The Economic Effects of Waiting to Stabilize Federal Debt

CBO analyzes the economic effects of waiting to stabilize federal debt. The longer action is delayed, the larger the policy changes needed to stabilize debt. The timing and type of policy would determine its effects on different age and income groups.

Summary

Under current law, the growth of federal noninterest spending and net outlays for interest on federal debt would outpace the increase in revenues over the next 30 years, the Congressional Budget Office projects. As a percentage of gross domestic product (GDP), federal debt held by the public is thus projected to climb from 102 percent at the end of 2021 to 202 percent in 2051. A perpetually rising debt-to-GDP ratio is unsustainable over the long term because financing deficits and servicing the debt would consume an ever-growing proportion of the nation’s income.

In this report, CBO analyzes the effects of measures that policymakers could take to prevent debt as a percentage of GDP from continuing to climb. Policymakers could restrain the growth of spending, raise revenues, or pursue some combination of those two approaches. Regardless of which method they chose, the policy change—and the timing of it—would directly affect the economy and the well-being of people.

Waiting to put fiscal policy on a sustainable course and allowing federal debt to continue to climb would have several effects on the economy. As federal borrowing increased, the amount of funds available for private investment would decline (a phenomenon known as crowding out), and interest costs would increase. Perpetually rising debt would also increase the likelihood of a fiscal crisis and pose other risks to the U.S. economy.

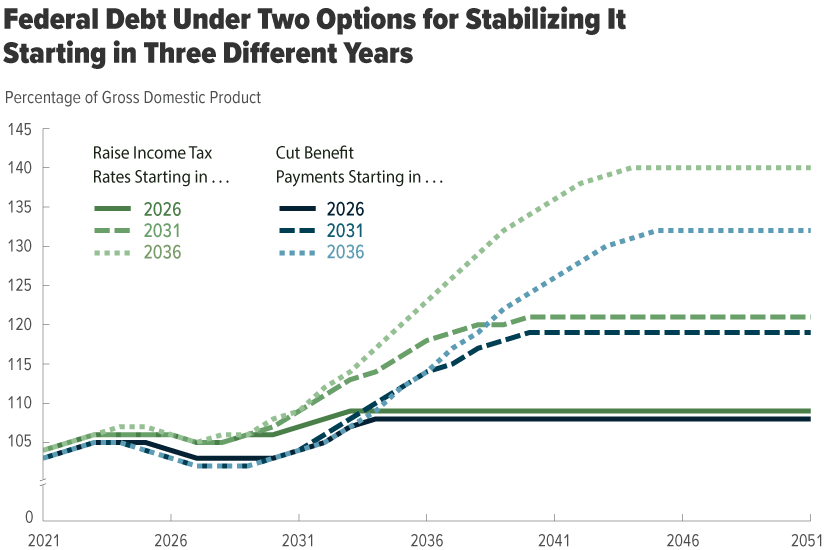

Many policy options are available to policymakers to stabilize debt as a percentage of GDP; for this analysis, CBO examined two simplified policies. The first would raise federal tax rates on different types of income proportionally. The second would cut spending for certain government benefit programs—mostly for Social Security, Medicare, and Medicaid. Under each of the two stylized policy options, debt as a percentage of GDP would be fully stabilized 10 years after the changes were implemented. CBO analyzed the effects of implementing the two options in three different years—2026, 2031, and 2036. To assess the effects of waiting to stabilize the debt 5 or 10 years, the agency calculated the differences in the estimated effects of implementing the policy changes in the two later years and implementing them in 2026.

CBO’s analysis yielded the following key findings:

- Regardless of when the process was begun, stabilizing federal debt as a percentage of GDP would require that income tax receipts or benefit payments change substantially from their currently projected path.

- The longer policymakers waited to implement a policy change, the more debt would grow in relation to GDP, and the greater the policy changes needed to stabilize it would be.

- If the option of increasing income tax rates was chosen, the effects of delaying implementation would be greater than they would be under the option of cutting benefits: Increases in interest costs would be larger, GDP and household consumption would be lower, and debt as a percentage of GDP would be higher in the long run.

- Under either option, the negative effects of delaying the implementation of policy changes on people’s consumption and labor supply would be disproportionately borne by younger people and lower-income people.