At a Glance

Some Members of Congress have proposed introducing a federally administered health insurance plan, or “public option,” to compete with private plans in the nongroup marketplaces established by the Affordable Care Act. In this report, the Congressional Budget Office describes the key design considerations of such a public option and some of their major implications.

Key Design Considerations. Among the key considerations that policymakers designing a public option would face are the following:

- Would the public option conform with state insurance regulations?

- Would it be offered in multiple metal tiers and available outside the marketplaces?

- How would payment rates for providers and prices for prescription drugs be determined?

- Would certain providers be required to participate?

- What administrative activities would the plan take on, and what administrative costs would it incur?

- Would the public option participate in risk-adjustment transfers?

- How would it be funded?

- Would it be offered everywhere or only in geographic markets with low insurer participation or high premiums?

Implications of Design Choices. Policymakers’ choices about design features of the public option would have implications for federal outlays and revenues, health insurance premiums, and health insurance coverage.

- Federal Outlays and Revenues. The budgetary impact of implementing a public option would depend largely on how the option affected the premium of the benchmark plan, which is used to determine marketplace subsidies. A public option with a premium similar to or higher than those of private plans would have little impact, whereas a public option with a relatively low premium would lower the benchmark premium and subsidies.

- Premiums. The public option’s premiums could be higher or lower than those of private nongroup plans, depending mostly on the characteristics of the option: how provider payment rates were determined, the health care utilization of enrollees in the public option compared with that of enrollees in private plans, whether the public option participated in risk-adjustment transfers, and whether the plan’s administrative expenses were more similar to those of Medicare or private insurers.

- Health Insurance Coverage. A public option would affect the total number of people in the United States with health insurance and their sources of coverage by attracting people currently enrolled in the nongroup market, the uninsured population, and people with employment-based coverage. The decrease in the uninsured rate would most likely be largest among those whose income is too high to receive marketplace subsidies. The net effect of implementing a public option on the number of people enrolled in subsidized marketplace coverage would probably be relatively small.

Notes

Notes

As referred to in this report, the Affordable Care Act comprises the Patient Protection and Affordable Care Act (Public Law 111-148), the health care provisions of the Health Care and Education Reconciliation Act of 2010 (P.L. 111-152), and the effects of subsequent judicial decisions, statutory changes, and administrative actions.

Summary

Some Members of Congress have introduced legislative proposals that would make a federally administered health insurance plan—often referred to as a public option—available for purchase with or without federal subsidies in the nongroup marketplaces established under the Affordable Care Act. The insurance risk of the public option would be borne by the federal government—that is, the federal government would bear financial responsibility for medical claims covered by the plan.

In this report, the Congressional Budget Office discusses some of the key design considerations associated with such a program (see Figure S-1). The agency then explains how those design choices would affect the public option’s premiums, private insurers’ premiums and participation in the marketplaces, health insurance coverage in the United States, and federal outlays and revenues. Certain design choices could, for example, result in a public option that used the federal government’s ability to set administered prices and its purchasing power to offer marketplace enrollees a lower-premium plan with a broad provider network; such a plan would most likely encourage a significant number of people to enroll in the public option. Other design choices could be made to establish a public option that was similar to private plans in terms of premiums and provider networks; although such a plan would provide stability to markets in which few private insurers currently participate, it would probably encourage fewer people to enroll in the public option.

This report does not consider policy changes—such as increases in marketplace subsidies—that are often proposed alongside a public option but that are not essential components of such a program.

How Would a Public Option Affect Federal Outlays and Revenues?

Introducing a public option in the nongroup marketplaces could affect the federal budget through three main pathways. First, federal subsidies for insurance purchased through the marketplaces could be reduced. (Those subsidies are determined by the premiums of a benchmark plan—currently, the second-lowest-cost silver plan.)1 Second, the number of people enrolling in marketplace coverage and claiming a subsidy in the form of a premium tax credit could change. Third, the Congress could appropriate funding to cover start-up or ongoing administrative costs.

The budgetary implications of the public option would therefore depend on how the public option affected the benchmark premium and the number of people who signed up for subsidized coverage. Each of those factors, in turn, would depend on private insurers’ participation in the marketplace and on the premiums of private plans and the public option.

How Would a Public Option Affect Premiums?

Depending on the combination of design choices policymakers made, the public option’s premiums could be similar to those of private plans, in which case, the benchmark premium and the total number of people with subsidized marketplace coverage (including enrollees in private plans and enrollees in the public option) would remain about the same. The public option’s premiums would be similar to or higher than private insurers’ premiums if, for example, the plan had the following characteristics: provider payment rates were similar to or higher than rates paid by private plans, prescription drug price negotiation was contracted to a pharmacy benefit manager, and the plan incurred administrative costs similar to those of private plans. In that case, the effects on federal outlays and revenues would be small. The main effect of such a public option would be to add another coverage choice to the private plans in the marketplaces, which could make marketplace coverage more attractive, particularly in markets with few insurers.

