At a Glance

In this report, the Congressional Budget Office describes its long-term projections for Social Security. One set of projections reflects a scenario in which the program continues to pay benefits as scheduled under current law, regardless of whether the program’s two trust funds have sufficient balances to cover those payments. Another set of projections reflects a scenario in which Social Security outlays are limited to what is payable from annual revenues after the combined trust funds are exhausted, which, in CBO’s current projections, occurs in fiscal year 2033.

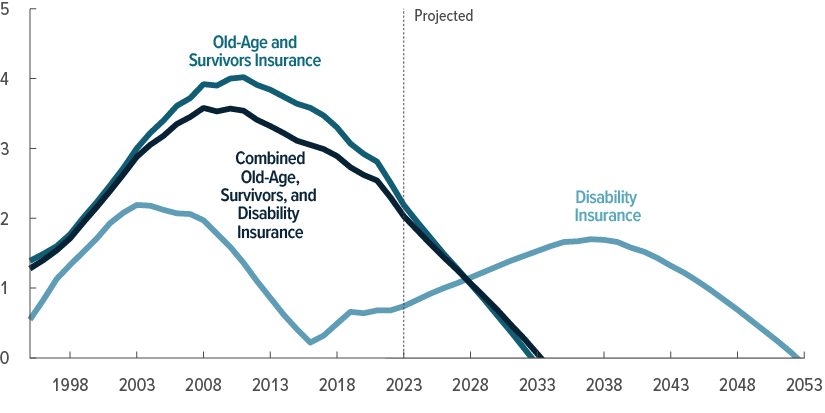

In CBO’s projections, the Old-Age and Survivors Insurance Trust Fund is exhausted in fiscal year 2032, and the Disability Insurance Trust Fund is exhausted in calendar year 2052. Social Security’s actuarial deficit over the next 75 years is equal to 1.7 percent of GDP, or 5.1 percent of taxable payroll.

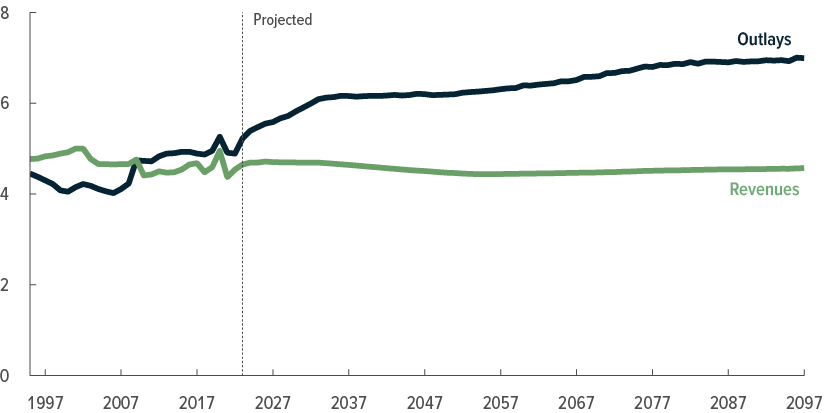

- Social Security’s Finances, With Scheduled Benefits. CBO projects that if Social Security paid benefits as scheduled, spending on the program would increase from 5.2 percent of gross domestic product (GDP) in 2023 to 7.0 percent in 2097; that increase is attributable to the increase in the average age of the population. Revenues would remain around 4.6 percent of GDP over the same period. After 2097, however, the gap between revenues and outlays would widen, and shortfalls would continue to increase.

- Distribution of Scheduled Benefits and Payroll Taxes. In CBO’s projections, average real (inflation-adjusted) initial retirement and disability benefits increase over time. Initial retirement benefits replace slightly larger shares of past earnings for later cohorts than earlier cohorts. Payroll taxes paid over the lifetime, measured as a percentage of lifetime earnings, do not change much for successive cohorts. Within cohorts, people with higher earnings generally receive larger benefits than people with lower earnings, but those larger benefits replace a smaller share of preretirement earnings. People with higher earnings pay a smaller share of lifetime earnings as payroll taxes.

- Social Security’s Finances, With Payable Benefits. CBO projects that if Social Security outlays were limited to what is payable from annual revenues after the combined trust funds’ exhaustion in fiscal year 2033, Social Security benefits would be 25 percent smaller than scheduled benefits in 2034. They would be 30 percent smaller in 2097 and later years.

