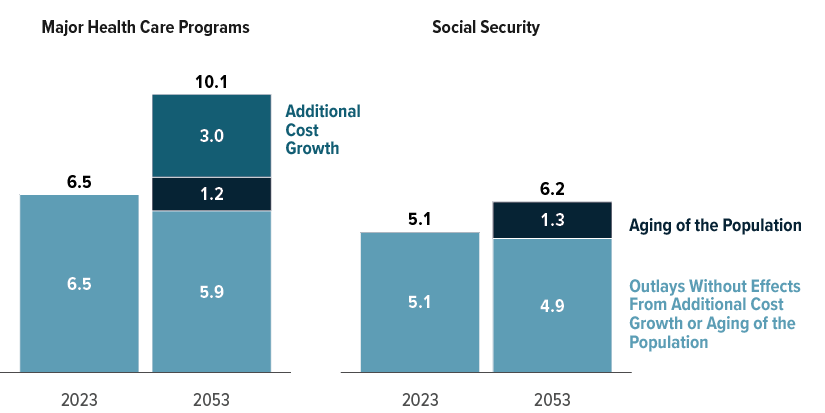

CBO assessed the combined effects of those two factors by projecting what would occur over the 2023–2053 period if health care costs per person (adjusted for demographic changes) grew at the rate of potential GDP per person—which would mean that costs grew more slowly than the agency currently projects—and the average age of the population was not increasing. Under those scenarios, spending on the major health care programs would be 5.9 percent of GDP in 2053, or 0.6 percentage points lower than the agency currently projects for 2023.12 And if the effects of the aging of the population alone were excluded, then spending on Social Security would be 4.9 percent of GDP in 2053, 0.2 percentage points lower than the agency projects for 2023 (see Figure 2-5).13

Figure 2-5.

Composition of Growth in Outlays for the Major Health Care Programs and Social Security, 2023 to 2053

Percentage of GDP

Growth in spending on the major health care programs is largely driven by cost growth above and beyond that accounted for by demographic changes or the growth of potential GDP per person. Spending on those programs, as well as spending on Social Security benefits, is also boosted by the aging of the population.

Data source: Congressional Budget Office. See www.cbo.gov/publication/59014#data.

The spending on the major health care programs examined here consists of gross spending on Medicare (which does not account for premiums or other offsetting receipts), Medicaid, and the Children’s Health Insurance Program, as well as outlays to subsidize health insurance purchased through the marketplaces established under the Affordable Care Act and related spending.

Additional cost growth is the extent to which the growth rate of nominal health care spending per person (adjusted for demographic changes) exceeds the growth rate of potential GDP per person. Potential GDP is the maximum sustainable output of the economy.

GDP = gross domestic product.

Rising Health Care Costs per Person. The average growth rate of federal health care spending per beneficiary has slowed in recent years, from 5.6 percent over the 1988–2005 period to 2.2 percent from 2007 to 2019. However, over the second and third decades of the projection period, such costs (adjusted for demographic changes) continue to increase faster than the 3.3 percent growth rate of potential GDP per person—1.0 percent faster for Medicare and 1.1 percent faster for Medicaid, on average. That growth in health care costs per person accounts for over two-thirds of the increase in spending, measured as a percentage of GDP, on the major health care programs between 2023 and 2053.

Aging of the Population. Over the 2023–2053 period, about one-third of the projected increase in total spending on the major health care programs, measured as a percentage of GDP, is attributable to the aging of the population. The lion’s share of the increase results from greater spending on Medicare because Medicare is the largest of those programs and most beneficiaries qualify for it at age 65. (See Figure 3-2 for CBO’s projections of the population by age group.)14 As the group of people who qualify for Medicare becomes larger and, on average, older, Medicare spending will grow, not only because of the greater number of beneficiaries but also because spending on health care tends to increase as people age.

From 2023 to 2053, all of the projected increase in spending on Social Security, measured as a percentage of GDP, is attributable to the aging of the population. The effects of that aging, which push spending on Social Security up, are partially offset by scheduled increases in the full retirement age for Social Security, which reduce the lifetime benefits for affected beneficiaries and thus push spending down.15 (In fact, if the population was not aging, then outlays for Social Security over the 2023–2053 period would decrease as a percentage of GDP.)