Alternatively, the public option’s premiums could be substantially lower than those of private plans. That would be the case if, for example, the plan had the following features: provider payment rates were administered and set at or around Medicare rates, prescription drug prices were set by statute below commercial prices, and the public option was exempt from certain taxes or fees paid by private insurers. Such a public option would enter many markets as the lowest- or second-lowest-cost plan, reducing the benchmark premium and the average federal subsidy. In some markets, the public option could increase the ability of private insurers to negotiate lower rates with providers; those insurers might, in turn, lower their premiums to maintain their market share, which could further reduce the benchmark premium. Such a public option would be more disruptive to nongroup marketplaces than other forms of an option would be. It would probably reduce health care providers’ and prescription drug manufacturers’ revenues. It would probably also cause some private insurers to exit the market entirely, thereby reducing coverage options.

How Would a Public Option Affect Health Insurance Coverage?

A low-premium public option would have the largest effect on the uninsured rate of people who are ineligible for marketplace subsidies because their income is above 400 percent of the federal poverty guidelines (commonly referred to as the federal poverty level).2 Because they must pay the full premium, they are more responsive than people in the subsidy-eligible income range to changes in premiums.

The net effect that a public option would have on the total number of people who received subsidies to purchase coverage through the marketplaces is ambiguous and would probably be small. Decreases in the benchmark premium and subsidy could result in higher net premiums (that is, premiums minus subsidies) for private plans, which might cause some enrollees in those plans to forgo coverage or switch to the public option or to a lower-tier plan. If the public option’s care management was limited and the plan had a broad provider network, it might attract some people who currently forgo marketplace subsidies and purchase a plan outside the marketplace.

A low-premium public option would also attract some people who currently have employment-based coverage: Some of those people would forgo their employer’s offer of insurance, and some employers would choose to no longer offer health insurance. That effect would be small, relative to the total number of people with employment-based coverage, because employers’ and most employees’ premium contributions are excluded from taxable compensation and because people with affordable offers of employment-based coverage are ineligible for marketplace subsidies under current law.

1. Plans in the nongroup marketplaces are classified according to their actuarial value (that is, the percentage of the total costs of covered benefits that the plan will pay for, on average) into bronze, silver, gold, and platinum tiers; bronze plans have the lowest actuarial value and platinum plans the highest. For example, a typical silver plan has an actuarial value of 70 percent, whereas a typical gold plan has an actuarial value of 80 percent. The Affordable Care Act caps the premium contribution as a share of income for enrollees eligible for subsidized coverage. The difference between this premium contribution and the premium of the benchmark plan is subsidized through a premium tax credit, which is typically paid directly to the insurance company on the basis of the enrollee’s estimated income. Although subsidies under the premium tax credit are calculated using the benchmark plan, they can be applied to any plan in the nongroup marketplace.

2. The American Rescue Plan Act of 2021 (Public Law 117-2) extended eligibility for marketplace subsidies to people with income above 400 percent of the federal poverty level (FPL) in 2021 and 2022. (In most states, the FPL in 2021 is $12,880 for a single person and increases by $4,540 for each additional person in a household. Thus, for a single person, 400 percent of the FPL is $51,520 in 2021.) Given the temporary nature of those changes, this report focuses on the marketplace subsidy structure that was in effect before enactment of the American Rescue Plan Act of 2021 and that will be in effect again under current law starting in 2023.

Chapter 1Background

Recently, several proposals to establish a public option—the details of which have varied significantly—have been put forth. This report provides a general framework for evaluating the key design choices in such proposals; it does not analyze any specific bill or proposal.

To establish that general framework, the Congressional Budget Office first defined the scope of the report by identifying characteristics of a public option common to many proposals. The agency then considered several characteristics of the current nongroup health insurance market that have led policymakers to put forth such proposals.1

Scope of the Report

Although various proposals have defined the specifics of a public option differently, CBO focused on a program with the following key characteristics:

- The public option would be offered by the federal government in the health insurance marketplaces established under the Affordable Care Act (ACA) and would, at a minimum, be offered in the metal tier used to determine the federal subsidy.2

- The federal government would bear the insurance risk, but it could contract out claims processing and related administrative functions.3

- The plan would adopt the ACA’s geographic rating areas, and premiums could vary only on the basis of metal tier, rating area, family size, age (by no more than a specified ratio), and tobacco use.4

- The plan would be subject to the same federal eligibility, benefit, and network-adequacy requirements that private nongroup plans are subject to under the ACA.5 In addition, enrollees in the plan would be eligible for income-based premium tax credits and, in the case of plans offered in the silver tier, cost-sharing reductions available under the ACA.

- The premiums for the plan would be set to cover the expected medical expenses of enrollees plus the costs of administration.

Several types of proposals are not considered in this report. For example, proposals to establish a public option often include changes that would substantially increase marketplace subsidies by switching the benchmark plan from silver to gold.6 Although increasing marketplace subsidies or benefits could substantially increase coverage and federal subsidies, neither change is an essential component of a public option; they are therefore outside the scope of this report.7 (For a brief discussion of the temporary increases to marketplace subsidies enacted in the American Rescue Plan Act of 2021, see Box 1-1.)

Box 1-1.