- Distribution of Payable Benefits. After the combined trust funds’ exhaustion in the payable-benefits scenario, average retirement benefits in the first year of claiming resume their growth, but those benefits are smaller than scheduled benefits for people born after 1968 (that is, those who turn 65 after 2033).

Notes

The Congressional Budget Office’s long-term projections for Social Security typically follow the agency’s 10-year baseline budget projections and then extend most of the concepts underlying those projections. This year, however, the long-term projections are based on the agency’s May 2023 baseline projections but also reflect the estimated budgetary effects of the Fiscal Responsibility Act of 2023 (FRA, Public Law 118-5), enacted on June 3, 2023. Other legislation enacted between March 30, 2023 (when CBO finalized its May baseline), and June 3, 2023, did not have significant budgetary effects.

The projections are consistent with the demographic projections that the agency published on January 24, 2023, and the economic forecast that it published on February 15, 2023. Through 2053, the budget projections in this report reflect the macroeconomic effects of legislation enacted through December 6, 2022, when the economic forecast was finalized; after 2053, the projections do not account for such effects. They do not reflect the economic effects of administrative actions, regulatory changes, legislation, or economic developments after December 6, 2022, nor do they reflect the budgetary effects of any developments after March 30, 2023, except for the enactment of the FRA.

For additional discussion of CBO’s long-term projections over the 2023–2053 period, see Congressional Budget Office, The Long-Term Budget Outlook: 2023 to 2053 (June 2023), www.cbo.gov/publication/59014.

Some projections in this report are based on a scheduled-benefits scenario in which Social Security continues to pay benefits as scheduled under current law, regardless of the status of the program’s trust funds. That approach is consistent with statutory requirements governing CBO’s baseline projections and reflects the assumption that funding for such programs will be adequate to make all payments required by law. See section 257(b)(1) of the Balanced Budget and Emergency Deficit Control Act of 1985, P.L. 99-177 (codified at 2 U.S.C. §907(b)(1) (2016)).

Other projections in this report reflect a payable-benefits scenario. In the years after the trust funds’ exhaustion, revenues would be insufficient to pay benefits specified in law, and the Social Security Administration would no longer be able to pay beneficiaries the full amounts to which they were entitled. In that scenario, CBO assumes that annual outlays would be limited to annual revenues credited to the program once the trust funds were exhausted.

Tax revenues shown in the projections for Social Security outlays and revenues with scheduled and payable benefits are consistent with projected tax revenues under the payable-benefits scenario; they would be slightly higher if scheduled benefits were paid because revenues from income taxes paid on those benefits would be higher.

Birth cohorts are groups of Social Security participants who were born in the same decade.

Projections of the distribution of initial benefits and initial replacement rates in this report exclude disabled workers born in the 1950s because no data are available for people who died before 1984, which means the data for that cohort are incomplete.

Unless this report indicates otherwise, the years referred to are calendar years. Federal fiscal years run from October 1 to September 30 and are designated by the calendar year in which they end.

Numbers in the text, table, and figures may not add up to totals because of rounding.

Supplemental data for this analysis are available at www.cbo.gov/publication/59184.

Background

Social Security—the largest single program in the federal budget—has two components. Old-Age and Survivors Insurance (OASI) provides benefits to retired workers, their eligible dependents, and some survivors of deceased workers. Disability Insurance (DI) provides benefits to disabled workers and their dependents.

The program is financed by payroll taxes and income taxes on benefits that are credited to the OASI and DI trust funds. The payroll tax, which accounts for 96 percent of the revenues, is generally 12.4 percent of earnings up to a maximum annual amount ($160,200 in 2023). Workers and their employers each pay half; self-employed people pay the entire amount. In addition to tax revenues, the trust funds also receive intragovernmental interest payments on the Treasury securities they hold. Although the two trust funds are legally separate, in some of its analyses, the Congressional Budget Office considers them as combined trust funds, known as the Old-Age, Survivors, and Disability Insurance (OASDI) trust funds.

Outlays for Social Security consist of benefit payments and the program’s administrative costs.

As discussed in this report, the program’s revenues consist of receipts from the payroll tax and the income tax on benefits. (If transfers are made from the general fund of the Treasury, they are also shown as revenues.) Revenues do not include interest credited to the Social Security trust funds.

Social Security Outlays and Revenues in 2022

Percentage of Gross Domestic Product

In 2022, outlays from the OASI fund were greater than revenues. For the DI fund, outlays were similar to revenues.

