At a Glance

In 2019, federal spending for highways totaled $46 billion. Such spending is funded primarily by revenues credited to the Highway Trust Fund, which have fallen short of spending from the fund for more than a decade. If the taxes that are credited to the trust fund were continued at their current rates and funding for highway and transit programs increased annually at the rate of inflation, by 2030, the cumulative shortfall in the trust fund would reach $189 billion, according to the Congressional Budget Office’s latest baseline projections. (Those projections were prepared in March 2020, before the current public health emergency caused by the coronavirus began. The net effect that the crisis will have on that shortfall is unclear.)

In this report, CBO discusses choices about revenues and spending that lawmakers face in addressing that shortfall and improving the nation’s infrastructure; the agency also analyzes options for subsidizing state and local governments’ financing of highway projects.

- Revenues. To increase revenues, lawmakers could raise taxes on motor fuels. Increasing those taxes by 15 cents per gallon and indexing them to inflation would generate an estimated $329 billion more for the trust fund over 10 years than the amount projected to be raised at the current rates in CBO’s March baseline. Another option is to impose a new tax on vehicle miles traveled by trucks or on freight shipments carried by trucks. Such a tax could eventually reduce the shortfall markedly, but the costs to implement it and ensure compliance would be substantial. Finally, lawmakers could increase the Highway Trust Fund’s resources by continuing to transfer money from the Treasury’s general fund.

- Spending. Increasing highway spending from 2021 to 2030 to an annual average of $71 billion—nearly 40 percent more than projected in the baseline—could fund all highway projects that are estimated to provide a net benefit if state and local governments increased their spending proportionally. But doing so would double the cumulative shortfall through 2030. Alternatively, highway conditions could be maintained with average annual spending of $54 billion (if state and local governments increased their spending proportionally), which would increase the shortfall by $31 billion.

Much of the shortfall could be eliminated if federal highway funding were set to match projected revenues for the highway account of the trust fund. Average annual spending would fall to $39 billion, about 25 percent less than projected in the baseline. The cumulative shortfall through 2030 would shrink by $124 billion but would not be entirely eliminated because outlays would continue to be made from funding allocated before the cuts were made.

- Financing. The federal government could provide more subsidies to state and local governments to support their borrowing to pay for highway projects. Policymakers could broaden the availability of subsidies provided in existing financing programs (tax-preferred bonds, direct loans and loan guarantees, and funds to be used to capitalize state infrastructure banks), or they could authorize state and local governments to issue tax credit bonds.

Notes

Notes

All projections presented in this report are based on the Congressional Budget Office’s baseline budget projections as of March 6, 2020 (www.cbo.gov/publication/56268), and on the economic forecast that the agency published in January 2020 as part of The Budget and Economic Outlook: 2020 to 2030 (www.cbo.gov/publication/56020). Thus, they do not reflect changes to the nation’s economic outlook and fiscal situation arising from the recent and rapidly evolving public health emergency caused by the coronavirus.

Unless this report indicates otherwise, all years referred to are federal fiscal years, which run from October 1 to September 30 and are designated by the calendar year in which they end.

Dollar amounts are reported in nominal (current-year) dollars unless this report specifies otherwise. Where amounts are given in inflation-adjusted dollars, CBO used the gross domestic product price index from the Bureau of Economic Analysis to convert them.

Numbers in the text and tables may not add up to totals because of rounding.

Summary

Federal spending on highways (or, synonymously, roads) totaled $46 billion in 2019. Most of those outlays were for grants to state and local governments to support their spending on capital projects. (Those governments typically spend roughly three times as much of their own funds on highways each year, not only on capital projects but also to operate and maintain roads.) That $46 billion also includes spending for federal programs that subsidize state and local governments’ borrowing for highway projects; other subsidies for state and local borrowing are provided through the tax code.

Most federal spending for highways is paid for by revenues credited to the highway account of the Highway Trust Fund, largely from excise taxes on gasoline, diesel, and other motor fuels. For more than a decade, those revenues have fallen short of federal spending on highways, prompting transfers from the Treasury’s general fund to the trust fund to make up the difference. If the taxes that are currently credited to the trust fund remained in place and if funding for highway and transit programs increased annually at the rate of inflation, the shortfalls accumulated in the Highway Trust Fund’s highway and mass transit accounts from 2021 to 2030 would total $189 billion, according to the Congressional Budget Office’s baseline budget projections as of March 6, 2020.1 Those projections, which are based on the economic forecast that CBO completed on January 7, 2020, do not account for the changes to the nation’s economic outlook and fiscal situation that have stemmed from the 2020 coronavirus pandemic.

The current authorization for federal highway programs expires on September 30, 2020. As they consider reauthorization, policymakers have many decisions to make about federal highway programs, including how to pay for those programs, how much to spend on them and how to direct that spending, and how much to subsidize borrowing by others to finance highway projects.

Revenues Credited to the Highway Trust Fund

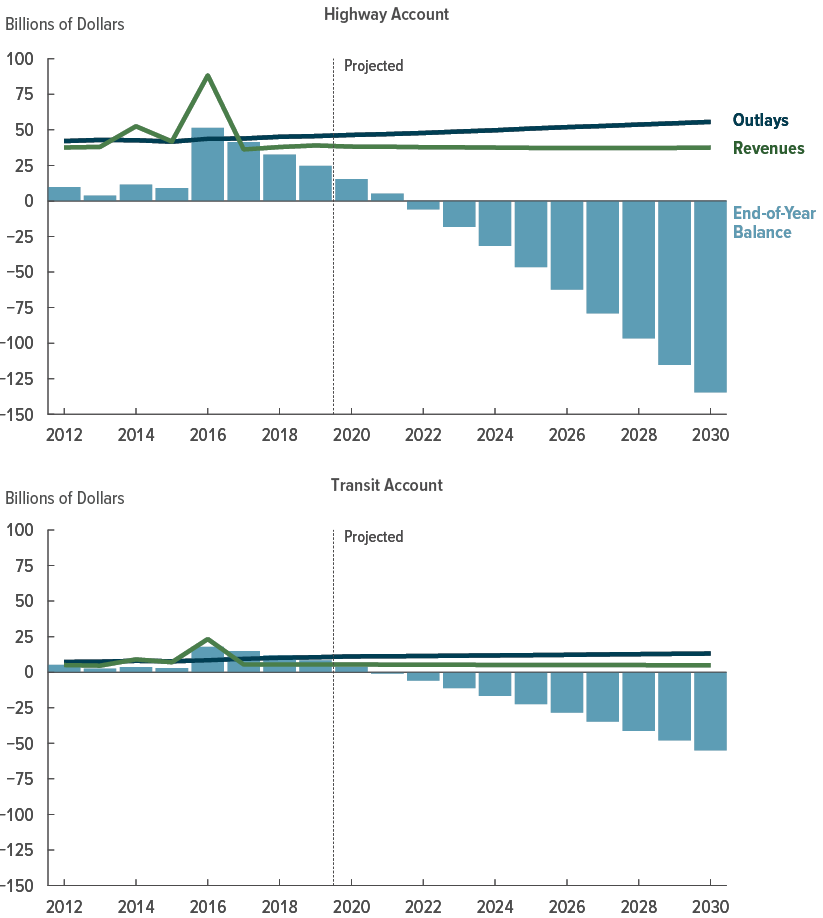

The Highway Trust Fund is an accounting mechanism in the federal budget with two accounts—one for highways and the other for mass transit—to which certain fuel and other vehicle-related excise tax collections are credited. According to CBO’s March projections, if the excise taxes are continued at their current rates and current funding for highway and transit programs increases annually at the rate of inflation, the revenues and accumulated balances of the Highway Trust Fund will be insufficient to cover spending from the transit account starting in 2021 and spending from the highway account beginning in 2022 (see Figure 1). In those projections, revenues credited to the Highway Trust Fund in 2020 total $44 billion, and outlays exceed revenues by about $14 billion.

Figure 1.

Annual Revenues, Outlays, and Balance of the Highway Trust Fund in CBO’s March 2020 Baseline Projections

Outlays from the Highway Trust Fund have long exceeded the revenues credited to it from taxes, but intragovernmental transfers have ensured that the fund’s two accounts maintained a positive balance. In CBO’s projections, the balance of the transit account is exhausted in 2021, and the highway account is in deficit the following year.

Source: Congressional Budget Office.

The projections shown here are based on CBO’s baseline budget projections as of March 6, 2020, which do not account for changes to the nation’s economic outlook and fiscal situation that have stemmed from the 2020 coronavirus pandemic. See Congressional Budget Office, Baseline Budget Projections as of March 6, 2020 (March 2020), www.cbo.gov/publication/56268.

Revenues credited to the Highway Trust Fund include tax receipts, interest, and intragovernmental transfers.

Some of the taxes that are credited to the Highway Trust Fund are scheduled to expire on September 30, 2022, including the excise taxes on tires for heavy trucks and all but 4.3 cents of the per-gallon federal tax on motor fuels (currently 24.4 cents per gallon on diesel fuel and 18.4 cents per gallon on gasoline and other fuels). However, in accordance with the rules governing baseline projections specified in the Balanced Budget and Emergency Deficit Control Act of 1985, the estimates shown here reflect the assumption that all the expiring taxes credited to the fund will continue to be collected after fiscal year 2022.

