CBO’s Economic Forecasting Record: 2019 Update

CBO’s economic forecasts have been comparable in quality to those of the Administration and the Blue Chip consensus. Large errors in CBO’s forecasts tend to reflect challenges faced by all forecasters.

Summary

Each year, CBO prepares economic forecasts that underlie its projections of the federal budget. CBO forecasts hundreds of economic variables, but some—including output growth, the unemployment rate, inflation, interest rates, and wages and salaries—play a particularly significant role in the agency’s budget projections. To evaluate the quality of its economic projections, estimate uncertainty ranges, and isolate the effect of economic errors on budgetary projections, CBO regularly analyzes its historical forecast errors. That analysis serves as a tool for assessing the usefulness of the agency’s projections.

In this report, CBO evaluates its two-year and five-year economic forecasts from as early as 1976 and compares them with analogous forecasts from the Administration and the Blue Chip consensus—an average of about 50 private-sector forecasts published in Blue Chip Economic Indicators. External comparisons help identify areas in which the agency has tended to make larger errors than other analysts. They also indicate the extent to which imperfect information may have caused all forecasters to miss patterns or turning points in the economy.

How CBO Measures Forecast Quality

CBO’s analysis focuses on three metrics of forecast quality—mean error, root mean square error, and two-thirds spread of errors:

- The mean error is CBO’s primary measure of centeredness, which indicates how close the average forecast value is to the average actual value over time. Centeredness is the opposite of statistical bias, which quantifies the degree to which a forecaster’s projections are too high or too low over a period of time.

- The root mean square error is CBO’s primary measure of accuracy, or the degree to which forecast values are dispersed around actual outcomes.

- The two-thirds spread, computed as the range between the minimum and maximum errors after removing the one-sixth largest errors and the one-sixth smallest errors, illustrates a forecaster’s typical range of errors and provides information about the extent of the dispersion of those errors.

The Quality of CBO’s Forecasts

When a mean error is used to assess the quality of a forecast, the standard for comparison is a mean error of zero. A forecast that has a mean error of zero is, on average, neither too high nor too low. CBO’s forecasts of most economic variables tend to exhibit small positive mean errors—that is, on average, they are too high by small amounts. CBO’s forecasts of interest rates and growth in wages and salaries exhibit larger mean errors than its forecasts of other economic indicators.

When a root mean square error and spread are used to assess the quality of a forecast, there is no absolute standard for comparison. Moreover, it is difficult to compare quality measures across variables because magnitudes of variables can differ substantially, and some variables are relatively easy to forecast but others are relatively hard. It is possible, however, to compare those measures across forecast horizons for a given variable. For example, as measured by the root mean square error, CBO’s two-year forecasts of most variables are not appreciably more accurate than its five-year forecasts. For most variables, the agency’s two- and five-year forecasts exhibit a similar two-thirds spread of errors.

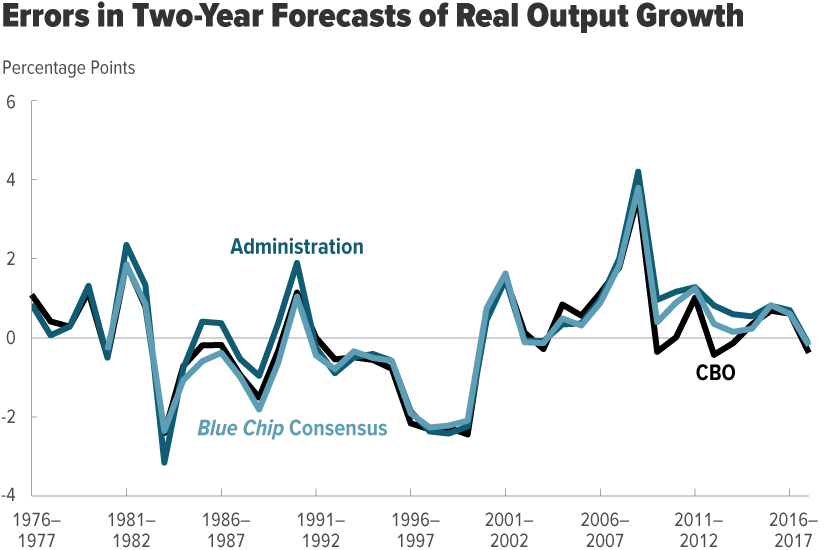

Comparing CBO’s Forecasts With the Administration’s Forecasts and the Blue Chip Consensus Forecasts

In general, forecasts produced by CBO, the Administration, and the Blue Chip consensus display similar error patterns over time. Because all forecasters faced the same challenges, periods in which CBO made large overestimates typically coincide with periods in which other forecasters made similarly large overestimates. Over time, however, even small differences in the magnitude of errors can result in appreciable differences in measures of forecast quality.

CBO and the Blue Chip consensus tend to produce less-biased forecasts of output growth but more-biased forecasts of interest rates than the Administration. As measured by the root mean square error, CBO’s forecasts tend to be slightly more accurate, on net, than the Administration’s forecasts and roughly comparable to the Blue Chip consensus forecasts. Finally, CBO’s forecasts tend to exhibit smaller two-thirds spreads than the Administration’s forecasts do; the agency’s forecasts tend to have two-thirds spreads that are similar to those of the Blue Chip consensus forecasts.

Sources of Forecast Errors

Forecasters made large errors in their economic forecasts as a result of several economic developments:

- Turning points in the business cycle;

- Changes in labor productivity trends;

- Changes in crude oil prices;

- The persistent decline in interest rates;

- The decline in the labor share—that is, labor income as a share of gross domestic product (GDP); and

- Data revisions.

Some of those developments resulted in errors in forecasting specific variables. Changes in crude oil prices, for example, resulted in misestimates of inflation in the consumer price index (CPI). Other developments, such as turning points in the business cycle, affect the entirety of an economic forecast, and their effects are observable in the error patterns of several variables.

How CBO Uses Its Forecast Errors to Estimate Uncertainty

CBO most frequently uses the root mean square error of its historical forecasts to quantify the uncertainty of its current economic projections. For example, CBO’s baseline forecast for real (inflation-adjusted) GDP growth over the next five years is 2.0 percent. Using its historical root mean square error for that variable (1.3 percentage points), CBO then estimates that there is approximately a two-thirds chance that the rate of real GDP growth over the next five years will be between 0.7 percent and 3.3 percent. Although the agency typically uses the historical root mean square error to estimate uncertainty, it uses the two-thirds spread of errors in instances where the statistical bias of its historical forecasts is high.