Effects of the American Rescue Plan Act of 2021 on Marketplace Subsidies and a Public Option

The American Rescue Plan Act of 2021 (Public Law 117-2), which was enacted in March 2021, includes provisions that temporarily expand subsidies for health insurance obtained through the marketplaces established under the Affordable Care Act. Those provisions are scheduled to be in effect in 2021 and 2022.1 The enacted legislation increases subsidies for those with income between 100 percent and 400 percent of the federal poverty guidelines (commonly referred to as the federal poverty level, or FPL).2 Those with income up to 150 percent of the FPL pay a zero net premium for the benchmark plan, and those with income between 150 percent and 400 percent of the FPL experience reductions in the share of income they are expected to pay for a benchmark plan. The enacted legislation also extends subsidy eligibility to those with income at or above 400 percent of the FPL so that they do not pay more than 8.5 percent of their income for a benchmark plan. Given the temporary nature of these changes, this report focuses on the marketplace subsidy structure that was in effect before enactment of the American Rescue Plan Act of 2021 and that will be in effect again under current law starting in 2023.

The temporary increases to the marketplace subsidies and expanded eligibility for those subsidies would not significantly change the effect of the public option on federal outlays and revenues, health insurance premiums, or health insurance coverage after those provisions expired. However, in periods when the enhanced subsidies and a public option were both in effect, the impact of the public option on those outcomes would differ in two major ways:

- First, if the entry of the public option into a marketplace lowered the benchmark premium, the federal savings stemming from lower average premium tax credits would be higher because there would be more people enrolled in subsidized coverage as a result of the American Rescue Plan Act of 2021.

- Second, the American Rescue Plan Act of 2021 could lessen the effect of a public option on coverage rates. That is because the expanded eligibility for a marketplace subsidy would prompt people with income above 400 percent of the FPL who would otherwise have been uninsured to enroll in the marketplace plans. A public option would have the largest effect on subsidy-ineligible, uninsured people, and expanding eligibility to those with income above 400 percent of the FPL would decrease the overall size of that group.

1. For more information on how the Congressional Budget Office estimated the effect of these provisions, see Congressional Budget Office, Reconciliation Recommendations of the House Committee on Ways and Means (revised February 17, 2021), www.cbo.gov/publication/57005.

2. In most states, the federal poverty level in 2021 is $12,880 for a single person and increases by $4,540 for each additional person in a household. Thus, for a single person, 400 percent of the FPL is $51,520 in 2021.

Lawmakers have recently proposed legislation that would allow certain people who would not otherwise be eligible for Medicare or Medicaid to purchase coverage through—or “buy in” to—those programs. Such proposals would introduce design considerations and implications that differ from those raised by the type of public option considered in this report.8

In addition, this report does not consider any proposals that would establish a public option at the state level. Some of those proposals more closely resemble regulation of the rates that private insurers pay providers than they do a public option as defined here.9 Nor does this report consider proposals that would have the federal government contract with private insurers to bear the insurance risk.

Also outside the scope of this report, which focuses on the nongroup market, is a public option that employers could offer their employees. A public option available in the large-group or small-group markets would introduce its own set of design considerations and implementation challenges and would have significantly different budgetary consequences. (For a brief overview of those issues, see Box 1-2.)

Box 1-2.

Creating a Public Option That Could Be Offered by Employers

In addition to establishing a federally administered public health insurance plan that would be offered in the nongroup market—often referred to as a public option—policymakers could make such a plan available to employers so that they could offer it to their employees.1 Most people obtain health insurance coverage through their or a family member’s employer, so a public option that employers could offer their employees could have a much greater impact on sources of coverage and federal subsidies for health insurance than one limited to the nongroup market.

Implementing a public option that could be offered by employers would be more complex than implementing one that was available only in the nongroup market. Specifically, allowing the public option to be offered through employers would change the set of design choices, the nature of the implementation challenges, and the magnitude of the effects on federal costs and on health insurance coverage. A detailed analysis of those questions is outside the scope of this report.

In general, an employment-based public option could be made available in any of the following forms:

- A fully insured plan in the small-group market. Small employers could offer the plan, and the federal government would bear the insurance risk. In most states, employers with 50 or fewer employees qualify as small under the Affordable Care Act and are thus eligible to purchase small-group coverage.2

- A fully insured plan in the large-group market. Large employers could offer the plan, and the federal government would bear the insurance risk.

- A self-insured plan. Employers who offered the plan would bear the insurance risk, and the federal government would provide administrative services, such as forming provider networks and setting or negotiating payment rates. Under the Employee Retirement Income Security Act, self-insured plans are not subject to state regulations, and many of the federal regulations that apply to fully insured plans in the large-group market do not apply to self-insured plans.

Design Considerations and Implementation Challenges

Under current law, the small-group and nongroup markets are subject to many of the same regulations, which would make offering the public option in the small-group market simpler than offering it in the large-group market. In most cases, small-group premiums can vary only by rating area, family size, age (by no more than a specified ratio), and tobacco use; most private insurers in the small-group market participate in a single risk pool and make risk-adjustment transfers; and small-group insurers are subject to the same essential health benefit requirements as nongroup insurers.

Policymakers could decide to vary the public option’s premiums by market segment (small group or nongroup). If both the public option and private insurers participated in the risk-adjustment system—which transfers funds among insurers on the basis of the relative health of their enrollees—it would be more challenging to set the same premiums in both the small-group and nongroup markets because the premiums would need to account for anticipated risk-adjustment transfers in two separate markets.