Under current law, the Highway Trust Fund cannot incur negative balances. However, to accord with the rules governing such projections, CBO’s baseline projections for surface transportation spending reflect the assumption that obligations incurred by programs funded by the Highway Trust Fund will be paid in full.

Policymakers have a number of options to increase the resources available in the Highway Trust Fund:

- Increase the existing fuel taxes. The tax on gasoline has been 18.4 cents per gallon, and the tax on diesel 24.4 cents per gallon, since October 1993. One option is to increase those taxes by 15 cents per gallon in 2021 (bringing them up to roughly the rates they would be if they had increased with inflation) and to adjust them for inflation thereafter. CBO and the staff of the Joint Committee on Taxation (JCT) estimate that such a change would raise $329 billion more in revenues for the Highway Trust Fund from 2021 to 2030 than projected in CBO’s March baseline. An increase of that amount would eliminate the fund’s shortfall and provide $140 billion for additional spending by 2030. However, that increase in fuel taxes would reduce taxable business and individual income, resulting in reductions in income and payroll tax receipts that would partially offset the increase in fuel tax receipts.

- Institute new taxes. Policymakers could institute new taxes on vehicle miles traveled (VMT), on freight shipments carried by trucks, or on electric vehicles. If, for example, a VMT tax of 5 cents per mile traveled by trucks had been in place in 2017, it would have raised about $13 billion that year—about $1 billion more than the fund’s shortfall for the year. The costs of implementing such a tax and ensuring compliance could, however, be substantial. Alternatively, a tax on freight transported by highway could also reduce the shortfall, depending on the specifics of the tax, but implementing such a tax would require establishing new mechanisms for assessing and collecting it, which could be an expensive and time-consuming process. A tax on electric vehicles would probably not have a substantial effect on the trust fund’s shortfall because the number of such vehicles remains small.

- Transfer money from the Treasury’s general fund. Under this option, the federal government would, in effect, pay for a portion of highway spending in the same way that it funds other programs and activities.

Federal Spending for Highways

The share of total economic output that federal spending for highways has accounted for has been relatively stable for several decades, though real (inflation-adjusted) federal spending has increased in recent years. Almost all of that spending, which takes place primarily through grants to state and local governments, is for capital projects rather than for operation and maintenance and is restricted to federal-aid highways, which consist of the Interstate Highway System and most other roads except for local roads. Federal highway funds are distributed to states on the basis of formulas that depend on how much states received in earlier years, so federal spending does not necessarily go to the projects that would produce the greatest net benefits.

Lawmakers have many options for determining the amount of money spent on highways, including these:

- Fund all projects for which the expected benefits meet or exceed the costs. In CBO’s estimation, that option would require increasing federal spending (which was $46 billion in 2019) to an average of at least $71 billion per year—nearly 40 percent more than projected in CBO’s baseline from 2021 to 2030. That estimate is based on analysis from the Federal Highway Administration (FHWA) and would be applicable only if state and local governments increased their spending for federal-aid highways proportionally. Implementing that option would require identifying sources of funding for the additional spending.

- Maintain the current conditions and performance of the highway system. Accomplishing that objective would require the federal government to spend at least $54 billion per year, on average, CBO estimates using FHWA data—nearly $4 billion more than the average annual spending in CBO’s 10-year baseline projections. To realize the conditions in FHWA’s model, state and local governments would also need to increase their spending for federal-aid highways.

- Set spending to match revenues. Policymakers could set spending to match the revenues projected to be credited to the highway account of the Highway Trust Fund. Under that option, nominal federal spending on highways would average $39 billion per year through 2030—an average of $12 billion (or about 25 percent) less each year than the amounts in CBO’s baseline projections.

In addition to determining how much to spend on highways, policymakers could adopt a different set of criteria for allocating that spending, such as directing federal highway funds to programs or projects on the basis of expected net benefits. Distributing funds in that manner would produce spending patterns that differed from those observed in recent years, when funds were distributed to states on the basis of formulas and states selected projects according to their own criteria and program requirements. Compared with actual spending in 2014, if spending were directed according to expected net benefits, a smaller share of spending would go to expanding non-Interstate roads in rural areas, and a larger share would go to rehabilitating non-Interstate federal-aid highways in urban areas. Furthermore, a larger share of spending than allocated in 2014 would go to rehabilitating rural and urban bridges on Interstate highways, and less would go to rehabilitating the Interstates themselves.

Federal Programs to Subsidize State and Local Borrowing for Highways

The federal government also supports investment in highways by state and local governments through several financing programs that subsidize the cost of borrowing to pay for that spending—that is, the federal government incurs costs to lower state and local governments’ borrowing costs. From 2007 to 2016, the federal government subsidized an average of $20 billion (in 2019 dollars) per year of new financing for highways that state and local governments obtained through tax-preferred bonds, direct loan and loan guarantee programs, and funds that were to be used to capitalize state infrastructure banks (SIBs). Tax-exempt bonds accounted for about three-quarters of that borrowing.

Federal policymakers could offer new programs or expand current programs to subsidize borrowing by state and local governments to build more roads. For instance, they could introduce a tax credit bond program. Depending on its design, such a program could subsidize the same amount of borrowing by state and local governments as tax-exempt bonds at a lower cost to the federal government by effectively eliminating some of the benefits of tax-exempt bonds that go to higher-income bondholders. Policymakers could also expand opportunities for state and local governments to use federally subsidized financing by authorizing state and local governments to issue more tax-exempt bonds to fund projects undertaken primarily by private entities or by extending more loans to those governments to finance transportation projects. In addition, policymakers could allow states to collect tolls on Interstate highways, which would offer states an additional revenue stream to borrow against.

A Note About the Possible Effects of the Coronavirus Pandemic on the Estimates

Several changes arising from the current public health emergency and resulting decline in economic activity will have offsetting effects on the balance of the highway account of the Highway Trust Fund. Revenues from fuel taxes will be lower than CBO projected in March because people have been driving less since the coronavirus pandemic began. If all other factors underlying CBO’s projections remained unchanged, the reduction in revenues would increase the annual shortfall in the trust fund’s highway account. But spending from the Highway Trust Fund may also decrease, because states, whose fiscal outlooks have worsened as a result of the decline in economic activity, may have to suspend highway projects for an extended period. Reductions in spending from the trust fund would, all else equal, decrease the annual shortfall. CBO has not yet assessed those changes to determine their net effect on the size of the shortfall in the Highway Trust Fund or to update the agency’s projections of when the fund’s balances will be insufficient to cover its outlays without delays.

In addition, if federal lawmakers respond to the economic downturn by providing funds for infrastructure projects outside the Highway Trust Fund, as they did in the American Recovery and Reinvestment Act of 2009, spending from the trust fund may decrease as it did in 2010.

Revenues Credited to the Highway Trust Fund

In 2019, $45 billion in revenues were credited to the Highway Trust Fund; of that amount, $39 billion went to the highway account. Most of those revenues came from taxes on gasoline and other motor fuels.

To cover the shortfalls recorded in the fund’s accounts, lawmakers have enacted legislation that since 2008 has transferred more than $140 billion—mostly from the Treasury’s general fund—to the Highway Trust Fund. Most recently, lawmakers transferred $70 billion from the general fund in 2016—$52 billion to the highway account and $18 billion to the transit account. Such intragovernmental transfers have allowed the fund to maintain a positive balance, but they have not changed the amount of receipts collected by the government.

If revenues continue to be less than spending, the Department of Transportation will have to delay its reimbursements to states for the costs of highway construction. To ensure that funding is available for highway spending at current levels or higher, lawmakers could take measures to increase the Highway Trust Fund’s resources.

Sources of Revenues

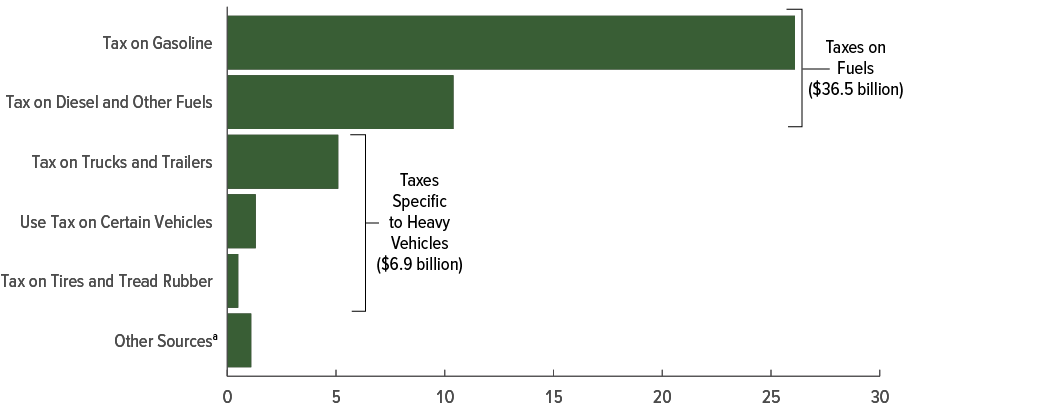

Of the revenues credited to the Highway Trust Fund in 2019, $36 billion (or 82 percent) stemmed from excise taxes on gasoline, diesel, and other motor fuels (see Figure 2). Receipts from the tax of 18.4 cents per gallon on gasoline and ethanol-blended fuel contributed the largest amount—$26 billion, or nearly 60 percent of the fund’s revenues. Receipts from the tax of 24.4 cents per gallon on diesel and other fuels totaled $10 billion, or about one-quarter of the fund’s revenues. The taxes on gasoline and diesel fuel have been in place since 1993, and the rates have not been adjusted since then. All but 4.3 cents of the per-gallon federal tax on motor fuels are scheduled to expire on September 30, 2022.2

Figure 2.