Discretionary Spending

In CBO’s long-term projections, discretionary outlays through 2033 follow the agency’s 10-year baseline projections adjusted to reflect the estimated budgetary effects of the Fiscal Responsibility Act of 2023 (Public Law 118-5). From 2023 to 2033, in CBO’s projections, about 49 percent of all discretionary outlays, on average, are dedicated to national defense. The rest are for nondefense discretionary spending, which comprises outlays for an array of federally funded activities and programs.

After 2033, discretionary outlays are assumed to transition (over a five-year period) to grow at the rate of nominal GDP. As a result, such outlays generally decrease as a percentage of GDP—falling from 6.5 percent in 2023 to 5.4 percent in 2037 and remaining at that level through 2053.

Net Outlays for Interest

Over the past 50 years, the government’s net interest costs have ranged from 1.2 percent of GDP to 3.2 percent, averaging 2.0 percent of GDP. In CBO’s projections, such costs amount to 2.5 percent of GDP in 2023. By 2033, those costs increase to 3.6 percent of GDP, as federal debt grows and interest rates rise. Net outlays for interest continue to increase thereafter, reaching 6.7 percent of GDP in 2053. They would be higher (as a percentage of GDP) in that year than spending on Social Security, discretionary outlays, or all mandatory spending other than that for the major health care programs and Social Security—and more than twice the highest amount observed since at least 1940 (the first year for which the Office of Management and Budget reports such data).

The projected increase in net outlays for interest is the result of escalating interest rates and the rising amount of debt. On average, in CBO’s projections, increases in the average interest rate account for about two-thirds of the rise in net interest costs over the 2023–2053 period.16

Revenues

In CBO’s projections, revenues measured as a percentage of GDP fluctuate over the next decade, declining through 2025 but increasing thereafter because of scheduled changes to tax provisions. Revenues rise steadily from 2033 to 2053, mainly because growth in income boosts receipts from the individual income tax. Measured in relation to the size of the economy, revenues are higher in each year of the next three decades than their average over the past 50 years.17

Projected Revenues

In CBO’s projections, total revenues amount to 18.4 percent of GDP in 2023, down from 19.6 percent last year. Revenues continue to decline through 2025 as the effects of temporary factors that boosted tax receipts in 2021 and 2022 (such as strong collections of taxes on capital gains realizations) subside. In 2026 and 2027, by contrast, revenues rise in relation to GDP because of changes to provisions governing the individual income tax that are scheduled to occur at the end of calendar year 2025.

From 2023 to 2053, total revenues measured as a percentage of GDP grow by nearly one percentage point in CBO’s projections, reaching 19.1 percent of GDP by the end of the period. That growth is mainly driven by an increase in individual income tax receipts that is partially offset by decreases in other revenues. Although receipts of individual income taxes initially fall, they resume their growth after 2025 and amount to 10.7 percent of GDP in 2053—one percentage point higher than their value in 2023 (see Figure 2-6). That growth in receipts from individual income taxes is partially offset by declining receipts from corporate income taxes and payroll taxes over the next three decades (by 0.4 percentage points and 0.2 percentage points, respectively).

Figure 2-6.

Revenues, by Source

Percentage of GDP

Measured as a percentage of GDP, total revenues grow by about one percentage point from 2023 to 2053, in CBO’s projections, mainly driven by an increase in individual income tax receipts. Receipts from payroll and corporate taxes, measured as a share of the economy, decline by a small amount over the 30-year period.

Data source: Congressional Budget Office. See www.cbo.gov/publication/59014#data.

GDP = gross domestic product.

a. Consists of excise taxes, remittances to the Treasury from the Federal Reserve System, customs duties, estate and gift taxes, and miscellaneous fees and fines.

Factors Affecting Revenues

The projected increase in total revenues, measured as a percentage of GDP, over the next 30 years stems from several factors, including real bracket creep and scheduled changes to tax provisions. Those factors are partially offset by others that cause revenues to decrease, including the end of a temporary boost to tax receipts, growing health care costs, and a decline in receipts from the corporate income tax (see Figure 2-7). Faster earnings growth for higher-earning people increases individual income taxes but decreases payroll taxes by nearly the same amount, affecting net revenues little over the long term.

Figure 2-7.

Key Factors Contributing to Changes in Revenues

Percentage of GDP

The largest source of growth in tax revenues over the long term is real bracket creep—the process in which, as income rises faster than prices, a larger proportion of income becomes subject to higher tax rates.

After 2025, another significant source of growth in revenues is the scheduled expiration of certain provisions of the 2017 tax act.