Under current law, premiums for fully insured large-group plans can be experience rated, and large-group insurers do not participate in a federal risk-adjustment program.3 If the public option was available in the large-group market and its premiums were experience rated, a premium-setting mechanism would have to be developed. If, instead, the public option’s premiums were set using the nongroup market’s rating rules, large firms with healthier employees would tend to prefer to self-insure or offer experience-rated private plans, and firms with sicker employees would tend to prefer the public option. If low administrative costs, provider payment rates, and prescription drug prices kept its premiums low, a public option might still attract firms with healthier employees.

Most employees in large firms have health coverage that is self-insured by their employer through an administrative services only (ASO) arrangement—that is, the employer pays for their enrollees’ medical claims and contracts with a third party to form provider networks, negotiate payment rates, and process claims.4 If the public option was available as an ASO, the government would provide administrative services but would not need a premium-setting mechanism.

Implications for Enrollment and Federal Spending

A public option that was available in the nongroup market and through employers could have much higher enrollment than a nongroup-only public option for several reasons. The number of workers and dependents enrolled in employment-based plans is roughly 10 times the size of the population in the nongroup market.5 Additionally, employers and employees might be more responsive to the lower premiums that a public option might offer than people in the nongroup market, who are insulated from premiums by the structure of subsidies. The availability of a public option could have a pronounced effect in the small-group market, because the decision of small employers to offer health insurance is more sensitive to premiums than that of large employers.6

The Congressional Budget Office expects that if the public option was offered by employers in the group market at premiums below current private premiums, employers would increase wages, which would increase taxable compensation and, in turn, federal tax revenues. Any costs of administering the program that were not covered by premium collections would, as long as appropriated funds were available, increase federal outlays.

If employers offered the public option and it paid providers lower rates than private insurers paid, the public option’s impact on health care providers’ revenues would also be greater than if the public option was available only in the nongroup market. Consequently, providers would be more likely to opt out of Medicaid and Medicare if participation in the public option was tied to those programs. The potential for spillover effects on the rates that private insurers negotiated with providers and the broader impact on private insurers would also be larger.

1. The nongroup market refers to the private market in which individuals and families purchase health insurance directly from an insurer, rather than obtaining it through an employer. Several legislative proposals would create a public option that would be available to employers. For example, the Choose Medicare Act (H.R. 2463 and S. 1261, 116th Cong.) and the Medicare-X Choice Act (H.R. 2000 and S. 981, 116th Cong.) would create a federal public option that would be offered to small employers through the Small Business Health Options Program marketplaces established by the Affordable Care Act. The Medicare-X Choice Act specifies that the public option would be made available in the small-group market only after it was offered in the nongroup market. The Choose Medicare Act would make a federal public option available in the large-group market and would allow the Centers for Medicare & Medicaid Services to act as a third-party administrator for self-insured employers.

2. See Centers for Medicare & Medicaid Services, “Market Rating Reforms” (updated June 2, 2017), https://go.usa.gov/x74Ft.

3. Experience rating refers to a method of setting premiums that predicts a group’s future health care costs on the basis of its past experience, such as the actual cost of providing health care coverage to the group during a given period of time. For an overview of which Affordable Care Act provisions apply to fully insured large group plans, see Annie L. Mach and Bernadette Fernandez, Private Health Insurance Market Reforms in the Patient Protection and Affordable Care Act (ACA), Report R42069 (Congressional Research Service, February 2016).

4. See Kaiser Family Foundation, 2018 Employer Health Benefits Survey (October 2018), https://tinyurl.com/ybqx9xnl.

5. In CBO’s baseline projections, 151 million people have employment-based coverage in 2021, and 14 million people have nongroup coverage. For more information, see Congressional Budget Office, Federal Subsidies for Health Insurance Coverage for People Under 65: 2020 to 2030 (September 2020), www.cbo.gov/publication/56571.

6. See Jonathan Gruber and Michael Lettau, “How Elastic Is the Firm’s Demand for Health Insurance?” Journal of Public Economics, vol. 88, nos. 7–8 (July 2004), pp. 1273–1293, https://doi.org/10.1016/S0047-2727(02)00191-3.

Characteristics of the Current Nongroup Health Insurance Market

Several characteristics of the nongroup health insurance market have led policymakers to consider establishing a nongroup public option. Those characteristics include volatility in insurers’ participation, a lack of competition, narrow provider networks, and provider payment rates and administrative costs that are often higher than those of publicly administered programs such as Medicare and Medicaid. A public option might mitigate those concerns to some extent, depending on how it was designed.

Volatility in Insurers’ Participation and Lack of Competition

The number of insurers in the nongroup marketplaces has fluctuated over time as various insurers have entered and exited. In 2021, an average of 5.0 insurers are participating in at least one of the marketplaces in each state, up from 3.5 in 2018 but down from 6.0 in 2015.10 Volatility in insurers’ participation in the marketplaces or in their plan offerings may force enrollees to involuntarily switch plans, which is one form of a phenomenon called insurance churning. That volatility undermines the attractiveness of marketplace plans and may dissuade some people from signing up for coverage.11

In addition to that volatility, the marketplaces in some geographic areas have only a few insurers participating in them. Although participation by insurers has increased in recent years, 22 percent of enrollees live in a county with only one or two insurers in 2021 (see Figure 1-1). Low insurer participation in the marketplaces limits enrollees’ choice of a plan and lessens competition among insurers, thereby contributing to higher premiums. CBO found a negative association between the number of insurers in a marketplace and the premiums for the second-lowest-cost silver plan in a marketplace, which is consistent with academic research (see Figure 1-2).12 In markets with four or more insurers, the average monthly premium for the second-lowest-cost silver plan is about $330 in 2021, whereas in markets with only one insurer, the average monthly premium is about $480.