Sources of Revenues Credited to the Highway Trust Fund, 2019

Billions of Dollars

Source: Congressional Budget Office, using data from the Federal Highway Administration and the Internal Revenue Service.

a. Consists of $0.8 billion in interest income, $0.1 billion in civil penalties and fines, and $0.1 billion in other income, primarily intragovernmental transfers—that is, funds transferred from other budgetary accounts to the Highway Trust Fund.

If those taxes were extended at their current rates, revenues from gasoline and diesel taxes would decline at a rate of about 1 percent per year over the next 10 years, CBO projects. Factors contributing to that projected decline include the rising fuel economy of vehicles and the slow rate of growth of the total number of miles traveled by vehicles.3

Not all of the receipts from the excise taxes on motor fuels are dedicated to highway spending. A portion of those receipts—2.86 cents per gallon, which amounted to about $6 billion in 2019—goes to the transit account of the Highway Trust Fund. In addition, 0.1 cent per gallon goes to the Environmental Protection Agency’s Leaking Underground Storage Tank Trust Fund, which supports programs run by state and local governments that prevent and clean up leaks from underground petroleum storage tanks.

Revenues from three other taxes, which are specific to heavy vehicles, are also credited to the Highway Trust Fund. The excise tax on trucks and trailers—equal to 12 percent of the sales price of tractors, trucks, and trailers that exceed certain weights—accounted for 12 percent of the trust fund’s revenues in 2019. A tax on the use of heavy vehicles (a $100 to $550 annual tax on trucks over 55,000 pounds) and an excise tax on certain tires for heavy trucks contributed smaller amounts to the fund. (That excise tax on tires is scheduled to expire on September 30, 2022.)

In addition to those taxes, other fees and interest on invested balances totaling about $1 billion per year are credited to the trust fund.

Costs Imposed by Users

Drawing on the various taxes that are credited to the Highway Trust Fund to pay for investment in highways is consistent with the view that those who benefit from public spending should pay for it and that charging users helps allocate resources efficiently. Knowledge of how different highway users contribute to highway costs can inform lawmakers’ decisions about how to set those user charges and how to allocate the resources collected.

The most recent national study of how different types of vehicles contribute to the highway costs that federal programs pay for was published by FHWA in 2000. Passenger vehicles constituted the largest group of vehicles in use and were estimated to account for about 60 percent of federal highway costs in 2000, even though their estimated cost per mile of highway use was the lowest at 0.8 cents.

Costs attributed to trucks accounted for the remaining 40 percent of federal highway costs, but trucks provided about one-third of the Highway Trust Fund’s revenues. For each mile they traveled in 2000, combination trucks (that is, tractors pulling one or more trailers) were estimated to impose a cost of 8.4 cents. For all trucks, the estimated cost per mile traveled ranged from 2.2 cents for the trucks carrying the lightest loads to 20.3 cents for those with the heaviest loads.4

More recently, some states have calculated cost shares for different types of vehicles that are similar to the estimates in the FHWA study. Oregon estimates that in 2020, light vehicles (mainly cars and other passenger vehicles) will account for about two-thirds of state highway costs and heavy vehicles for about one-third.5 As the Oregon report notes, however, highway spending by state governments includes maintenance costs, whereas federal spending does not. Maintenance costs, such as snow removal and pothole patching, relate primarily to light vehicle use, so a comparable study of federal expenditures would be expected to attribute a larger share of costs to heavy vehicles.

Options

Lawmakers have several options for increasing resources in the Highway Trust Fund. One option is to increase existing taxes on gasoline and diesel fuels. Alternatively, lawmakers could impose new taxes on vehicle miles traveled, on freight movement, or on electric vehicles. Finally, the Congress could make additional transfers from the Treasury’s general fund to the Highway Trust Fund.

Increase Existing Fuel Taxes. CBO analyzed an option that would increase federal excise tax rates on gasoline and diesel fuel by 15 cents per gallon and adjust them to grow with inflation thereafter. If those rates (which have not changed since 1993) had grown with inflation as measured by the gross domestic product (GDP) price index, the 18.4 cent-per-gallon gasoline tax would have increased by about 12 cents by 2019, and the 24.4 cent-per-gallon diesel tax would have increased by about 15 cents.

According to JCT’s estimates, increasing the tax rates on fuel by 15 cents in 2021 and indexing them to the consumer price index thereafter would increase cumulative fuel-tax receipts credited to the Highway Trust Fund over the 2021–2030 period above the amount in CBO’s March baseline projections by $329 billion. An increase of that amount would eliminate the current shortfall and provide an additional $140 billion in revenues to the Highway Trust Fund by 2030. Interest payments on any accumulated balances would further increase the resources available in the trust fund. However, that increase in fuel taxes would reduce other federal income and payroll tax receipts by decreasing taxable business and individual income.6

Institute New Taxes. Another option is to impose new taxes that better align the taxes paid for using roads with the cost of building those roads. In recent years, revenues credited to the Highway Trust Fund have declined. Because of improvements in fuel efficiency, drivers use less fuel and therefore pay less in fuel taxes to travel the same distance. Meanwhile, under current law, drivers of the small but growing number of all-electric vehicles do not pay any of the federal taxes that are credited to the Highway Trust Fund—though a tax on electric vehicles would probably not have a substantial effect on the trust fund’s shortfall because the number of such vehicles remains small (see Box 1).

Box 1.

Electric Vehicle Fees and Incentives

More than 1.5 million plug-in electric cars and light trucks were on the road in 2019—a number that represents 0.6 percent of the stock of light-duty vehicles.1 Because drivers of electric vehicles (EVs, including plug-in hybrid vehicles, which combine a gasoline engine with a battery-powered electric motor that can be recharged by plugging it into an external electricity source, as well as all-electric vehicles, which run solely on battery power) pay little or no state fuel tax, many states have begun charging owners of EVs an annual fee, typically in the range of $50 to $200. If in 2019 the federal government had charged an annual EV fee of $100—comparable to the average amount that drivers of light-duty vehicles would have paid in federal fuel taxes in 2017—it would have raised about $150 million, the Congressional Budget Office estimates, using data from the U.S. Energy Information Administration.2 By comparison, in 2019, the Highway Trust Fund’s outlays exceeded revenues by $11.6 billion.

Plug-in EVs represent a small but growing segment of the light vehicle market. In 2018, 362,000 plug-in EVs were sold, accounting for 2 percent of the nearly 17 million light vehicles sold that year. That volume of sales represented an 85 percent increase over the previous year and was more than six times the number of EVs sold in 2012.3

To reduce the reliance on petroleum in the transportation system, lawmakers at both the federal and state levels have implemented a variety of tax credits and subsidies that incentivize people and businesses to purchase plug-in EVs. Those subsidies further that goal, but they also tend to boost the number of miles traveled by vehicles paying little or no fuel tax. At the federal level, the full value of the tax credit for the purchase of a plug-in EV by a consumer or business ranges from $2,500 to $7,500, depending on the vehicle’s battery capacity.4

In 2017, $573 million in plug-in EV tax credits were claimed by about 91,000 taxpayers, the Internal Revenue Service reports. A disproportionate number of those credits were claimed by higher-income households: 75 percent of returns claiming the tax credit showed an adjusted gross income of $100,000 or more, whereas only 18 percent of all returns reported income of that amount.5 The extent to which the benefits of such tax credits flow to purchasers or to the manufacturers of EVs is unclear. Between 2019 and 2023, the staff of the Joint Committee on Taxation estimates, claims for the plug-in EV tax credit will total $4.8 billion.6

State and local governments also provide a variety of financial incentives to encourage people and businesses to buy plug-in EVs. Examples of such incentives include rebates on purchases of EVs, tax credits for purchasing or converting vehicles to electric power, exemptions from excise taxes, reductions in toll fees, and reductions in vehicle registration fees. As with the federal tax credits, those benefits are largely claimed by people with relatively high income. Some states also offer EV owners additional benefits, such as access to high-occupancy vehicle lanes, exemptions from emissions testing, and financial incentives to install charging infrastructure.

