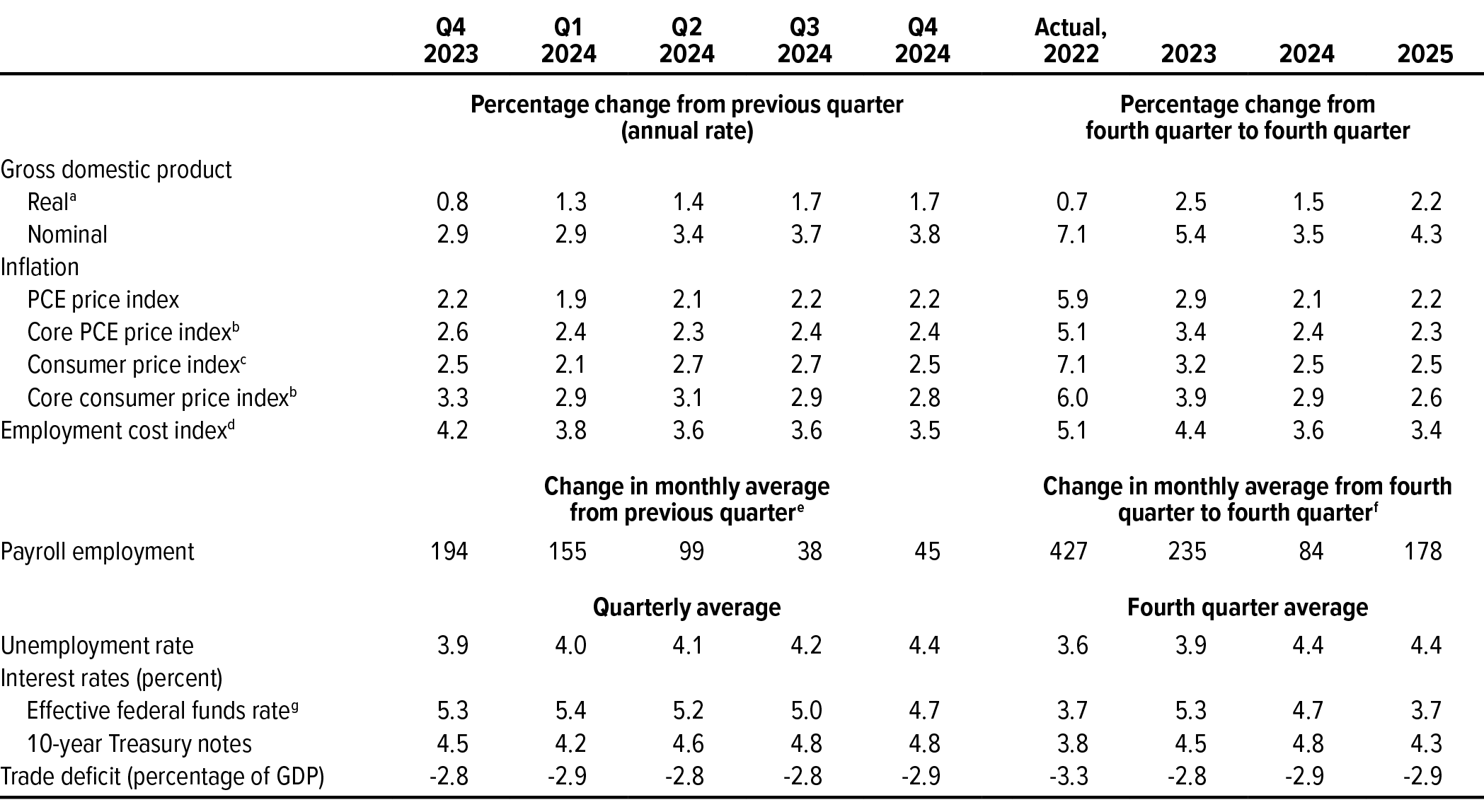

The Congressional Budget Office periodically updates its economic forecast to ensure that its projections reflect recent economic developments and current law. CBO will publish its budget and economic projections for 2024 to 2034 early next year in its annual Budget and Economic Outlook. This report provides details about CBO’s most recent projections of the economy through 2025, which reflect economic developments as of December 5, 2023 (see Table 1). CBO develops its economic projections so that they fall in the middle of the range of likely outcomes under current law. Those projections are highly uncertain, and many factors could lead to different outcomes. In CBO’s latest projections:

- Output growth slows in 2024 and rebounds in 2025. The growth of real gross domestic product (GDP, adjusted to remove the effects of inflation) falls from 2.5 percent in 2023 to 1.5 percent in 2024 as consumer spending weakens and investment in private nonresidential structures contracts. In 2025, real GDP growth rises to 2.2 percent, supported by lower interest rates and improved financial conditions. (Unless this report indicates otherwise, annual growth rates are measured from the fourth quarter of one year to the fourth quarter of the next.)