Figure 1-1.

Number of Insurers That People Enrolling in Coverage Through the Marketplaces Were Able to Choose From

Some of the nongroup health insurance marketplaces established by the Affordable Care Act are more competitive than others. The number of insurers participating in each of the more than 500 geographic rating areas across the country has ranged from 1 to 10 or more since 2017.

Data source: Congressional Budget Office, using data from Daniel McDermott and Cynthia Cox, Insurer Participation on the ACA Marketplaces, 2014–2021 (Kaiser Family Foundation, November 2020), https://tinyurl.com/y37ugsc8. See www.cbo.gov/publication/57020#data.

a. Percentage of all people enrolled in a marketplace plan in a given year. For 2021, values are based on the number of people who signed up for a plan for the year in 2020. CBO modified the rounded percentages reported in the Kaiser Family Foundation report so that they would sum to 100 percent.

Figure 1-2.

Average Monthly Premiums of Benchmark Plans in 2021, by the Number of Insurers Participating in the Marketplace

Dollars

The benchmark plan’s premiums tend to be lower in geographic areas with more insurers, which accords with academic research suggesting that greater competition among insurers contributes to lower premiums.

Data source: Congressional Budget Office, using data from the Robert Wood Johnson Foundation’s HIX Compare database. See www.cbo.gov/publication/57020#data.

Plans in the nongroup health insurance marketplaces established by the Affordable Care Act are classified according to their level of cost sharing into tiers named after precious metals. Under current law, the benchmark plan for a marketplace is the second-lowest-cost silver plan in that marketplace.

Narrow Provider Networks

In 2017, 21 percent of plans in the marketplaces had physician networks that included less than a quarter of eligible physicians in the plan’s area, and 41 percent of plans’ networks included less than 40 percent of eligible physicians.13 Narrow hospital networks were also prevalent—29 percent of individuals eligible for marketplace plans had access only to a plan whose network included less than 70 percent of eligible hospitals.14 Only 5 percent of firms offering health benefits to their employees reported that they offered one or more plans that they considered to have a narrow network.15

After controlling for other factors, some researchers have found evidence to suggest that marketplace plans with narrow provider networks tend to have lower premiums.16 Several possible explanations for that finding exist. Plans with narrow networks may achieve savings by excluding high-priced or inefficient providers. Another possibility is that plans with narrow networks may be able to negotiate lower prices with providers in exchange for bringing a greater number of patients to those providers. In addition, the threat of exclusion from the network could induce providers to become more efficient and decrease unnecessary spending. Also, longer travel times to receive care and greater difficulty scheduling appointments might dissuade enrollees in plans with a limited set of in-network providers from seeking some care.

Although narrow networks may result in lower premiums, they may also limit enrollees’ access to care, especially in areas with a limited number of geographically accessible providers. One study of marketplace enrollees in California found that plans with narrow networks exacerbated the problem of limited access to providers for enrollees in rural areas.17 Moreover, plans with narrow networks often have limited coverage of out-of-network care, which can leave patients exposed to high medical bills.18

Higher Provider Payment Rates Than Those Paid by Public Programs

CBO estimates that in 2020, the rates paid to providers by insurers in the broader commercial market (which includes employment-based plans and nongroup plans) were roughly twice as high as Medicare’s rates for hospitals and 25 percent higher than the program’s rates for physicians.19 The net prices paid by commercial insurers for prescription drugs are, the agency estimates, somewhat higher than the net prices paid in Medicare Part D.20 Moreover, CBO projects that provider payment rates in the commercial market will grow faster than Medicare’s rates over the next decade, which would further widen the gap between commercial and Medicare rates over time.21

CBO does not know of research estimating provider payment rates in the nongroup market for a broad range of services, but the agency expects that they fall between Medicare’s rates and broader commercial rates, on average.22 Two factors suggest that payment rates in the nongroup market are lower than the rates in the broader commercial market and that they could be lower than Medicare’s rates in some markets: Nongroup plans generally have narrower provider networks than employment-based plans; and a significant number of Medicaid managed care organizations, which typically have narrow provider networks, participate in the nongroup marketplaces. Payment rates are lower, on average, in narrow network plans.23 Likewise, insurers participating in Medicaid managed care tend to pay providers lower rates than employment-based plans, and they may pay lower rates than other marketplace plans, too.24 One study reports that average spending is lower in the nongroup market than in the employment-based group market even though enrollees in the nongroup market have higher risk scores, on average.25 That discrepancy suggests that provider payment rates of plans in the nongroup market may be lower than those of employment-based group plans, though nongroup plans’ more stringent care management and the fact that they generally require enrollees to pay a larger share of costs than employment-based plans may also contribute to the difference in average spending.