1. U.S. Energy Information Administration, Annual Energy Outlook 2020 (January 2020), Table 39, www.eia.gov/outlooks/aeo/.

2. U.S. Energy Information Administration, Monthly Energy Review (September 2019), Table 1.8, www.eia.gov/totalenergy/data/monthly/previous.php.

3. Stacy C. Davis and Robert G. Boundy, Transportation Energy Data Book: Edition 38.1 (prepared by Oak Ridge National Laboratory for the Department of Energy, April 2020), Table 6.2, https://tedb.ornl.gov/.

4. The plug-in electric vehicle credit was established by the Energy Improvement and Extension Act of 2008 (Public Law 110-343) and codified in 26 U.S.C. §30D. The credit begins to phase out once a manufacturer has sold 200,000 qualifying vehicles. General Motors and Tesla have exceeded that threshold. See Congressional Budget Office, Effects of Federal Tax Credits for the Purchase of Electric Vehicles (September 2012), www.cbo.gov/publication/43576.

5. Internal Revenue Service, “All Returns: Tax Liability, Tax Credits, and Tax Payments, by Size of Adjusted Gross Income, Tax Year 2017” (September 2019), Table 3.3, https://go.usa.gov/xv38b.

6. Joint Committee on Taxation, Estimates of Federal Tax Expenditures for Fiscal Years 2019–2023, JCX-55-19 (December 18, 2019), https://go.usa.gov/xv3Uy.

Impose a VMT Tax. Instituting a tax on vehicle miles traveled would charge all vehicles for their highway use regardless of the vehicle’s fuel efficiency or energy source, but doing so would present several challenges. A VMT tax would be more costly to administer than the current excise taxes on fuels. In addition, such a tax would raise privacy concerns if calculating and collecting the tax required the government to track people’s movement and use of vehicles. Apart from those challenges, a VMT tax has implications for equity that are similar to those of fuel taxes—namely, the burden, relative to income, is greatest for lower-income households because the money paid in taxes for highway use would constitute a larger share of their total income than of higher-income households’ total income.

Limiting a VMT tax to only commercial trucks would raise fewer of those concerns. Because many trucking companies already track their vehicles, implementing a VMT tax on only commercial trucks would require overcoming fewer administrative and privacy hurdles than implementing such a tax on all vehicles would.

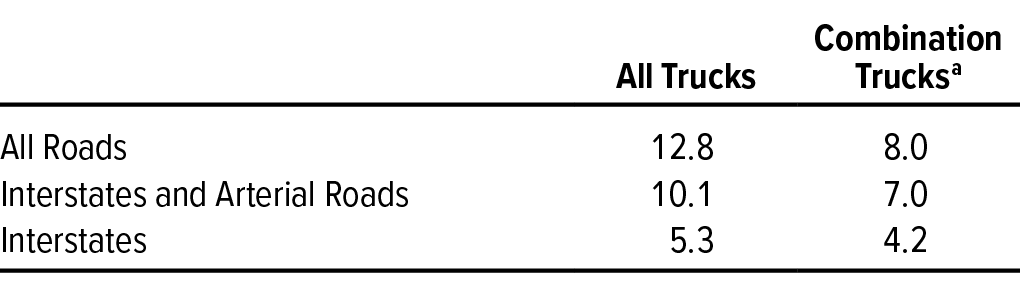

CBO recently analyzed the effects on revenues of several possible formulations of a VMT tax on commercial vehicles.7 One example suggested that if a 5 cent tax per mile traveled by trucks had been in place in 2017, it would have generated between $4 billion and $13 billion in revenues that year, depending on the types of trucks and roads that the tax applied to. Taxing all trucks, including box and large pickup trucks, would raise more revenues than taxing only combination trucks. Similarly, revenues would be greater if the tax applied to travel on all public roads than they would be if it applied only to travel on Interstates or on Interstates and arterial roads (see Table 1).

Imposing a federal VMT tax on commercial trucks could eventually be a substantial source of revenues for the Highway Trust Fund, but doing so would require lawmakers to make several choices about the design of the tax:

- Which trucks would be taxed on which roads?

- What would the structure of the tax rates be?

- How would the tax be implemented?

Establishing and operating a program to collect a VMT tax on commercial trucks would entail not only costs to set up the program, including capital costs for new equipment, but also ongoing administrative and enforcement costs. The costs of instituting such a program would be incurred before any revenues were generated by the program.

Establish a Highway Freight Tax. An alternative option for raising highway revenues is to institute a new tax on freight traveling by highway that is similar to the taxes currently collected on freight transported by plane or by ship. Taxes on freight transportation could raise a substantial amount of money relative to the shortfall in the Highway Trust Fund, but the amount of revenues generated would depend on what was taxed and the rate that was set. Implementing a highway freight tax would require policymakers to make decisions about which freight shipments would be taxed and to design and implement a system to collect those taxes. Those choices would determine the capital costs of setting up the system as well as the ongoing costs to administer it and enforce collections.

The taxes on freight transported by plane and by ship provide two different models of how a tax on freight transported by trucks might work. The waybill tax on domestic cargo transported by air is one of several sources of revenues credited to the Airport and Airway Trust Fund—the primary funding source for the Federal Aviation Administration and for federal grants to airports. The tax is equal to 6.25 percent of the amount paid for transport. If policymakers used that tax as a model for designing a freight tax on cargo transported by truck, they would need to decide which shipments to include and which shipping fees to tax. A trucking industry association reported that total revenues for the industry were about $800 billion in calendar year 2018, though that includes only primary shipments (that is, the first movement of freight from an origin to a destination), not secondary shipments by truck.8

Cargo transported by ship is taxed in a different manner. The freight tax on ship cargo, which through the Harbor Maintenance Trust Fund provides half of the funds for federal spending on harbor maintenance, is equal to 0.125 percent of the value of domestic and imported cargo moving through ports on the coasts and Great Lakes. (Exports are not subject to the tax because the Constitution forbids the taxation of exports.) Policymakers seeking to implement a similar tax on freight shipped by trucks over the nation’s highways would face decisions about which cargo would be subject to such a tax and about how to value those shipments. In 2017, the value of shipments sent by truck in the United States—including intermediate and finished goods and imported and exported goods—totaled nearly $10.5 trillion.9

Transfer General Revenues. Since 2008, lawmakers have transferred more than $140 billion from general revenues to the Highway Trust Fund. Most recently, in 2015, the Fixing America’s Surface Transportation (FAST) Act authorized a transfer of $70 billion to the fund. Further transfers would supplement the revenues collected from the excise taxes dedicated to highway and transit programs. In CBO’s 10-year baseline projections, outlays from the transit account exceed accumulated balances and annual revenues in 2021, and the highway account is exhausted the next year. In the highway account, the cumulative shortfall over the 2022–2030 period is projected to be $135 billion; the cumulative shortfall in the transit account over the 2021–2030 period is projected to be $55 billion.

Using general revenues to fund federal highway spending on an ongoing basis would have the effect of decoupling spending from the user charges that pay for that spending, but that approach has two advantages. First, if taxes were increased to pay for highway programs, the incremental costs of collection would be negligible because income taxes and other broad-based taxes are already in place. In addition, compared with several of the other options for increasing the amounts credited to the Highway Trust Fund, funding highways through broad-based taxes would have the advantage of not imposing a larger burden, relative to income, on lower-income households.

Funding highway programs with general revenues instead of taxes on highway users would also have some disadvantages. If spending on other programs was reduced to pay for highway programs, the benefits of highway investments would be at least partially offset by a reduction in the benefits that would have been provided by that other spending. If, instead, lawmakers chose to pay for highway programs by taking on additional debt, such a policy would tend to slow the economy in the long term by reducing the amount of money available for private investment.10 Finally, if highway spending was less connected to highway-use taxes, users would have a reduced incentive to drive less or to conserve fuel, and any gains in fairness and efficiency from a system in which users pay for the benefits they receive would be reduced or eliminated.

Federal Spending for Highways

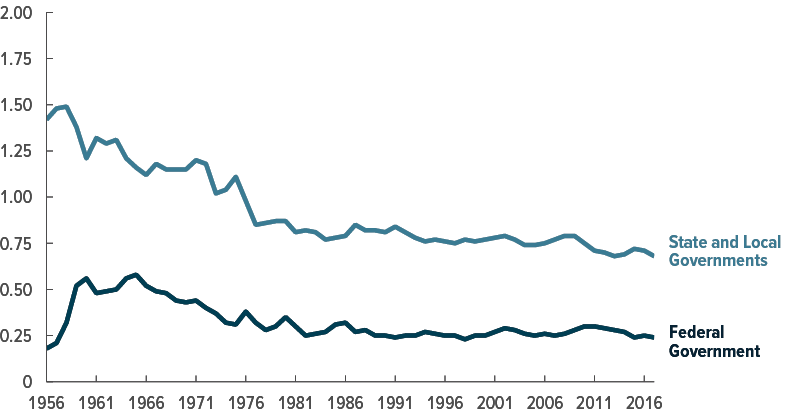

In 2017, the most recent year for which data about highway spending by all levels of government are available, the federal government spent $46 billion on highways—an amount equal to 0.24 percent of GDP. Such spending’s share of total economic output has, in general, been stable over the past 30 years, though it is only half as large as it was in the 1960s, when construction of the Interstate highway system expanded (see Figure 3).