The Outlook for Social Security: 2023 to 2097

CBO’s long-term projections of Social Security’s finances under a scheduled-benefits scenario reflect the assumption that benefits will be paid as scheduled under the provisions of the Social Security Act, regardless of balances in the Social Security trust funds. (For details about the basis for those projections, see Notes. For more information about what would happen to benefit payments if the balances were exhausted, see Appendix A.)

In CBO’s projections under a scheduled-benefits scenario, spending for Social Security increases rapidly in relation to gross domestic product (GDP) over the next decade as the large baby-boom generation continues to reach retirement ages. Growth then slows as members of that generation die and people from later generations become eligible for Social Security, but spending continues to rise throughout the 75-year projection period because life expectancy increases. Growth in spending for Social Security relative to GDP would continue after 2097.

Unlike outlays, revenues for Social Security remain stable in relation to the size of the economy. Payroll tax revenues decrease slightly, and receipts from income taxes on Social Security benefits increase slightly. Those changes offset each other, so the amount of tax revenues credited to the trust funds remains roughly unchanged as a percentage of GDP, a trend that would continue after 2097.

CBO’s projections of Social Security’s spending and revenues are subject to considerable uncertainty. If the population or economy differ from the agency’s projections, then spending and revenues will differ as well. Those differences could be especially large in the later years of the projection period because differences in the underlying projections would compound over time.

Social Security Outlays and Revenues, With Scheduled Benefits

Percentage of Gross Domestic Product

In CBO’s projections, the gap between Social Security’s outlays and revenues widens over the long term. Total spending on the program in 2023 is equal to 5.2 percent of GDP; by 2097, spending on the program reaches 7.0 percent of GDP. Over the same period, revenues remain at about 4.6 percent of GDP.

Social Security’s Finances, With Scheduled Benefits

Two measures are commonly used to assess Social Security’s finances. The program’s actuarial balance, often measured over 75 years, summarizes Social Security’s current trust fund balance and annual future streams of revenues and outlays as a single number. (A negative actuarial balance is called an actuarial deficit.) The trust fund ratio, or the ratio of the balance of a trust fund to its expected outlays in that year, indicates how much of recipients’ annual benefit amounts could be paid from the balance at the beginning of a given year. (See Appendix B for definitions of those and other terms.)

Actuarial Balance

In CBO’s projections, the program’s 75-year actuarial deficit is equal to 1.7 percent of GDP, or 5.1 percent of taxable payroll, which is slightly higher than what CBO projected last year. (See Appendix C for more information on changes since last year.) In other words, the federal government could pay the benefits prescribed by current law through 2097 and have a trust fund balance equal to a year’s benefits at the end of that period if payroll tax rates were raised immediately and permanently by about 5.1 percentage points—from 12.4 percent of taxable payroll under current law to 17.5 percent of taxable payroll, a relative rise of 41 percent. Other ways to maintain the necessary trust fund balances include reducing scheduled benefits by an amount equivalent to 5.1 percent of taxable payroll (a relative reduction in benefits of 27 percent), combining tax increases with benefit reductions, or transferring money to the trust funds. (This analysis excludes the effects of changes in taxes or spending on people’s behavior and the economy, which would depend on the specifics of the policy change and would change the required tax increase or benefit reduction.)

Summarized 75-Year Financial Measures for Social Security, With Scheduled Benefits

The income rate for Social Security measures income to the program from taxes as a percentage of GDP or taxable payroll; the cost rate measures the program’s cost as a percentage of GDP or taxable payroll. (For more details, see Appendix B.)

Sustainability

A policy that increased revenues or reduced outlays by the same percentage of taxable payroll each year (or made an equivalent combination of such changes) to eliminate the 75-year shortfall would not ensure Social Security’s solvency after 2097. Estimates of the actuarial deficit do not account for revenues or outlays after the 75-year projection period ends, but CBO projects that the gap between revenues and outlays would widen thereafter. Although such a policy would create annual surpluses in the next three decades, it would result in growing annual deficits later and would not leave Social Security on a sustainable financial path after 2097.

Trust Fund Ratios

In CBO’s projections, the amount in the OASI trust fund continues to steadily decline in relation to outlays as expenditures outpace income to the fund.

By contrast, the amount in the DI trust fund increases in relation to outlays in each of the next 14 years as income to the fund exceeds expenditures. Thereafter, the DI trust fund ratio declines.

Because the balance of the OASI trust fund comprised 96 percent of the total balance of the combined OASDI trust funds at the beginning of 2023, the ratio for the combined trust funds tends to follow trends in the ratio for the OASI trust fund.