Higher Administrative Costs Than Those of Other Payers

Administrative costs in the nongroup market accounted for an average of 17 percent of total premiums from 2015 to 2018.26 That administrative cost share is higher than in most other market segments, partly because, on average, nongroup insurers have fewer enrollees—and thus less revenue from premiums—yet many administrative costs are fixed (that is, they do not vary with the number of enrollees). By comparison, CBO estimates that in 2020, administrative costs accounted for 8 percent of total spending for Medicaid, 2 percent of Medicare’s fee-for-service (FFS) program spending, 7 percent of all spending for Medicare (including spending for FFS, Medicare Advantage, and Part D), and 12 percent of private plans’ spending, on average. Such expenses include the cost of claims processing and appeals, quality improvement, advertising, fraud reduction programs, educational activities for beneficiaries, certification of providers, general information technology, accounting costs, taxes, salaries and broker compensation, and (for private insurers) profits and losses.

1. The nongroup health insurance market is the private market in which individuals and families purchase health insurance directly from an insurer, rather than obtaining it through an employer.

2. Under current law, the second-lowest-cost silver plan is the benchmark plan that determines the amount of premium tax credits in a marketplace. A public option offered in the silver tier would be considered in the determination of the benchmark plan and the premium tax credit.

3. Several legislative proposals, including the Keeping Health Insurance Affordable Act of 2019 (S. 3, 116th Cong.), the CHOICE Act (H.R. 2085 and S. 1033, 116th Cong.), and the Public Option Deficit Reduction Act (H.R. 1419, 116th Cong.), specify that the public option would not transfer insurance risk to private insurers. The Medicare-X Choice Act (H.R. 2000 and S. 981, 116th Cong.) specifies that the public option would not transfer insurance risk, except under alternative payment models. Those proposals also would allow the public option to contract out administrative functions. Contractors could play a role similar to that of the administrative contractors for Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) authorized under section 1874A of the Social Security Act (codified at 42 U.S.C. §1395kk-1 (2018)).

4. See Centers for Medicare & Medicaid Services, “Market Rating Reforms” (updated June 2, 2017), https://go.usa.gov/x74Ft.

5. Under the ACA, plans in the marketplace must, among other things, cover 10 essential health benefits, have no annual or lifetime caps on such benefits, be made available to people with preexisting conditions, and offer specified actuarial values. For more information, see Annie L. Mach and Namrata K. Uberoi, Overview of Private Health Insurance Provisions in the Patient Protection and Affordable Care Act (ACA), Report R43854, version 9 (Congressional Research Service, April 5, 2016), https://go.usa.gov/x72xu.

6. For example, the Choose Medicare Act (H.R. 2463 and S. 1261, 116th Cong.) would change the benchmark plan from silver to gold (that is, from a plan with an actuarial value of 70 percent to one with a value of 80 percent). Both the Choose Medicare Act and the Keeping Health Insurance Affordable Act of 2019 (S. 3, 116th Cong.) would extend eligibility for premium tax credits to people with income of up to 600 percent of the federal poverty level.

7. For example, the Patient Protection and Affordable Care Enhancement Act (H.R. 1425, 116th Cong.) would increase marketplace subsidies without introducing a public option. See Congressional Budget Office, cost estimate for Rules Committee Print 116-56, Patient Protection and Affordable Care Enhancement Act (June 24, 2020), www.cbo.gov/publication/56434.

8. For more information, see Kaiser Family Foundation, “Compare Medicare-for-All and Public Plan Proposals” (May 15, 2019), https://tinyurl.com/rweag65. For examples of Medicare buy-in legislation, see the Expanding Health Care Options for Early Retirees Act (H.R. 4527 and S. 2552, 116th Cong.), the Medicare Buy-In and Health Care Stabilization Act of 2019 (H.R. 1346, 116th Cong.), and the Medicare at 50 Act (S. 470, 116th Cong.). For an example of Medicaid buy-in legislation, see the State Public Option Act (H.R. 1277 and S. 489, 116th Cong.).

9. For instance, Washington State introduced a version of a public option administered by private insurers for the 2021 plan year that caps aggregate payment rates at a specified multiplier of Medicare fee-for-service payment rates. For more information, see James C. Capretta, “Washington State’s Quasi-Public Option,” The Milbank Quarterly, vol. 98 (March 2020), https://tinyurl.com/y4omu2uo.

10. See Daniel McDermott and Cynthia Cox, Insurer Participation on the ACA Marketplaces, 2014–2021 (Kaiser Family Foundation, November 23, 2020), https://tinyurl.com/ydc6wlpb.

11. Churning, even when it does not result in gaps in coverage, has been associated with worsening quality of care in self-report surveys. For more information, see Benjamin D. Sommers and others, “Insurance Churning Rates for Low-Income Adults Under Health Reform: Lower Than Expected but Still Harmful for Many,” Health Affairs, vol. 35, no. 10 (October 2016), pp. 1816–1824, http://doi.org/10.1377/hlthaff.2016.0455.

12. Researchers have estimated that the population-weighted average premium for the second-lowest-cost silver plan would have been reduced by 5.4 percent in 2014 if United Healthcare had entered all federally facilitated marketplaces and enrolled an average of 16 percent of enrollees in each market. The average benchmark premium would have been 11.1 percent lower if all insurers that sold individual coverage in a state had also sold nongroup marketplace coverage in each of that state’s rating areas. For more information, see Leemore Dafny, Jonathan Gruber, and Christopher Ody, “More Insurers Lower Premiums: Evidence From Initial Pricing in the Health Insurance Marketplaces,” American Journal of Health Economics, vol. 1, no. 1 (Winter 2015). pp.53–81, http://doi.org/10.1162/ajhe_a_00003. For further evidence on the relationship between premiums and insurers’ participation in the marketplaces, see Linda J. Blumberg and others, Is There Potential for Public Plans to Reduce Premiums of Competing Insurers? (Urban Institute, October 2019), https://tinyurl.com/yyhk55og.