Figure 3.

Public Spending for Highways as a Share of GDP

Percentage of GDP

State and local governments spend nearly three times as much as the federal government on highways. Measured as a percentage of total economic output, such spending by those levels of government has been relatively stable for the past 30 years.

Source: Congressional Budget Office, using data from the Bureau of Economic Analysis, the Census Bureau, and the Office of Management and Budget.

GDP = gross domestic product.

State and local governments spent nearly three times as much as the federal government on highways in 2017—$131 billion, or about two-thirds of one percent of GDP. Like federal spending on highways, state and local governments’ spending as a share of GDP peaked in the 1950s and 1960s, when it accounted for about twice the share it has in recent years.

Between 2009 and 2011, during and immediately after the 2007–2009 recession, federal spending for highways increased as a share of GDP, while state and local governments’ highway spending from their own funds fell. That shift was due, at least in part, to the additional federal funds provided to states for highway capital projects in the American Recovery and Reinvestment Act of 2009 (see Box 2). As the economy recovered, federal spending on highways relative to the nation’s total output gradually returned to prerecession levels. Though state and local governments’ nominal spending for highways has increased, it still accounts for a smaller share of GDP than it did before the recession.

Box 2.

Federal Highway Spending and the American Recovery and Reinvestment Act

Lawmakers are considering options to increase spending for infrastructure as one possible response to the economic downturn caused by the 2020 coronavirus pandemic. Depending on how such spending was structured, it could have implications for the Highway Trust Fund in addition to any effects it had on the economy as a whole. Specifically, if the matching requirements or other conditions on the use of such funds are less stringent than those for the ongoing trust fund programs, some of the new funding may initially be used in place of existing funding, rather than in addition to it.

One example of such stimulus spending is the American Recovery and Reinvestment Act of 2009 (ARRA; Public Law 111-5), which lawmakers enacted in response to the recession that began in 2007. Among other things, ARRA provided $27.5 billion from the general fund of the Treasury in grants for highway projects that were awarded to states on the basis of formulas.

The increased funding from ARRA temporarily decreased spending from the Highway Trust Fund because the stimulus spending replaced some spending from the trust fund. Projects that were eligible for funding from the Highway Trust Fund were also eligible for the funding provided under ARRA, but the ARRA funds had to be committed to a project within one year and did not require states to provide a matching contribution. In 2010, outlays for highways from ARRA funds totaled $12 billion, while outlays from the highway account of the Highway Trust Fund were $32 billion, $6 billion less than they were the previous year. Revenues credited to the highway account of the Highway Trust Fund equaled 94 percent of expenditures in 2010; in more recent years, the ratio of revenues to spending has been closer to 80 percent.

Nominal federal spending for highways has largely kept pace with the growth of the economy in recent decades, but the amount of construction put in place has not always followed the same path. Using infrastructure-specific price indexes to calculate real spending on highways indicates that such spending fell by 4 percent from 1998 to 2017. Starting in 2003, construction costs, particularly the costs of building materials, increased more quickly than general inflation.11

Using the GDP price index to remove the effects of inflation presents a much different picture of federal highway spending. Based on that inflation measure, real federal spending on highways increased by 55 percent from 1998 to 2017. That trend indicates that the amount of federal resources that the government devoted to highways increased in those years—though that increase did not keep pace with construction costs.

For the past several years, the difference between inflation in prices overall and inflation in construction costs has narrowed, so real spending based on the two inflation measures is similar.

Characteristics of Federal Funding for Highways

Two characteristics of the ways that the federal government typically spends on highways stand out. First, most federal highway funding takes the form of grants to state and local governments, which own most public roads in the United States and have broad discretion, with some constraints, to spend those federal funds. Second, federal spending on highways is almost entirely dedicated to capital projects that are intended to expand or rehabilitate eligible federal-aid highways.

Grants to State and Local Governments. In 2017, most of the $46 billion that the federal government spent on highways took the form of grants to state and local governments. State and local governments own almost all highways; federal agencies own less than 1 percent of public roads (typically, those in national parks and forests, on Indian reservations, or on other federally owned land).

In general, state and local governments decide which projects to undertake and, as construction proceeds, receive reimbursements from the federal government for projects that meet federal eligibility criteria for various programs. Most federal highway programs set a cap on the portion of a project’s total costs that a federal grant may cover—typically 80 percent. State and local governments must cover the remaining costs with nonfederal funds, such as tax revenues or proceeds from issuing municipal bonds.

States’ departments of transportation are ultimately responsible for planning and coordinating federal highway and transit investments, and each year they prepare both long-range (20-year) and short-range (4-year) plans outlining how they intend to use funds. In urban areas, metropolitan planning organizations—comprising representatives from local governments and transportation agencies—coordinate with the states’ departments of transportation to develop the plans.12

Not all roads are eligible for federally funded projects. FHWA classifies roads according to their function in terms of providing access and mobility, and those classifications serve as a basis for directing federal funds. Roads that primarily provide access usually serve smaller volumes of traffic traveling for shorter distances at lower speeds, whereas roads that provide mobility typically serve larger volumes for longer distances at higher speeds and often have a limited number of access points to maintain the speed of travel.13

FHWA identifies four categories of roads, which overlap to some extent:

- Highways in the Interstate System;

- Roads in the National Highway System—Interstates and other roads serving significant population centers, border crossings, transportation facilities, or travel destinations;

- Federal-aid highways—roads in the National Highway System and most other roads that are not local; and

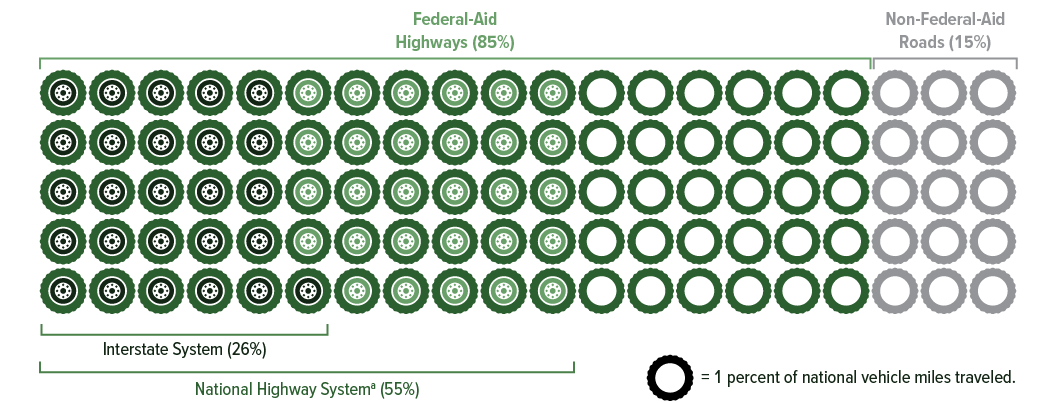

- Non-federal-aid roads—mostly local roads (two-lane roads that are usually owned by local governments and function almost entirely to provide access) and certain others that are not typically eligible for federal aid (see Figure 4).

Figure 4.

Shares of National Vehicle Miles Traveled on Different Types of Roads, 2018

Source: Congressional Budget Office.

Federal-aid highways are eligible for federal funding, and non-federal-aid roads (mostly local roads) are not.

a. The National Highway System comprises Interstates and other roads serving significant population centers, border crossings, transportation facilities, or travel destinations.

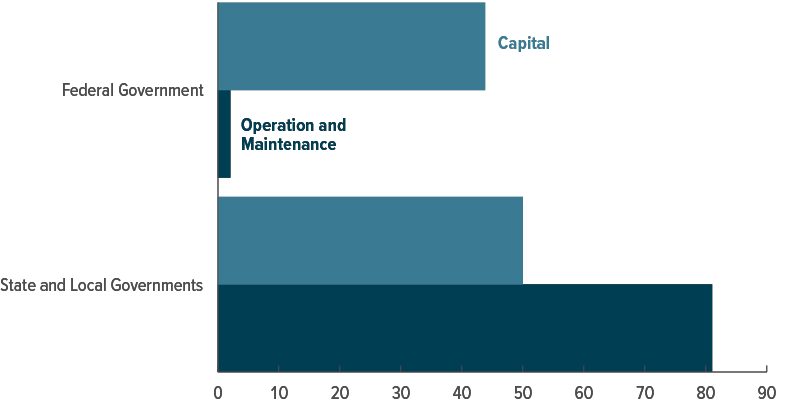

Capital Spending. Federal highway programs are dedicated almost entirely to capital projects rather than to the operation and maintenance of roads. In 2017, $44 billion (or 96 percent) of federal spending for highways went to capital investment (see Figure 5). Such an allocation between capital and operation and maintenance has been typical of federal spending for highways since the 1950s. Because the federal government does not generally own highways, the responsibility to operate and maintain them falls to state and local governments. Spending patterns reflect that: Operation and maintenance accounted for more than 60 percent of state and local governments’ spending on highways, net of federal grants, in 2017.