Social Security Trust Fund Ratios

Ratio of Trust Fund Balance to Scheduled Payments

A trust fund is exhausted when its balance reaches zero. In CBO’s projections, the OASI trust fund is exhausted in fiscal year 2032 and the DI trust fund is exhausted in 2052. If their balances were combined, the OASDI trust funds would be exhausted in fiscal year 2033.

The Distribution of Scheduled Benefits and Payroll Taxes

Benefits for Retired Workers

In CBO’s projections, initial Social Security benefits—that is, benefits in the first full year of claiming, adjusted to remove the effects of inflation—grow over time in a scheduled-benefits scenario because real (inflation-adjusted) earnings are expected to continue to rise. That growth is partly offset for some birth cohorts because the increase in the full retirement age from 66 (for people born from 1943 to 1954) to 67 (for people born after 1959) reduces their initial benefits. (The analysis of initial benefits reflects the assumption that all eligible beneficiaries would claim benefits at age 65.) In addition, initial Social Security benefits are larger, on average, for retired workers with higher lifetime household earnings because people’s Social Security benefits are based on their earnings history.

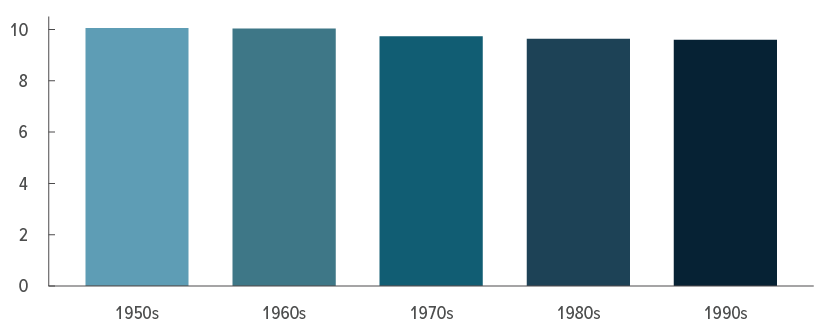

Average Initial Annual Benefits for Retired Workers, by Birth Cohort

2023 Dollars

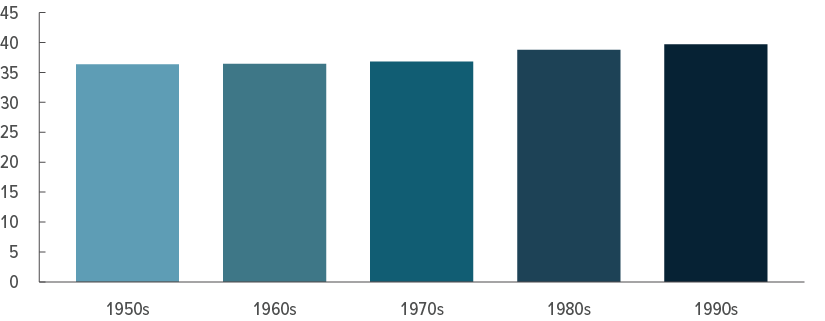

In CBO’s projections, average initial scheduled benefits for retired workers increase over time, after adjusting to remove the effects of inflation. For example, initial benefits are larger, on average, for people born in the 1990s (who turn 65 beginning in 2055) than for earlier cohorts.

Average Initial Annual Benefits for Retired Workers, by Birth Cohort and Earnings Quintile

2023 Dollars

Within a given cohort, retired workers with higher lifetime household earnings generally receive larger initial benefits. Across cohorts, average initial benefits are projected to increase for all earnings quintiles (or fifths of the distribution), three of which are shown here.

Replacement Rates for Retired Workers

In CBO’s projections, the share of preretirement earnings that Social Security benefits replace increases slightly over time. The program’s benefit formula is designed to be progressive: People who have lower lifetime earnings receive benefits that are larger, as a percentage of their lifetime average earnings, than those received by higher-earning beneficiaries. (For more details, see Appendix B.) Accordingly, initial replacement rates are higher, on average, for retired workers with lower earnings—that is, initial benefits replace a larger share of past earnings for those workers.