Several other factors affect projected revenues. In 2023, for example, revenues fall as a percentage of GDP as the temporary boost to tax receipts observed in 2021 and 2022 ends.

Data source: Congressional Budget Office. See www.cbo.gov/publication/59014#data.

GDP = gross domestic product.

a. Real bracket creep is the process in which, as income rises faster than inflation, a larger proportion of income becomes subject to higher tax rates, even when the underlying distribution of income remains unchanged.

b. Other factors include an end to the temporary boost to tax receipts as recent strength in collections dissipates, as well as factors that affect revenues over the longer term, such as changes in the distribution of wages and growth in nontaxable compensation resulting from rising health care costs.

Real Bracket Creep. The income thresholds for the various tax rate brackets in the individual income tax are indexed to increase with inflation (as measured by the chained consumer price index for all urban consumers, published by the Bureau of Labor Statistics). In CBO’s projections, nominal income grows faster than prices, so more income is pushed into higher tax brackets even when the underlying distribution of income remains unchanged. That process is known as real bracket creep and is the largest source of growth in total projected revenues over the next three decades.

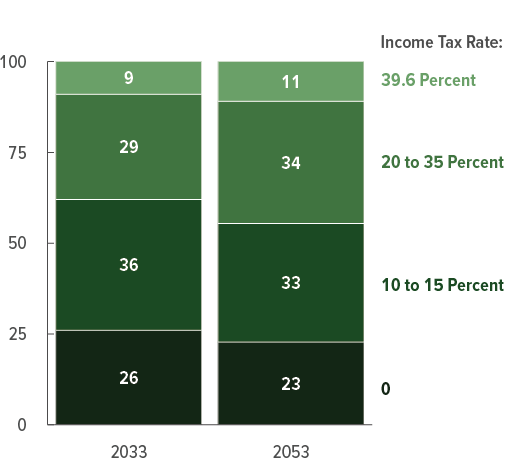

If current laws generally remained unchanged, real bracket creep would continue to gradually boost taxes in relation to income through 2053, CBO projects, thereby increasing tax receipts. From 2033 to 2053, the share of income in the highest income bracket (taxed at the top rate of 39.6 percent) would rise by 2 percentage points, and the share of income excluded from taxation (mostly because of exemptions and deductions) would fall by 3 percentage points—because of real bracket creep (see Figure 2-8).18

Figure 2-8.

Shares of Income Taxed at Different Rates Under the Individual Income Tax System

Percent

The largest contributor to growth in projected revenues over the long term is real bracket creep—the process in which, as income rises faster than prices, a larger proportion of income becomes subject to higher tax rates. As the share of income taxed at higher rates grows, the share exempt from taxation shrinks.

Data source: Congressional Budget Office. See www.cbo.gov/publication/59014#data.

In this figure, income refers to adjusted gross income—that is, income from all sources not specifically excluded by the tax code, minus certain deductions. The income tax rate is the statutory rate specified under the individual income tax system. The lowest statutory tax rate is zero (because of deductions and exemptions).

Scheduled Changes to Tax Provisions After 2025. Under current law, nearly all the provisions of the 2017 tax act (P.L. 115-97) affecting the individual income tax are scheduled to expire at the end of calendar year 2025. In CBO’s projections, the resulting changes, taken together, boost tax revenues in relation to income. Once in effect, the scheduled changes would bring about higher statutory tax rates, a smaller standard deduction, the return of personal exemptions, and a reduction in the child tax credit. Those changes would cause tax liabilities (the amounts taxpayers owe) to rise beginning in calendar year 2026, pushing up receipts in fiscal year 2026 and beyond. CBO projects that after 2025, the scheduled changes would boost individual income tax revenues, measured as a share of GDP, by 0.8 percentage points, on average.

Other Factors. Several other factors affect projected revenues. One is the end of a temporary boost to tax receipts observed in 2021 and 2022, which reflects CBO’s expectation that the recent strength in tax collections from capital gains realizations and other sources will not continue. In addition, payments of certain taxes deferred during the first two years of the pandemic will mostly have been collected by the end of 2023. Taken together, the end of the temporary boost to tax receipts and the windup of deferred tax payments produce a drop in revenues that persists throughout the projection period.

The second factor is the growth in health care costs, which is projected to reduce revenues as a percentage of GDP over the next three decades. The share of employees’ compensation that is paid in the form of spending on fringe benefits, such as employment-based health insurance, is projected to increase, and those benefits are generally not taxable. Correspondingly, the share of employees’ compensation that is paid in the form of wages and salaries, which are subject to income and payroll taxes, is projected to decline. That shift in compensation would decrease taxable income—and thus revenues from both income and payroll taxes—in relation to GDP.