Figure 5.

Spending for Highways, by Level of Government and Type of Spending, 2017

Billions of 2017 Dollars

Federal spending for highways consists primarily of grants to state and local governments to help pay for capital projects. Those governments own the roads and pay to operate and maintain them.

Source: Congressional Budget Office.

Federal funds are generally eligible to be spent only on capital projects. That spending includes outlays for the purchase of structures (such as new highways and bridges) and equipment as well as expenditures that improve or rehabilitate structures and equipment already in place. Operation and maintenance costs include the costs of providing necessary operating services (such as snow removal) and maintaining and repairing existing capital (such as filling potholes) as well as the costs of funding other highway-related programs (such as education on highway safety).

Distribution of Federal Funds to States

Under the most recent authorization for highway spending—the FAST Act, which became law in 2015—more than 90 percent of federal highway assistance each year was designated for apportionment to states based on formulas. Formulas have long been used to distribute funds to states under various federal highway programs.14 In the past, those formulas have accounted for a number of different factors, including the state’s population, share of national highway lane miles, share of vehicle miles traveled, land area, rates of diesel fuel use, and tax payments to the Highway Trust Fund. Some formulas have also included program-specific factors, such as air quality measures (for air congestion and air pollution programs) and fatalities (for safety programs).

Starting in the 1980s, surface transportation authorization acts also included provisions that guaranteed that the amount of federal highway funding apportioned to each state would, at a minimum, equal a certain percentage of the federal highway taxes collected in that state. Most states received additional funds even if their apportionment would have been sufficient to meet the guarantee without them. Such provisions made the formula factors less important in determining a state’s share of funding.15

The two most recent federal highway authorization acts further departed from the factors included in earlier apportionment formulas. Enacted in 2012, the Moving Ahead for Progress in the 21st Century Act, or MAP-21, based each state’s apportionment primarily on its share of total federal highway funding in 2012. Today, under the FAST Act, formula funds are apportioned among the states largely on the basis of each state’s share of the apportioned funding in 2015, but if necessary, the apportioned amount is adjusted to ensure that each state receives at least 95 percent of the tax payments that it remits to the highway account of the Highway Trust Fund.

Once a state’s total apportionment has been set, that amount is divided (on the basis of the amounts and formulas set out in the FAST Act) among six different federal programs—the National Highway Performance Program, the Surface Transportation Block Grant Program, the Highway Safety Improvement Program, the Congestion Mitigation and Air Quality Improvement program, the Metropolitan Planning Program, and the National Highway Freight Program. For many of those programs, after that initial apportionment, states have the flexibility to transfer up to half the funds apportioned to one program to the other programs.

Programs whose funding is not apportioned to states on the basis of a formula account for less than 10 percent of federal highway spending authorized by the FAST Act. A number of those programs nevertheless support highway spending by state and local governments. Some, such as the Nationally Significant Freight and Highway Projects program, provide grants to state and local governments, and others, such as the Transportation Infrastructure Finance and Innovation Act credit program, make loans to those governments to help finance transportation projects. In addition, a small share of federal highway spending pays for highway projects on federal lands.

Options

In legislation to authorize federal highway programs, the Congress specifies both the total amount of funding and the manner in which those funds are to be allocated among states and programs. A number of different criteria could be used to set total annual amounts of federal highway funding: Lawmakers could, for example, choose to target specific levels of highway conditions or to tie spending levels to revenue collections. Apportionment of those funds could rely on formulas based on highway or economic measures, or the Congress could shift away from using formulas in that process toward allowing federal policymakers to play a larger role in selecting specific projects.

Options for Determining Total Annual Spending Amounts. To construct its baseline projections for spending on highways from the Highway Trust Fund, CBO starts with the funding provided in the most recent appropriation law and adjusts that amount to grow at the projected rate of inflation (which is based on a combination of the projected changes in the GDP price index and in the employment cost index). However, lawmakers could choose to set annual spending levels for highway programs according to a number of different criteria. CBO analyzed three options that the Congress could pursue.

Fund All Highway Projects for Which Benefits Exceed Costs. Funding all projects for which benefits are expected to equal or exceed costs would require increasing annual spending well above recent amounts and the amounts in CBO’s baseline projections. On the basis of analysis from FHWA that examined the 2015–2034 period, CBO estimates that the federal portion of the total average annual investment from 2021 to 2030 that would be required to implement all highway and bridge projects on federal-aid highways for which benefits are expected to meet or exceed costs is $71 billion.16 That amount would represent an increase of more than 50 percent over the $46 billion in outlays that the federal government made for highways from the Highway Trust Fund in 2019. State and local governments would also have to increase spending on federal-aid highways to achieve the total level of investment modeled in the FHWA analysis. If those funds were spent only on projects whose benefits were estimated by FHWA to meet or exceed costs, that spending would improve pavement quality and expand the highway system’s capacity. As a result, the share of total vehicle miles traveled on federal-aid highways whose pavement was rated good or fair (as opposed to poor) would increase from 83 percent to 89 percent, and annual average travel delays per vehicle would be cut by about 9 hours.

Spending estimates that arise from benefit-cost analysis are uncertain, however. They rely on judgments about a variety of factors, including the value of costs and benefits that are difficult to measure (such as the value of travelers’ time), the appropriate interest rate to use to discount future costs and benefits to present values, and how highways will be used in the future (for example, the number of vehicle miles traveled by passenger vehicles and trucks).

Set Spending to Maintain Current Highway Conditions and Performance. The Congress could choose to spend less than would be required to fund all highway projects with an estimated net benefit. Using FHWA’s analysis, CBO estimates that an annual average of $97 billion in total federal and state spending would be needed over the 2021–2030 period to maintain highway conditions and performance on federal-aid highways—namely, pavement quality, bridge conditions, and travel delays—at their 2014 levels.17 If the federal government’s share of spending for capital on federal-aid highways remained 56 percent (the average share from 2004 to 2014), average annual federal spending from 2021 to 2030 would be $54 billion, about 18 percent more than spending in 2019.

Limit Spending to the Amount of Revenues Credited to the Highway Account of the Highway Trust Fund. Instead of targeting certain highway performance levels, this option would reduce the funding provided for highway programs so that it equaled the amount of revenues projected to be credited to the highway account of the Highway Trust Fund. Annual outlays under the option would average $39 billion from 2021 to 2030. The federal taxes that directly fund the Highway Trust Fund would not change. (The option would not affect highway spending that is provided under other funding authority—namely, spending for the Emergency Relief Program and a small portion of the National Highway Performance Program, which totals $739 million per year in CBO’s baseline projections.)

Under this option, the total amount of funding provided through highway grants to state and local governments over the 2021–2030 period would be $156 billion less than it is in CBO’s baseline projections. If federal appropriations were set accordingly, outlays over that period would be $124 billion less than the amounts projected in the baseline. Those two sums differ because some of the money is not spent immediately when funds are committed to a project; rather, such outlays typically span several years after the funds are obligated. About one-quarter of the savings in outlays associated with a reduction in obligations in a given year are projected to occur in the same year, and about 40 percent occur the following year. Thus, the option would not entirely eliminate the trust fund’s shortfall over the 2021–2030 period, because spending during the first several years of that period would be affected by the greater funding provided in earlier years.

Options for Distributing Federal Highway Spending. For any given amount of spending for highways, the federal government can decide to spend or distribute those funds in different ways. Under the current system, in which federal funds are apportioned to states largely according to how those funds were distributed five or eight years earlier, federal highway spending is not necessarily distributed in a way that reflects the use or condition of the highway system. Nor does such spending necessarily fund the highway projects that are expected to generate the largest net benefits.

If more federal funds for highways were distributed to programs or projects whose benefits were expected to outweigh their costs, policymakers could boost the impact of highway spending on the economy. FHWA examined how spending on federal-aid highways in 2014 was distributed in both rural and urban areas among projects that either expanded the highway system or rehabilitated highways or bridges.18 The shares devoted to those two types of areas and types of projects were different from the shares that would be provided under the scenario modeled by FHWA in which all highway projects whose benefits equaled or exceeded their costs would be funded. In particular, a smaller share of spending would go to expanding the federal-aid highway system in rural areas under that scenario than actually went to such projects in 2014; in urban areas, a smaller share would be spent on rehabilitating Interstates, and a larger share would go to rehabilitating other federal-aid highways. In both rural and urban areas, a larger share of funding would go to rehabilitating bridges on Interstates (see Figure 6).

Figure 6.

Shares of Total Federal-Aid Highway Spending Used for Various Purposes

Percent

Source: Congressional Budget Office, using data from the Federal Highway Administration.

The shares suggested by FHWA’s scenario in which highway conditions and performance would be improved are based on investment over the 2015–2034 period. Under that scenario, the share of spending going to system enhancements (safety enhancements, traffic control facilities, and environmental enhancements) would remain constant at the 2014 level, so that spending is excluded from this figure. For details on that scenario, see Federal Highway Administration and Federal Transit Administration, Status of the Nation’s Highways, Bridges, and Transit: Conditions and Performance, 23rd ed. (November 2019), www.fhwa.dot.gov/policy/23cpr/.