- Labor market conditions soften in 2024. Growth in payroll employment slackens, and the unemployment rate rises from 3.9 percent in the fourth quarter of 2023 to 4.4 percent in the fourth quarter of 2024 and remains close to that level through 2025. The labor force grows at a moderate pace, with an increased contribution to that growth stemming from projected immigration over the next two years.1

- Inflation continues to slow over the next two years and approaches the Federal Reserve’s target rate of 2 percent. As measured by the price index for personal consumption expenditures (PCE), inflation falls from 2.9 percent in 2023 to 2.1 percent in 2024, reflecting softer labor markets and slower increases in rents. In 2025, inflation rises slightly, to 2.2 percent, as downward pressures on inflation in food and energy prices ease and stronger economic activity modestly increases price pressures for some categories of services.

- Interest rates on Treasury securities peak in 2024 and then recede through 2025. The Federal Reserve holds the federal funds rate (the rate that financial institutions charge each other for overnight loans of their monetary reserves) between 5.25 percent and 5.50 percent through the first quarter of 2024 and then reduces it in response to slowing inflation and rising unemployment. The rate on 10-year Treasury notes increases to 4.8 percent in the second half of 2024 and begins to fall in mid-2025.

Table 1.

CBO’s Economic Projections for 2023 to 2025

Data sources: Congressional Budget Office; Bureau of Economic Analysis; Bureau of Labor Statistics; Federal Reserve. See www.cbo.gov/publication/59837#data.

GDP = gross domestic product; PCE = personal consumption expenditures.

a. Real values are nominal values that have been adjusted to remove the effects of changes in prices.

b. Excludes prices for food and energy.

c. The consumer price index for all urban consumers (CPI-U).

d. The employment cost index for wages and salaries of workers in private industries.

e. Monthly average values are calculated by dividing quarterly values by 3.

f. Changes in monthly averages are calculated by taking the value for the fourth quarter of a year, subtracting the value for the fourth quarter of the previous year, and dividing by 12.

g. The interest rate calculated by the Federal Reserve as a volume-weighted median of overnight federal funds transactions.

Compared with its February 2023 projections, CBO’s current projections exhibit weaker growth, lower unemployment, and higher interest rates in 2024 and 2025.2 The agency’s current projections of inflation are mixed relative to those made in February 2023.

- Slower economic growth during 2024 (by 1.0 percentage point) and 2025 (by 0.4 percentage points) largely occurs because of slower-than-projected growth in consumption, investment, and exports. The downward revision from those sources is partially offset by higher net immigration.

- The lower unemployment rate for 2024 and 2025, on average, is the result of faster-than-projected economic growth in 2023.

- Higher interest rates in 2024 and 2025 reflect stronger economic activity in 2023, which resulted in the Federal Reserve raising the target range for the federal funds rate higher than what CBO projected in February 2023.

- The upward revision to inflation in the consumer price index for all urban consumers (CPI-U) in 2025 (by 0.3 percentage points) reflects faster-than-expected growth in the cost of housing services. (The CPI-U places more weight on the cost of housing services than the PCE price index does.) PCE inflation in 2024 that is lower than previously projected (by 0.3 percentage points) stems from better-than-expected improvements in supply conditions affecting prices that receive more weight in the PCE price index than in the CPI-U.

1. See Testimony of Julie Topoleski, Director of Labor, Income Security, and Long-Term Analysis, before the Joint Economic Committee, CBO’s Demographic Projections (November 15, 2023), www.cbo.gov/publication/59683. CBO expects to publish its next comprehensive demographic projections in January 2024.

2. See Congressional Budget Office, The Budget and Economic Outlook: 2023 to 2033 (February 2023), www.cbo.gov/publication/58848.

The Congressional Budget Office prepared this report in response to interest expressed by Members of Congress. This document is one of a series of reports on the state of the economy that CBO issues each year. In keeping with the agency’s mandate to provide objective, impartial analysis, the report makes no recommendations.

CBO consulted members of its Panel of Economic Advisers during the development of this report. Although the agency’s outside advisers provided considerable assistance, they are not responsible for the contents of this report; that responsibility rests solely with CBO.

Daniel Fried wrote the report. Leigh Angres, Sebastien Gay, Jaeger Nelson, and Joseph Rosenberg provided helpful comments. The economic forecast and related estimates were prepared by Nicholas Abushacra, Grace Berry, Aaron Betz, Daniel Fried, Edward Gamber, Ron Gecan, Mark Lasky, Chandler Lester, Kyoung Mook Lim, Michael McGrane, Christine Ostrowski, Jeffrey Schafer, and Matthew Wilson. Robert Arnold, Richard DeKaser, and Devrim Demirel supervised the preparation of the forecast and the report. Nicholas Abushacra and Grace Berry fact-checked the report.

Mark Doms, Jeffrey Kling, and Robert Sunshine reviewed the report. Caitlin Verboon edited it, and Jorge Salazar prepared it for publication. The report is available on CBO’s website at www.cbo.gov/publication/59837.

CBO seeks feedback to make its work as useful as possible. Please send comments to communications@cbo.gov.

Phillip L. Swagel

Director