13. See Daniel Polsky, Janet Weiner, and Yuehan Zhang, Exploring the Decline of Narrow Networks on the ACA Marketplaces in 2017, LDI Issue Brief, vol. 21, no. 9 (Leonard Davis Institute of Health Economics, November 2017), https://tinyurl.com/y5gjgwqm.

14. See Erica Hutchins Coe, Jessica Lamb, and Suzanne Rivera, Hospital Networks: Perspective From Four Years of the Individual Market Exchanges (McKinsey Center for U.S. Health System Reform, May 2017), https://tinyurl.com/y3u3gjr6. If a network was tiered, the authors included only the hospitals in the lowest cost-sharing tier in their analysis.

15. See Kaiser Family Foundation, 2019 Employer Health Benefits Survey (September 25, 2019), Section 14, https://tinyurl.com/y47uagba.

16. See Leemore S. Dafny and others, “Narrow Networks on the Health Insurance Marketplaces: Prevalence, Pricing, and the Cost of Network Breadth,” Health Affairs, vol. 36, no. 9 (September 2017), pp. 1606–1614, https://doi.org/10.1377/hlthaff.2016.1669.

17. See Simon F. Haeder, David Weimer, and Dana B. Mukamel, “A Consumer-Centric Approach to Network Adequacy: Access to Four Specialties in California’s Marketplace,” Health Affairs, vol. 38, no. 11 (November 2019), pp. 1918–1926, https://doi.org/10.1377/hlthaff.2019.00116.

18. See Kathy Hempstead, “Marketplace Pulse: Percent of Plans With Out-of-Network Benefits” (Robert Wood Johnson Foundation, October 4, 2018), https://tinyurl.com/y5ryko74.

19. For more information, see CBO’s Single-Payer Health Care Systems Team, How CBO Analyzes the Costs of Proposals for Single-Payer Health Care Systems That Are Based on Medicare’s Fee-for-Service Program, Working Paper 2020-08 (Congressional Budget Office, December 2020), Section 4, www.cbo.gov/publication/56811; Daria M. Pelech, “Prices for Physicians’ Services in Medicare Advantage and Commercial Plans,” Medical Care Research and Review, vol. 77, no. 3 (June 2020), pp. 236–248, https://doi.org/10.1177/1077558718780604; Eric Lopez and others, How Much More Than Medicare Do Private Insurers Pay? A Review of the Literature (Kaiser Family Foundation, April 2020), https://tinyurl.com/y6yyb83z; and Jared Lane K. Maeda and Lyle Nelson, “How Do the Hospital Prices Paid by Medicare Advantage Plans and Commercial Plans Compare With Medicare Fee-for-Service Prices?” INQUIRY: The Journal of Health Care Organization, Provision, and Financing, vol. 55 (June 2018), pp. 1–8, https://doi.org/10.1177/0046958018779654.

20. Net prices are the total prices paid at pharmacies minus rebates from manufacturers and other discounts. The net prices that Medicare Part D pays for outpatient prescription drugs are closer to the prices paid by commercial plans than are the program’s prices for hospital and physicians’ services because Medicare uses tools similar to those used by commercial plans to determine prices for outpatient prescription drugs. CBO expects that Medicare’s net prices for outpatient prescription drugs are somewhat lower than those paid by private plans: Manufacturers are required to offer the highest rebate that they offer to any payer, excluding certain government programs, such as Medicare Part D; manufacturers may therefore be less willing to offer steep discounts to commercial plans than to Medicare Part D plans. For more information, see Congressional Budget Office, A Comparison of Brand-Name Drug Prices Among Selected Federal Programs (February 2021), www.cbo.gov/publication/56978.

21. In CBO’s projections for 2020 to 2030, Medicare’s payment rates grow by 2.3 percent per year for hospitals and by 0.3 percent per year for physicians, while commercial payment rates increase by 4.2 percent per year for hospitals and by 2.9 percent per year for physicians. For more information, see CBO’s Single-Payer Health Care Systems Team, How CBO Analyzes the Costs of Proposals for Single-Payer Health Care Systems That Are Based on Medicare’s Fee-for-Service Program, Working Paper 2020-08 (Congressional Budget Office, December 2020), Section 4, www.cbo.gov/publication/56811.

22. Recent studies have compared rates paid by nongroup plans with rates paid by employment-based plans and public programs, but they have done so only for a narrow set of physicians’ services or by using data from the first years of the marketplaces. See Adam I. Biener and Thomas M. Selden, “Public and Private Payments for Physician Office Visits,” Health Affairs, vol. 36, no. 12 (December 2017), pp. 2160–2164, https://doi.org/10.1377/hlthaff.2017.0749; and Heidi Allen and others, “Comparison of Utilization, Costs, and Quality of Medicaid vs Subsidized Private Health Insurance for Low-Income Adults,” JAMA Network Open, vol. 4, no. 1 (January 2021), e2032669, https://doi.org/10.1001/jamanetworkopen.2020.32669.