The third factor is the change in the distribution of earnings. Earnings are projected to continue to grow faster for higher-earning people than for other people in the long term. That trend would cause a larger share of individual earnings to be taxed at higher rates. However, the resulting increase in individual income tax revenues would be largely offset by a decrease of nearly the same amount in payroll tax receipts, CBO projects, because the share of earnings above the maximum amount subject to Social Security payroll taxes would grow.19

A final factor is a decline in corporate income tax receipts, which fall in relation to the size of the economy between 2023 and 2033. That decline reflects the varying effects, over time, of provisions of the 2017 tax act and the 2022 reconciliation act (P.L. 117-169). Those provisions include the end of payments for a onetime tax on certain foreign profits, changes to the treatment of certain expenditures for research and experimentation, and new credits that can be used to reduce liability in excess of a new minimum tax on certain corporations.

1. The long-term budget projections in this report are based on CBO’s May 2023 baseline projections but also reflect the estimated budgetary effects of the Fiscal Responsibility Act of 2023 (FRA, Public Law 118-5), enacted on June 3, 2023. Other legislation enacted between March 30, 2023 (when CBO finalized its May baseline), and June 3, 2023, did not have significant budgetary effects. The projections are consistent with the demographic projections that the agency published on January 24, 2023, and the economic forecast that it published on February 15, 2023. They do not reflect the economic effects of administrative actions, regulatory changes, legislation, or economic developments after December 6, 2022, when that economic forecast was finalized. Nor do they reflect the budgetary effects of any developments after March 30, 2023, except for the enactment of the FRA.

2. Mandatory spending includes outlays for most federal benefit programs and for certain other payments to people, businesses, nonprofit institutions, and state and local governments. Such outlays are generally governed by statutory criteria and are not normally constrained by the annual appropriation process. Discretionary spending encompasses an array of federal activities funded through or controlled by appropriations. That category includes most defense spending and spending for many nondefense activities, such as elementary and secondary education, housing assistance, international affairs, the administration of justice, and highway programs. In the federal budget, net outlays for interest consist of the government’s interest payments on federal debt, offset by interest income that the government receives.

3. For a more detailed discussion of outlays from 2023 to 2033, see Congressional Budget Office, An Update to the Budget Outlook: 2023 to 2033 (May 2023), www.cbo.gov/publication/59096, The Budget and Economic Outlook: 2023 to 2033 (February 2023), www.cbo.gov/publication/58848, and How the Fiscal Responsibility Act of 2023 Affects CBO’s Projections of Federal Debt (June 2023), www.cbo.gov/publication/59235.

4. Federal subsidies for health insurance for low- and moderate-income households account for most of the outlays for subsidies for insurance purchased through the marketplaces and related spending. The related spending consists almost entirely of payments for risk adjustment (which are financed by funds collected from insurers with healthier enrollees and made to health insurers whose enrollees are in poorer health) and spending for the Basic Health Program (an optional state program that covers low-income residents outside the health insurance marketplaces).

5. Medicare’s second trust fund, the Supplementary Medical Insurance (SMI) Trust Fund, is used to pay for outpatient services (including physicians’ services) and prescription drugs under Parts B and D of the program. The SMI Trust Fund differs from the HI Trust Fund in that most of its income does not come from a specified set of revenues collected from the public. Rather, most of the SMI fund’s income is in the form of transfers from the general fund of the Treasury, which are automatically adjusted to cover the differences between the program’s spending and specified revenues. Thus, the balance in the SMI fund cannot be exhausted.

6. CBO’s projections reflect the assumption that Medicare and Social Security will continue to pay benefits as scheduled under current law, regardless of the status of the programs’ trust funds. That approach is consistent with a statutory requirement that CBO’s 10-year baseline projections reflect the assumption that funding for such programs is adequate to make all payments required by law. See sec. 257(b)(1) of the Balanced Budget and Emergency Deficit Control Act of 1985, P.L. 99-177 (codified at 2 U.S.C. §907(b)(1) (2016)).

7. The actuarial balance is the sum of the present value of projected income and the current trust fund balance minus the sum of the present value of projected outlays and a year’s worth of benefits at the end of the period. (The present value expresses a flow of current and future income or payments in terms of an equivalent lump sum received or paid today.) For the HI trust fund, that difference is presented in this report as a percentage of the present value of taxable payroll or of GDP over 25 years.