Average Initial Replacement Rates for Retired Workers, by Birth Cohort

Percent

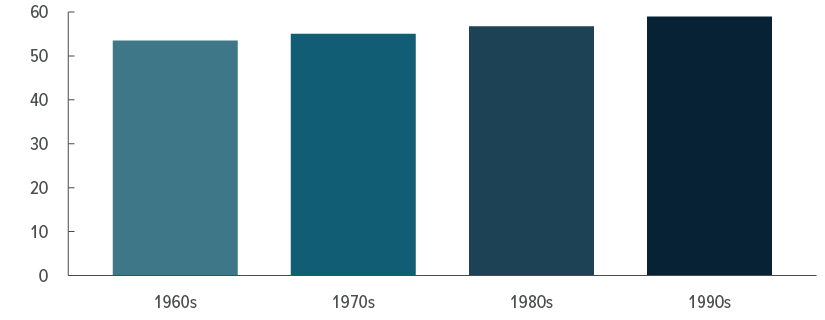

In CBO’s projections, initial benefits replace slightly larger shares of average past earnings for later cohorts of retired workers than the earlier cohorts.

Average Initial Replacement Rates for Retired Workers, by Birth Cohort and Earnings Quintile

Percent

Initial replacement rates are higher for later cohorts than for earlier cohorts in the lowest quintile (or fifth) of lifetime household earnings, whereas they change only slightly for those in the middle and highest earnings quintiles. That is because earnings for low earners are projected to grow more slowly than average wages.

Benefits and Replacement Rates for Disabled Workers

If benefits are paid as scheduled, then initial benefits for disabled workers (adjusted for inflation) will be larger in the future than they are today, CBO projects, because real earnings will continue to rise. The average initial replacement rates for disabled workers are projected to increase slightly over time.

Average Initial Annual Benefits for Disabled Workers, by Birth Cohort

2023 Dollars

In CBO’s projections, average DI benefits (adjusted for inflation) in the first full year of claiming increase over time. For example, initial benefits for disabled workers born in the 1990s are larger, on average, than for earlier cohorts.

Average Initial Replacement Rates for Disabled Workers, by Birth Cohort

Percent

Over time, initial DI benefits replace slightly larger shares of disabled workers’ previous earnings because the earnings of disabled workers tend to be low, and earnings for low earners are projected to grow more slowly than average wages.

Social Security Payroll Taxes Over People’s Lifetimes

People with higher earnings generally pay more in Social Security payroll taxes (in dollars) than people with lower earnings. But those taxes tend to make up a smaller share of lifetime earnings for people in the highest earnings quintile than for people with lower earnings. That is because annual earnings in excess of a maximum taxable amount ($160,200 in 2023) are not subject to the tax. (Earnings above the taxable maximum are excluded from calculations for Social Security benefits.)

Average Lifetime Social Security Taxes as a Percentage of Lifetime Earnings, by Birth Cohort

Percent

In CBO’s projections, about 10 percent of people’s lifetime earnings goes toward Social Security payroll taxes. Those amounts are less than the current payroll tax rate because some people have earnings above the maximum annual amount that is subject to the tax and because payroll tax rates were lower in the past.

Average Lifetime Social Security Taxes as a Percentage of Lifetime Earnings, by Birth Cohort and Earnings Quintile

Percent

Because earnings over a certain threshold are not taxed, people in the highest earnings quintile tend to pay a smaller share of their earnings in payroll taxes. In CBO’s projections, that pattern does not change much over time.

Social Security’s Finances, With Payable Benefits

Like CBO’s baseline budget projections, the projections discussed so far reflect the assumption that Social Security will continue to pay benefits as scheduled under the provisions of the Social Security Act, regardless of the balances in the Social Security trust funds. To show how the exhaustion of the trust funds might affect benefits, CBO also projects Social Security benefits under the assumption that they would be limited to the amounts payable from dedicated funding sources.

When the balance in the trust funds declines to zero, the Social Security Administration will no longer be able to pay full benefits when they are due (though beneficiaries will remain legally entitled to full benefits). In the years after the trust funds’ exhaustion, annual outlays would be limited to annual revenues, and payments to beneficiaries would be reduced. (The method for reducing payments is not prescribed under current law.) Therefore, in CBO’s projections, payable benefits would equal scheduled benefits until the combined trust funds are exhausted in fiscal year 2033; after that, payable benefits are the same as the program’s annual revenues.

In 2034, Social Security revenues are projected to equal 75 percent of the program’s scheduled outlays, resulting in a 25 percent shortfall. Thus, CBO estimates that Social Security benefits would be reduced by 25 percent in 2034 under the payable-benefits scenario. The gap between scheduled and payable benefits would equal 30 percent by 2097, and that gap would remain stable thereafter. (See Appendix A for more information.)