FHWA = Federal Highway Administration.

Another option lawmakers could choose is to provide more funding to programs that use benefit-cost analysis in selecting projects, such as the Better Utilizing Investments to Leverage Development (BUILD) program.19 Funding projects with the highest net economic benefits could realize most of the benefits of current highway spending at a lower cost or allow the same amount of spending to have a greater economic payoff.20 Another approach is to promote the use of benefit-cost analysis at the state and local levels, where most of the spending decisions are made.

Benefit-cost analyses have some limitations, however. Lawmakers may want to fund highway projects to achieve various other objectives that are not accounted for in such analyses—increasing employment or increasing rural access to transportation networks, for example. In addition, programs that assess the benefits and costs of highway spending will improve the economy’s performance only to the extent that the calculations adequately capture the benefits to the economy, and benefit-cost analysis on a project-by-project basis may miss important ways in which distinct components of the highway network affect one another. Also, implementing policies that emphasized such analysis would reduce state and local governments’ discretion in how they use their federal funds.

Federal Programs to Subsidize State and Local Borrowing for Highway Spending

In addition to providing grants to state and local governments to pay for highway capital projects, the federal government also supports state and local investment in highways through a variety of mechanisms that reduce the cost of their borrowing. In some cases, that federal support comes through forgone federal tax revenues. Other mechanisms appear as spending in the federal budget. The federal cost of each dollar of financing provided to state and local governments varies for the different mechanisms.

To finance investments in highways, state and local governments borrow from the federal government or issue bonds to obtain funds that they repay over time. Financing allows state and local governments to pay for highways and other infrastructure over a period that more closely matches the useful life of that infrastructure. Financing can be particularly attractive when a government does not have the resources on hand that are required to fund a desired investment. However, financing is not a source of revenues; it is a means of making future state and local revenues available to pay for projects sooner. Future revenues committed to paying back funds that are borrowed today will not be available to pay for projects in the future.

Of the available federally supported financing mechanisms, tax-preferred bonds are the one that states and localities have used most frequently to finance highway infrastructure. Most of those tax-preferred bonds are tax-exempt bonds, but tax credit bonds, which are no longer authorized to be sold, have been used in the past and still affect the federal budget. Another financing mechanism, direct federal credit programs, offers loans or loan guarantees to state and local governments for highway projects. Finally, states can establish infrastructure banks to finance highway projects, but the use of that financing mechanism for such purposes is not widespread.

From 2007 to 2016, CBO estimates, an average of $20 billion (in 2019 dollars) each year, or about one-fifth of the public sector’s total capital spending on highways, involved federally supported financing.21 That federally supported financing accounted for 37 percent of the $54 billion (in 2019 dollars) that state and local governments spent, on average, each year for highway capital projects from funds other than federal grants over that period.

Tax-Preferred Bonds

State and local governments frequently issue bonds, which they sell to investors, to raise money to pay for capital investments in highways and other infrastructure. Tax-exempt bonds are the most frequently used federally supported financing mechanism. The interest paid on such bonds is generally exempt from federal income tax, so issuers can pay a lower interest rate than private bonds would pay and still attract investors. But to attract enough investors, issuers must pay a higher interest rate than they would need to pay to attract some investors. Some of the federal subsidy goes to those investors who would have purchased the bonds at a lower interest rate and thus does not provide a benefit to the issuer.

Although the federal government does not currently authorize state and local governments to issue tax credit bonds, when such bonds were issued in the past, the federal subsidy was paid either as an annual credit against bondholders’ federal income tax liability (instead of, or sometimes in addition to, the interest that typically would be paid) or as a direct payment to the bonds’ issuer that was equal to a portion of the interest paid to the bondholder. All of the benefit of the federal subsidy for tax credit bonds could, therefore, go to the state or local government issuing the bond.

Federal subsidies for tax-preferred bonds are paid through reductions in taxes or spending from the general fund, so neither tax-exempt bonds nor tax credit bonds affect outlays from the Highway Trust Fund.

Tax-Exempt Bonds. From 2007 to 2016, state and local governments issued an average of $15 billion (in 2019 dollars) of new tax-exempt bonds for highway projects per year (see Table 2). Such bonds accounted for about three-quarters of the new federally supported highway financing in those years.22 State and local governments rely on several different sources of funds to repay that borrowing, including general revenues and fuel and vehicle-related taxes. In addition, some highway projects may generate revenues to repay bondholders from tolls. State and local governments may also issue grant anticipation revenue vehicle (GARVEE) bonds, which are backed by expected future federal grants. All of those financing options provide state and local governments substantial latitude in choosing which public-purpose projects to finance with bond proceeds.

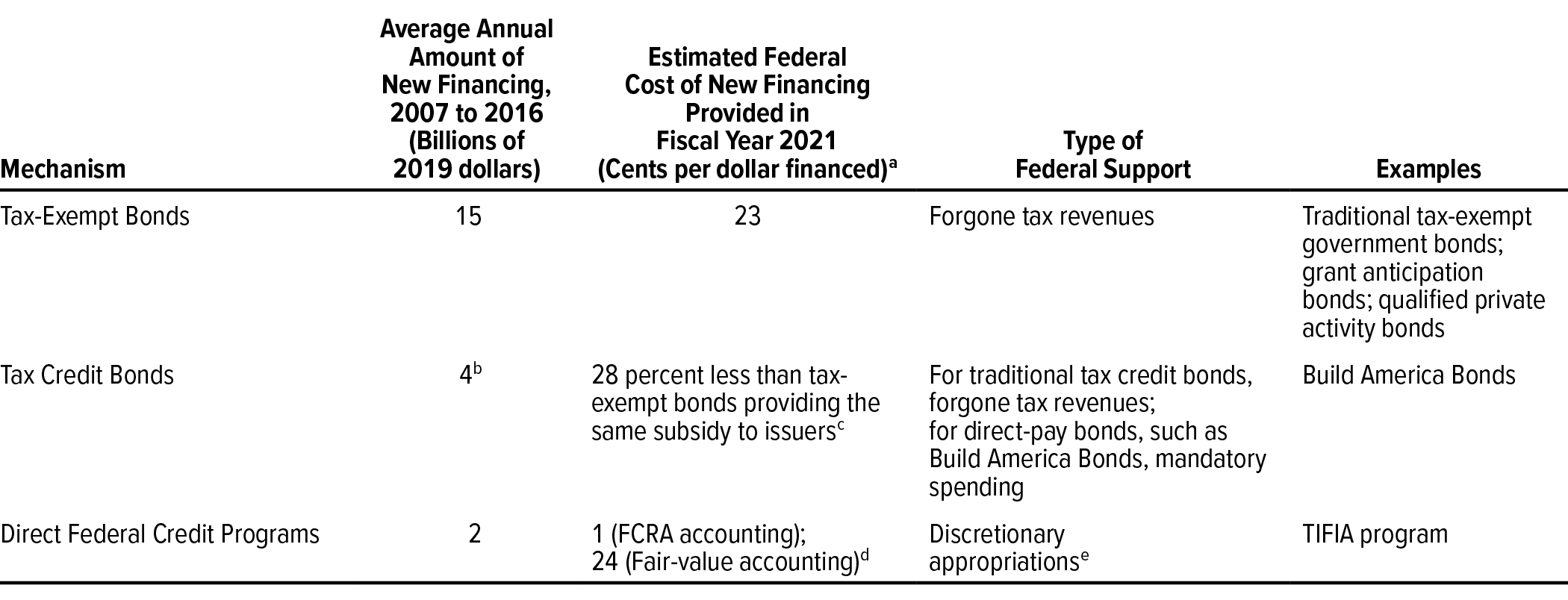

Table 2.

Selected Federally Supported Mechanisms That State and Local Governments Use to Finance Highway Infrastructure

Source: Congressional Budget Office.

FCRA = Federal Credit Reform Act of 1990; TIFIA = Transportation Infrastructure Finance and Innovation Act.

a. The estimate for tax-exempt bonds is based on 20-year financing; the estimate for direct federal credit programs is for loans from the TIFIA program, which commonly have terms of 30 to 35 years. All estimates are discounted present values—that is, they express related current and future cash flows as an equivalent lump sum paid when the financing is provided.

b. The average reflects the Build America Bonds that were issued for highway projects in 2009 and 2010, the only two years in which those bonds were authorized to be sold.

c. No current program allows such bonds to be issued for transportation infrastructure.

d. These estimates are for direct loans from the TIFIA program. The FCRA estimate is from the Office of Management and Budget. CBO’s fair-value estimate reflects the market value of the financial risk associated with the program.

e. The largest direct federal credit program for transportation, the TIFIA program, is formally funded by contract authority, which is a form of mandatory budget authority. However, use of that contract authority is controlled by limitations on obligations contained in annual appropriation acts.