8. In CBO’s projections, spending on Social Security continues as scheduled regardless of the amounts in the program’s trust funds. The baby-boom generation comprises people born between 1946 and 1964.

9. Another commonly used measure of Social Security’s financial position is the program’s actuarial balance, often measured over 75 years. See Congressional Budget Office, CBO’s 2023 Long-Term Projections for Social Security (forthcoming, June 2023), www.cbo.gov/publication/59184.

10. Refundable tax credits reduce a filer’s overall income tax liability; if the credit exceeds the filer’s income tax liability, the government pays all or some portion of that excess to the taxpayer (and the payment is treated as an outlay in the budget). For more information, see Congressional Budget Office, Refundable Tax Credits (January 2013), www.cbo.gov/publication/43767.

11. Sec. 257(b)(2) of the Balanced Budget and Emergency Deficit Control Act of 1985, which governs CBO’s baseline projections, makes exceptions regarding current law for some programs, such as SNAP, that have expiring authorizations but that are assumed to continue as currently authorized.

12. Potential GDP is the maximum sustainable output of the economy. The analysis of the causes of the growth in spending on the major health care programs encompasses gross spending on Medicare and does not reflect receipts credited to the program from premiums and other sources.

13. In this report, the term “additional cost growth” describes the amount by which the growth rate of nominal health care spending per person (adjusted to remove the effects of demographic changes) exceeds the growth rate of potential GDP per person. To assess how additional cost growth would affect spending on the major health care programs and how the aging of the population would affect such spending as well as outlays for Social Security, CBO produced estimates using three scenarios: In the first scenario, the age distribution of the population matched that in 2023 and additional cost growth was held at zero. In the second scenario, the agency projected the effect of the aging of the population while holding additional cost growth at zero. And in the third scenario, it projected the effects of the aging of the population and additional cost growth. To determine how the aging of the population would affect projected outlays for the major health care programs and Social Security, CBO then compared the result of the second scenario with that of the first scenario; and to determine how additional cost growth would affect projected spending on the major health care programs, the agency compared the result of the third scenario with that of the second scenario.

14. In this report, population refers to the Social Security area population, which includes all residents of the 50 states and of the District of Columbia, as well as civilian residents of U.S. territories. It also includes federal civilian employees and members of the U.S. armed forces living abroad and their dependents, U.S. citizens living abroad, and noncitizens living abroad who are eligible for Social Security benefits on the basis of their earnings while in the United States.

15. For more details about the full retirement age for Social Security, see Zhe Li, The Social Security Retirement Age, Report R44670, version 14 (Congressional Research Service, July 6, 2022), https://tinyurl.com/yndurmpa.

16. To determine the change in net interest costs separately attributable to primary deficits (that is, deficits excluding net outlays for interest) and to changes in the average interest rate, CBO started with a benchmark scenario. In that scenario, after 2022, the average interest rate did not change and there were no primary deficits adding to the amount of debt. The agency then estimated the effect on net interest costs from primary deficits (by estimating those deficits without a change in the average interest rate) and from the change in the average interest rate (by estimating those rates without primary deficits). The relative size of those estimates was then used to calculate the percentage of the total increase in net interest costs attributable to the increase in the average interest rate and to primary deficits by proportionally allocating the interaction between the average interest rate and the primary deficit.

17. CBO’s revenue projections are based on the assumption that the rules for all tax sources (individual income taxes, corporate income taxes, payroll taxes, and other taxes) will change as scheduled under current law. The sole exception is expiring excise taxes dedicated to trust funds. The Balanced Budget and Emergency Deficit Control Act of 1985 requires that CBO’s baseline reflect the assumption that those taxes would be extended at their current rates. That law does not stipulate that the baseline include the extension of other expiring tax provisions, even if lawmakers have routinely extended them in the past.

18. For more details, see Congressional Budget Office, “How Income Growth Affects Tax Revenues in CBO’s Long-Term Budget Projections” (June 2019), www.cbo.gov/publication/55368.

19. For additional information, see Brooks Pierce, How Changes in the Distribution of Earnings Affect the Federal Deficit, Working Paper 2021-12 (Congressional Budget Office, October 2021), www.cbo.gov/publication/57217.

Chapter 3Long-Term Demographic and Economic Projections

Overview