Social Security Outlays and Revenues, With Scheduled and Payable Benefits

Percentage of Gross Domestic Product

In CBO’s projections, outlays in a payable-benefits scenario are about 4.6 percent of GDP in 2097, lower than the 7.0 percent projected in a scheduled-benefits scenario.

The Distribution of Payable Benefits

In CBO’s projections for the payable-benefits scenario, Social Security benefit payments are reduced after the combined trust funds’ exhaustion in fiscal year 2033. Therefore, initial benefits for people who begin collecting benefits after the exhaustion are smaller than they would be under the scheduled-benefits scenario. Beneficiaries in earlier cohorts who start claiming benefits before 2034 see no change to their initial benefits. However, because they receive smaller benefits after the trust funds’ exhaustion, their lifetime benefits are smaller than they would be under the scheduled-benefits scenario.

Reductions in Average Initial Benefits for Retired Workers Under a Payable-Benefits Scenario, by Birth Cohort

2023 Dollars

In CBO’s projections, payable benefits fall short of scheduled benefits beginning in 2034, when workers born in 1969 turn 65. As a result, average payable benefits fall by a small amount for the 1960s cohort and more for later cohorts.

Reductions in Average Lifetime Benefits for All Social Security Beneficiaries Under a Payable-Benefits Scenario, by Birth Cohort

2023 Dollars

For all cohorts, average lifetime Social Security benefits are smaller in the payable-benefits scenario than in the scheduled-benefits scenario because at least some members of every cohort experience benefit reductions in some years. That decline in lifetime benefits is smaller for earlier cohorts, who begin collecting benefits before the combined trust funds are exhausted.

Appendix AScheduled Benefits and Payable Benefits

In accordance with statutory requirements, the Congressional Budget Office produces its baseline budget projections under the assumption that funding for entitlement programs will be adequate to make all payments required by law. Likewise, in this report, CBO’s projections of Social Security’s finances with scheduled benefits reflect the assumption that the Social Security Administration will pay benefits as scheduled under current law regardless of the status of the program’s trust funds.1

Without legislative action, CBO projects the combined Old-Age, Survivors, and Disability Insurance trust funds would be exhausted in fiscal year 2033. Beyond that point, the trust fund balances would no longer be sufficient to make up the gap between benefits specified in current law and annual trust fund receipts.

If a trust fund was depleted and its expenditures continued to exceed its receipts, two federal laws would come into conflict. Under the Social Security Act, beneficiaries would remain legally entitled to full benefits. However, under the terms of the Antideficiency Act, the Social Security Administration would not have legal authority to pay those benefits on time. (That act prohibits government spending in excess of available funds.) It is unclear what specific actions the Social Security Administration would take if a trust fund was insolvent.2

There are many ways to restore Social Security’s solvency after the trust funds’ projected exhaustion. For example, benefits could be reduced to decrease expenditures from the trust funds, payroll tax rates could be raised, or funds could be transferred from the Treasury’s general fund to increase Social Security’s income.

In CBO’s projections of Social Security’s finances with payable benefits, benefits are limited to the amounts payable from dedicated funding. That is, payable benefits are reduced as necessary to ensure that outlays do not exceed the Social Security system’s revenues once the balances in the combined trust funds are exhausted. Under this scenario, the trust funds’ annual income and expenditures are equal. Because Social Security outlays would be lower under the payable-benefits scenario than under the scheduled-benefits scenario, federal deficits and debt under the payable-benefits scenario would be lower than under the scheduled-benefits scenario. Because CBO’s projections incorporate macroeconomic effects through 2053, the lower debt and deficits would lead to faster growth in gross domestic product (GDP) and higher levels of GDP under the payable-benefits scenario after the trust funds are projected to be exhausted than under the scheduled-benefits scenario.

How outlays would be reduced is not specified in law. For this report, CBO assumed that once the combined trust funds were exhausted, Old-Age and Survivors Insurance benefits and Disability Insurance benefits paid to all existing and new beneficiaries would be reduced by the percentages necessary to make the program’s total annual outlays equal its total available revenues.

1. Sec. 257(b)(1) of the Balanced Budget and Emergency Deficit Control Act of 1985, Public Law 99-177 (codified at 2 U.S.C. §907(b)(1) (2016)).

2. Barry F. Huston, Social Security: What Would Happen If the Trust Funds Ran Out? Report RL33514, version 34 (Congressional Research Service, September 28, 2022), https://tinyurl.com/3v5t6a28.