Another type of tax-exempt bond, qualified private activity bonds (QPABs), may be used to finance projects that are undertaken mainly by private entities. The state or local government issues such bonds on the private entity’s behalf after receiving approval from the federal Department of Transportation. The total amount authorized to be issued as highway QPABs nationwide is currently capped at $15 billion.

For every dollar of tax-exempt bonds with a 20-year repayment period issued in 2021, federal tax revenues would be reduced by 23 cents, CBO estimates, because the interest paid on those bonds would be exempt from federal taxes. If the average annual amount of new bond financing from 2021 to 2025 was the same as it was from 2007 to 2016, the federal revenues forgone for those bonds would be about $3 billion per year.

Much of that federal cost represents benefits to the state and local governments that issue the bonds (by allowing them to offer a lower interest rate on their bonds), but some of that cost goes to benefits that accrue only to certain bondholders. Bondholders with higher marginal tax rates save more than those with lower marginal tax rates. To appeal to some investors whose tax rates are lower or who find the bonds less attractive for other reasons, bond issuers must offer interest rates that are higher than those required to attract investors with higher tax rates. The benefits received by those bondholders who save more in taxes than is necessary to compensate them for the lower interest rates of the tax-exempt bonds represent costs to the federal government that do not benefit the bond issuers.

Tax Credit Bonds. The federal government has also supported the issuance of tax credit bonds by state and local governments at certain times. Most recently, state and local governments were authorized to issue Build America Bonds in 2009 and 2010. Those direct-pay tax credit bonds required the federal government to make cash payments to the bonds’ issuer equal to a portion of the interest that the issuer paid to bondholders. That allowed the issuer to offer a higher rate of return on the bonds, which was necessary to offset the tax liability that bondholders would incur on the interest they received. For every $100 in interest paid to holders of Build America Bonds, an issuer would receive $35 from the federal government, resulting in a credit rate of 35 percent. For tax credit bonds that were authorized in earlier periods, the form of federal support differed: An annual federal income tax credit was provided to bondholders instead of, or in addition to, the interest that would typically be paid on the bonds.

The cost to the federal government of tax credit bonds depends on the amount of subsidy that is authorized. Tax credit bonds could, however, provide the same amount of support to their issuers as tax-exempt bonds at a federal cost that is 28 percent lower than that of tax-exempt bonds, CBO estimates. That difference exists because the entire federal cost of a tax credit bond benefits the issuer, whereas part of the cost of tax-exempt bonds provides a subsidy to bondholders with high marginal tax rates.

Direct Federal Credit Programs

The Transportation Infrastructure Finance and Innovation Act (TIFIA) program provides credit assistance to state and local governments primarily for highway and mass transit infrastructure, although it can be used for a broad range of surface transportation projects. Outlays provided through the TIFIA program are paid out of the Highway Trust Fund.

The Department of Transportation must approve a state or local government’s application for TIFIA assistance. To qualify, a project must cost at least $50 million, though the minimum cost is lower for rural or local projects ($10 million) and for intelligent transportation system projects ($15 million). Projects receiving TIFIA assistance are expected to attract other public and private investment in addition to the federal support. Examples of TIFIA-funded projects include the Central 70 Project in Colorado, which will redesign, reconstruct, and add capacity to a section of Interstate 70 in Denver; the Monroe Expressway toll road in North Carolina; and the Portsmouth Bypass in Ohio.

The TIFIA program lends at Treasury bond rates for up to 35 years. In addition, repayment is deferred until 5 years after a project is substantially complete, and TIFIA loans have a subordinated status, meaning that a project’s other lenders and equity investors retain rights to be repaid before the federal government (unless the borrower defaults and enters bankruptcy, in which case the TIFIA loan takes a priority equal to that of the project’s senior debt). In practice, TIFIA loan amounts have typically been limited to about 33 percent of a project’s eligible costs, though borrowers may apply for loans of up to 49 percent of eligible costs.

The budgetary cost of TIFIA loans depends on the riskiness of the loans made and thus varies from year to year. In 2019, TIFIA provided about $1.5 billion in loans; to do so, it used $98 million of its budget authority at an estimated subsidy rate of 6.3 percent, or a federal cost of 6.3 cents per dollar financed.23 To estimate the subsidy rate for loans made in a given year, the Department of Transportation uses a model that it recently updated in consultation with the Treasury Department and the Office of Management and Budget (OMB). Using that model, OMB estimates that the subsidy rate of loans made in 2021 will be 1 percent.24

Those official budgetary estimates do not reflect the cost of market risk—the risk that arises because borrowers are more likely to default on their debt obligations when the economy is performing poorly—but under the fair-value accounting method, that risk is taken into account.25 Using the fair-value method, CBO estimates that the loans made under the program in 2021 will have a subsidy rate of 24 percent. Those rates may increase in subsequent years when Treasury interest rates are projected to rise as the economy recovers from the disruptions caused by the coronavirus pandemic.

State Infrastructure Banks

State infrastructure banks are financial institutions that state governments create and run to lend money to fund infrastructure projects. SIBs established for highway and mass transit projects do not receive designated federal grants each year, but state governments may decide to use some of the federal formula grants that they receive for highways and mass transit to capitalize them. Some banks choose to increase their current lending capacity by issuing tax-exempt bonds, thus receiving a second form of federal support. Most of the financial support that SIBs have provided has gone to highway projects.

Of the 33 states that have established SIBs, only about a dozen have actively used them. From 2007 to 2016, average annual financing for highway infrastructure provided by SIBs amounted to $200 million (in 2019 dollars), or about 1 percent of the total amount of new financing by state and local governments that the federal government subsidized each year. The data necessary to estimate the federal costs of financing SIBs are unavailable.26

Options

Changes to federal programs that support the financing of state and local highway capital projects could expand the amount of investment that occurred on federal-aid highways by making state and local investments less costly to finance. Policymakers could establish a new program to provide state and local governments with the opportunity to issue new tax credit bonds. Or they could expand existing financing programs. Another option federal lawmakers could pursue is to allow more tolling on Interstate highways, thereby providing states with a revenue stream that could be borrowed against. If those options were implemented and state and local governments expanded their use of the financing mechanisms, the federal costs would, in most cases, take the form of forgone federal revenues. TIFIA outlays, however, are paid out of the Highway Trust Fund, so expansions of that program would affect the shortfall in the trust fund.

Institute a Tax Credit Bond Program. Instituting a new tax credit bond program that was similar to the Build America Bonds program that was active in 2009 and 2010 would provide state and local governments with an additional option for issuing debt to finance capital spending. Tax credit bonds could offer state and local governments the same federal subsidy as tax-exempt bonds at a lower cost to the federal government.

Whereas CBO estimates that 20-year tax-exempt bonds issued by state and local governments in 2023 would cost the federal government 26 cents for each dollar financed, tax credit bonds issued that same year (with the same maturity and the same federal subsidy of a 22 percent reduction in interest costs) would cost the federal government 19 cents per dollar financed. In other words, for the same federal cost as traditional tax-exempt bonds, the federal government could, by authorizing tax credit bonds, provide state and local governments with a subsidy that was 39 percent larger, thereby reducing their financing costs more than tax-exempt bonds would. Ultimately, the federal cost of such a program would depend on the amount of subsidy that lawmakers authorized and the amount of bonds that state and local governments issued.

Tax credit bonds might offer one further advantage over tax-exempt bonds—they might appeal to a broader set of investors, particularly those with little or no tax liability, such as pension funds and other tax-exempt organizations.

Raise the Cap on Highway QPABs. Of the $15 billion in qualified private activity bonds allowed to be issued for highway and other surface transportation projects, about $12 billion in such bonds had been issued as of April 2020, and another $2 billion in such bonds had been approved by the Department of Transportation but had not yet been issued. (In the past, some projects that received a QPAB allocation switched to other forms of financing, so many of those bonds that have had funds allocated for them but that have not been issued may never be issued.)27

Giving private entities access to the tax-exempt bond market through QPABs lowers the cost of capital for those borrowers and can promote infrastructure projects when state and local governments have self-imposed limits on borrowing. Development of large, complex infrastructure projects often takes years, so the limit on the use of QPABs for funding highway and surface transportation projects reduces the certainty that the bonds would still be available if developers chose to apply for them in the future.

If the availability of QPABs increased and their use became more widespread, federal costs would go up. Like tax-exempt bonds, QPABs result in forgone federal revenues. Another consideration in weighing this option is that, to the extent that private funding was available to developers without QPABs (albeit at a higher cost), the only projects that would be unable to receive financing without them would be those of marginal value.

Expand the TIFIA Program. From 2015 through 2019, 19 highway and bridge projects received financing through the Transportation Infrastructure Finance and Innovation Act program. The average total cost per project was $1 billion, and each received, on average, $314 million in TIFIA loans. The smallest project to receive assistance had a total cost of $127 million; the TIFIA loan for that project totaled $47 million.

The financing assistance provided through TIFIA is paid for with outlays from the Highway Trust Fund, so expanding the program would increase the trust fund’s shortfall if no changes were made to the revenues credited to the fund.

Lawmakers have several different options for expanding TIFIA financing: