The Distribution of Household Income and Federal Taxes, 2013

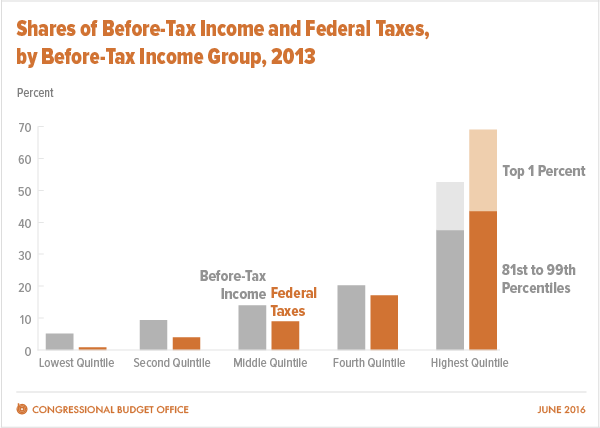

In 2013, households in the top, middle, and bottom income quintiles received 53, 14, and 5 percent, respectively, of the nation's before-tax income and paid 69, 9, and 1 percent, respectively, of federal taxes.

Summary

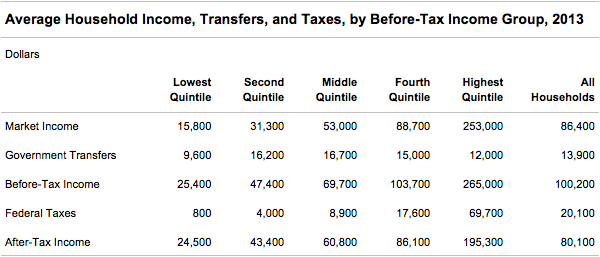

In 2013, according to the Congressional Budget Office’s estimates, average household market income—a comprehensive income measure that consists of labor income, business income, capital income (including capital gains), and retirement income—was approximately $86,000. Government transfers, which include benefits from programs such as Social Security, Medicare, and unemployment insurance, averaged approximately $14,000 per household. The sum of those two amounts, which equals before-tax income, was about $100,000, on average. In this report, CBO analyzed the distribution of four types of federal taxes: individual income taxes, payroll (or social insurance) taxes, corporate income taxes, and excise taxes. Taken together, those taxes amounted to about $20,000 per household, on average, in 2013. Thus, average after-tax income—which equals market income plus government transfers minus federal taxes—was about $80,000, and the average federal tax rate (federal taxes divided by before-tax income) was about 20 percent.

How Were Income and Federal Taxes Distributed in 2013?

Before-tax income was unevenly distributed across households in 2013. Average before-tax income among households in the lowest one-fifth (or quintile) of the distribution of before-tax income was approximately $25,000 in 2013, CBO estimates (see Table 1). Among households in the middle income quintile, average before-tax income was about $70,000. Households in the highest income quintile had average before-tax income that was much higher—approximately $265,000. In response to tax law changes that went into effect in 2013, some taxpayers—especially those at the top of the income distribution—shifted some income into 2012 to avoid the higher tax rates on that income in 2013. Because of that income shifting, income at the top of the distribution was lower in 2013 than it would have been in the absence of those tax law changes.

Overall, federal taxes are progressive, meaning that average tax rates generally rise as income increases. Households in the lowest income quintile paid less than $1,000 in federal taxes in 2013, on average, which amounted to an average federal tax rate of about 3 percent, CBO estimates. Households in the middle quintile paid about $9,000 in federal taxes, on average, and households in the highest quintile paid about $70,000; their average federal tax rates were approximately 13 percent and 26 percent, respectively.

Households in the highest income quintile received a little more than half of total before-tax income and paid more than two-thirds of all federal taxes in 2013 (see Figure 1). Households in other income groups received considerably smaller shares of before-tax income and paid considerably smaller shares of federal taxes. Furthermore, the share of taxes paid by households in other income groups (in contrast to households in the highest income quintile) was less than the share of before-tax income they received. Households in the middle income quintile, for instance, received about 14 percent of total before-tax income and paid about 9 percent of federal taxes. And households in the lowest income quintile received about 5 percent of before-tax income in 2013 and paid less than 1 percent of federal taxes, CBO estimates.

The progressive federal tax structure results in a distribution of after-tax income that is slightly more even than that of before-tax income. Households in the lowest income quintile received approximately 6 percent of after-tax income in 2013, compared with 5 percent of before-tax income, and households in the highest income quintile received about 49 percent of after-tax income, compared with 53 percent of before-tax income, CBO estimates.

What Are the Trends in the Distribution of Income, Federal Taxes, and Income Inequality?

The distributions of household income and federal taxes depend on economic conditions and tax laws—both of which have changed over time. Changes in the distribution of after-tax income can be traced to changes in the distributions of market income, government transfers, and federal taxes.

Income inequality varies depending on the measure of income examined. By comparing measures of income inequality based on income with and without government transfers (market income and before-tax income), it is possible to determine the degree to which government transfers reduce income inequality. Similarly, by comparing measures of income inequality based on income excluding or including the effects of federal taxes (before-tax income and after-tax income), it is possible to determine the degree to which federal taxes reduce income inequality.

Market and Before-Tax Income. Over the 35-year period from 1979 to 2013, average inflation-adjusted market and before-tax income increased for each income group. The cumulative growth rates for those income measures, however, differed significantly across the income distribution. Market income in 2013 for households in the top 1 percent was 188 percent higher than it was in 1979. For households in the bottom four income quintiles, market income was 18 percent higher in 2013 than it was in 1979.

Because government transfers largely go to low-income households, the cumulative growth in before-tax income for households in the bottom four quintiles was significantly higher than the cumulative growth in market income for households in similar market income quintiles. In addition, because of such transfers, the average cumulative growth in before-tax income for households in the lowest quintile was slightly higher than the average cumulative growth for households in the middle three income quintiles—39 percent versus 32 percent. Conversely, because high-income households receive relatively small amounts of government transfers, on average, the inflation-adjusted cumulative growth rates over the 35-year period for market and before-tax income were very similar for those households.

Average Federal Tax Rates. Average federal tax rates fluctuate over time because of changes in tax law and changes in the composition and distribution of income. Primarily because of significant changes in tax rules, average federal tax rates in 2013 were higher than in 2012 across the income distribution. Households in the bottom 99 percent of the income distribution saw their average federal tax rates increase by more than 1 percentage point, on average, between 2012 and 2013. Households in the top 1 percent of the income distribution, however, saw their average federal tax rates jump by more than 5 percentage points between 2012 and 2013. Those changes in average federal tax rates in 2013 made the federal tax system the most progressive it has been since at least the mid-1990s.

Despite the increases in tax rates in 2013, average federal tax rates in that year were below the 35-year average for most households. Average federal tax rates in 2013 for households in all but the top income quintile were significantly below the average rates over the 1979–2013 period. For the top quintile, the breakdown differs; the average tax rate in 2013 was slightly below the 35-year average for households in the 81st to 99th percentiles but well above the 35-year average for households in the top 1 percent of the income distribution (see Figure 2).

After-Tax Income. From 1979 to 2013, average after-tax income grew at significantly different rates for households at different points on the income scale. For households in the top 1 percent of the income distribution, inflation-adjusted after-tax income grew at an average rate of about 3 percent per year, making that income 192 percent higher in 2013 than it was in 1979 for those households.

In contrast, households in the bottom quintile experienced an average growth of about 1 percent per year in their inflation-adjusted after-tax income over the same period, making that income 46 percent higher in 2013 than it was in 1979, CBO estimates. Those differences in growth rates for after-tax income are largely attributable to differences in growth rates for market income, although changes in taxes and transfers had an effect as well.

Income Inequality. Between 1979 and 2013, all three measures of income examined in this report—market income, before-tax income, and after-tax income—became less equally distributed, based on a standard measure of inequality known as the Gini index. The increase in inequality in both before-tax and after-tax income over the 35-year period stemmed largely from a significant increase in inequality in market income, mostly because of substantial income growth at the top of the market income distribution.

Because government transfers go predominantly to lower-income households, before-tax income (which is equal to market income plus government transfers) was more evenly distributed in each year than market income. And because higher-income households pay a larger share of federal taxes than lower-income households do, after-tax income was more evenly distributed than before-tax income.

In each year between 1979 and 2013, government transfers reduced income inequality significantly more than the federal tax system did. The effects of federal taxes have been relatively stable since the 1990s, whereas the effects of government transfers have generally fluctuated with the business cycle. The equalizing effects of government transfers increased significantly during the recession that began in 2007. Unlike previous economic cycles, government transfers have had a sustained effect on reducing income inequality during the subsequent slow recovery.