Appendix BDefinitions

The actuarial balance is a common measure of the sustainability of a program that has a trust fund and a dedicated revenue source. The actuarial balance is the sum of the present value of projected income and the current trust fund balance minus the sum of the present value of projected outlays and a year’s worth of benefits at the end of the period. (The present value expresses a flow of current and future income or payments in terms of an equivalent lump sum received or paid today.) For Social Security, that difference is traditionally presented as a percentage of the present value of gross domestic product (GDP) or of taxable payroll over 75 years.

The actuarial balance is also the difference between the income rate and the cost rate. The income rate is the present value of annual income plus the initial trust fund balance, divided by the present value of GDP or of taxable payroll, over the 75-year period. The cost rate is the present value of annual outlays plus the present value of a year’s worth of benefits at the end of the period, divided by the present value of GDP or of taxable payroll over the same period. A negative actuarial balance is called an actuarial deficit.

The Social Security Administration calculates the benefit paid to a retired worker who claims benefits at the full retirement age or to a disabled worker using its benefit formula. That formula is applied to workers’ average indexed monthly earnings (AIME)—a measure of their average taxable monthly earnings over their 35 highest-earning years. AIMEs are separated into three brackets using two threshold amounts, or bend points. In calendar year 2023, the first bend point is $1,115, and the second is $6,721. AIMEs in the three brackets are multiplied by 90 percent, 32 percent, and 15 percent, respectively, to calculate the primary insurance amount (PIA), with the largest factor applying to the lowest AIME bracket. The benefit formula is thus progressive; that is, because PIA factors are larger for lower earnings brackets, the benefit is larger as a share of lifetime earnings for someone with a lower AIME than it is for someone with a higher AIME.

Initial annual benefits for retired workers are the benefits people receive the first year they claim them. To remove the effects of inflation on initial benefits, the Congressional Budget Office used the GDP price index for all goods and services included in GDP. For this report, the agency computed initial benefits for all people who are eligible and who have not yet claimed any other Social Security benefits. All workers are assumed to claim benefits at age 65, and all amounts are net of income taxes paid on benefits.

The initial replacement rate for retired workers is the initial annual benefit amount measured as a percentage of workers’ preretirement earnings. For this report, preretirement earnings are defined as the average of the last five years of substantial earnings before age 62.1 (Substantial earnings are annual earnings amounting to at least half of a worker’s average indexed annual earnings—that is, average annual earnings over that person’s lifetime, adjusted for changes in average wages.) The preretirement earnings are adjusted to account for price increases and thus reflect the purchasing power of earnings over time. Replacement rates are computed for all individuals who are eligible to claim retirement benefits at age 62 and who have not yet claimed any other benefit. To take account of only those individuals with significant attachment to the labor force, workers with fewer than 20 years of earnings that are above 10 percent of average wages in the total economy in each year are excluded. All workers are assumed to claim benefits at age 65. All amounts are net of income taxes paid on benefits and credited to the Old-Age and Survivors Insurance (OASI) Trust Fund.

Initial annual benefits for disabled workers are the benefits people receive in the first year after being awarded Disability Insurance benefits. To remove the effects of inflation, CBO used the GDP price index for all goods and services included in GDP. All amounts are net of income taxes paid on benefits and credited to the Disability Insurance (DI) Trust Fund.

The initial replacement rate for disabled workers is a worker’s initial annual benefit amount measured as a percentage of the average of that worker’s last five years of substantial earnings. Those past earnings are adjusted to account for growth in prices and reflect the purchasing power of earnings over time.

Lifetime earnings are the present value of real (inflation- adjusted) earnings over a person’s lifetime at age 65, including earnings above the taxable maximum. To remove the effects of inflation, CBO used the GDP price index for all goods and services included in GDP. For someone who is single in all years, lifetime household earnings are the present value of real earnings over a lifetime. In any year in which a person is married, the measure of that person’s earnings is the average of the couple’s earnings, with adjustments to account for economies of scale in household consumption. CBO used lifetime earnings to estimate shares of earnings paid in taxes among cohorts, or groups of people born in the same decade. To examine differences across the distribution of earnings, CBO used lifetime household earnings to rank people in each cohort and sort them into quintiles, or fifths.

Lifetime Social Security benefits include the present value of all Social Security benefits (except those received by young widows, young spouses, and children), net of income taxes that some recipients pay on their benefits and are credited to the OASDI trust funds. (Those benefits received by young widows, young spouses, and children are excluded from this measure because of insufficient data for years before 1984.)

Lifetime Social Security taxes consist of the present value of the employer’s and employee’s combined payroll taxes.

The trust fund ratio is the balance in a trust fund at the beginning of the year divided by outlays (benefits and administrative costs) for that year. Trust fund exhaustion occurs when a fund’s balance, and thus its trust fund ratio, reaches zero. Under current law, a Social Security trust fund cannot incur negative balances.

1. For more information, see Congressional Budget Office, Social Security Replacement Rates and Other Benefit Measures: An In-Depth Analysis (April 2019), www.cbo.gov/publication/55038.

Appendix CChanges to CBO’s Projections of the 75-Year Actuarial Balance Since Last Year

The Congressional Budget Office’s current projections of Social Security’s 75-year actuarial deficit are slightly higher than last year’s projections. CBO projects that over the next 75 years, if current laws remained in place, the program’s actuarial deficit would be 1.7 percent of gross domestic product (GDP)—approximately the same amount that CBO estimated last year—or 5.1 percent of taxable payroll—which is higher than last year’s estimate of 4.9 percent.1

The current projections of the actuarial deficit reflect several developments since last year. Some factors made the actuarial deficit larger:

- CBO lowered its projections of interest rates in the long run, resulting in lower discount rates used to calculate the actuarial deficit. The cumulative effect of those lower discount rates placed greater weight on future years when projected financial shortfalls are larger, which therefore increased the actuarial deficit.

- CBO projected slower growth in real (inflation-adjusted) GDP starting in the mid-2040s and a smaller labor force after the mid-2050s. To remove the effects of inflation, CBO used the GDP price index for all goods and services included in GDP. As a result, projected Social Security revenues from payroll taxes decreased. Partly offsetting that decrease in revenues is a decrease in outlays driven by the slower growth in GDP. That decrease is gradual because future beneficiaries would only gradually begin to receive smaller benefits—on the basis of lower earnings—than they would otherwise have received. Because earlier years, which are projected to have larger financial shortfalls, receive more weight in the calculation of the actuarial balance, the overall effect of the slower GDP growth is an increase in the actuarial deficit.

- The projection period included an additional year with a relatively large deficit (2097).

Other factors partially offset those effects and made the actuarial deficit smaller:

- CBO lowered its projections of the long-run age- and sex-adjusted rate of disability incidence from 5.2 per 1,000 insured workers to 4.7 per 1,000 insured workers. The lower disability incidence rates resulted in lower projections of the number of people claiming Disability Insurance benefits and decreased outlays for Social Security. That revision of the disability incidence rate is based on analysis of historical patterns and expected future conditions. The rate has declined since 2010, when it peaked after the 2007–2008 financial crisis. CBO expects that the changing nature of work and increasing accommodations for workers with impairments will keep the rate below its average over the past 30 years. In addition, the unemployment rate is projected to remain lower than it has been over the past decade and to decline in the long term, and the disability incidence rate typically falls when the unemployment rate declines. The long-run disability incidence rate of 4.7 is consistent with the agency’s projected unemployment rates in the long run.2

- The population is projected to be larger and to grow slightly faster, on average, in this year’s projections than last year’s. CBO increased its projections of net immigration, which boosted the size and growth of the working-age population over the projection period.3

1. Because of CBO’s rounding conventions, the measure of actuarial deficit as a percentage of GDP does not appear to change compared to last year’s projections.

2. Congressional Budget Office, The 2023 Long-Term Budget Outlook (June 2023), Appendix D, www.cbo.gov/publication/59014.

3. Congressional Budget Office, The Demographic Outlook: 2023 to 2053 (January 2023), www.cbo.gov/publication/58612.

About This Document

This volume is one of a series of reports on the state of the budget and the economy that the Congressional Budget Office issues each year. In keeping with CBO’s mandate to provide objective, impartial analysis, the report makes no recommendations.

Xinzhe Cheng prepared the report with guidance from Molly Dahl and Julie Topoleski. Damir Cosic, Daniel Crown, Kyoung Mook Lim, Noah Meyerson, Charles Pineles-Mark, Emily Stern, and Jordan Trinh contributed to the analysis. Lucy Yuan fact-checked the report and the supplemental data.

Mark Doms, Jeffrey Kling, and Robert Sunshine reviewed the report. Caitlin Verboon edited it, and Jorge Salazar created the graphics and prepared the text for publication. Xinzhe Cheng prepared the supplemental data. The report is available at www.cbo.gov/publication/59184.

CBO seeks feedback to make its work as useful as possible. Please send comments to communications@cbo.gov.

Phillip L. Swagel

Director

June 2023