23. See John A. Graves and others, “Breadth and Exclusivity of Hospital and Physician Networks in U.S. Insurance Markets,” JAMA Network Open, vol. 3, no.12 (December 2020), e2029419, http://doi.org/10.1001/jamanetworkopen.2020.29419; Leemore S. Dafny and others, “Narrow Networks on the Health Insurance Marketplaces: Prevalence, Pricing, and the Cost of Network Breadth,” Health Affairs, vol. 36, no. 9 (September 2017), pp. 1606–1614, https://doi.org/10.1377/hlthaff.2016.1669; and Jonathan Gruber and Robin McKnight, “Controlling Health Care Costs Through Limited Network Insurance Plans: Evidence From Massachusetts State Employees,” American Economic Journal: Economic Policy, vol. 8, no. 2 (May 2016), pp. 219–250, https://doi.org/10.1257/pol.20140335.

24. See Erik Wengle and others, Effects of Medicaid Health Plan Dominance in Health Insurance Marketplaces (Urban Institute, June 2020), https://tinyurl.com/yy6wzthy; and Katherine Hempstead, “Marketplace Pulse: Medicaid Managed Care Organizations in the Individual Market” (Robert Wood Johnson Foundation, May 20, 2019), https://tinyurl.com/yxsnz5ty.

25. See Brett Lissenden and others, “A Comparison of Health Risk and Costs Across Private Insurance Markets,” Medical Care, vol. 58, no. 2 (February 2020), pp. 146–153, https://doi.org/10.1097/MLR.0000000000001239.

26. See CBO’s Single-Payer Health Care Systems Team, How CBO Analyzes the Costs of Proposals for Single-Payer Health Care Systems That Are Based on Medicare’s Fee-for-Service Program, Working Paper 2020-08 (Congressional Budget Office, December 2020), Box 14-1, www.cbo.gov/publication/56811.

Chapter 2Key Design Considerations

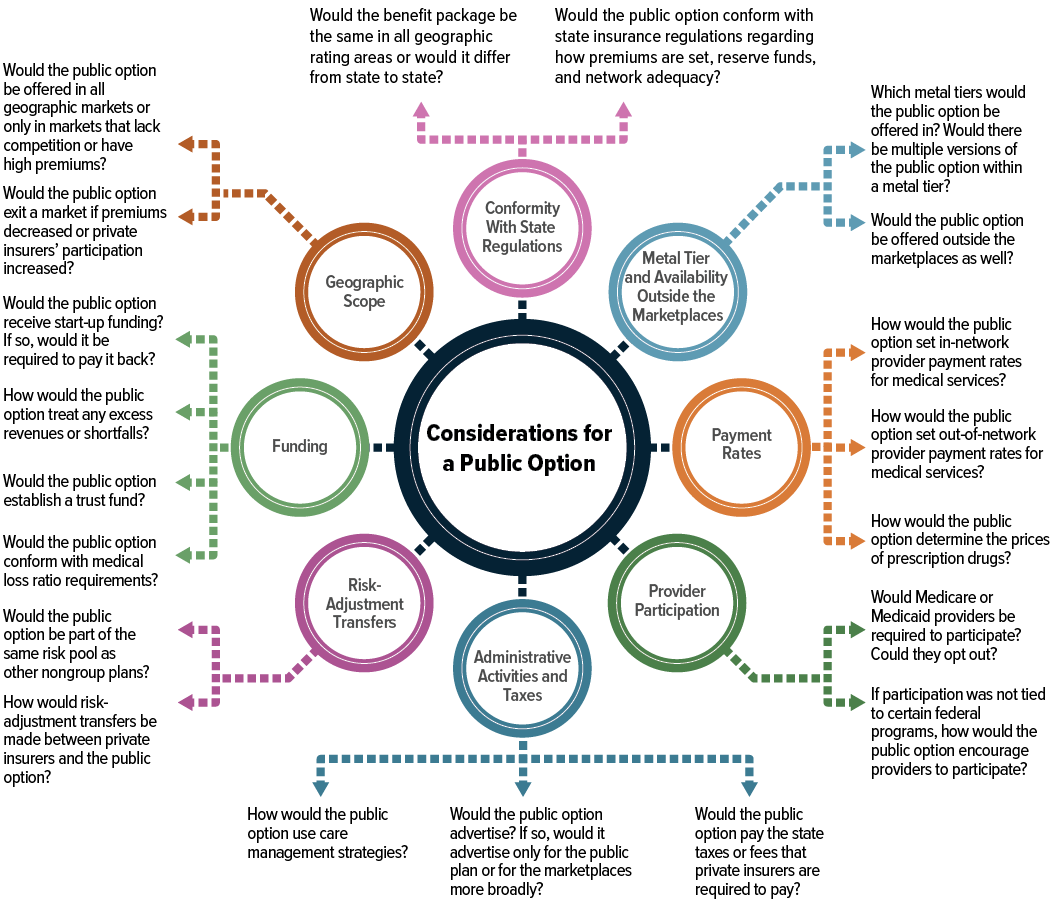

This report focuses on the following key design considerations that policymakers will face as they develop proposals that would create a public option:

- Would the public option conform with state insurance regulations pertaining to benefit packages, how premiums are set, reserve funds, and network adequacy?

- Would the public option be offered in multiple metal tiers, and would it be available outside the marketplaces?

- How would provider payment rates for medical services and the prices of prescription drugs be determined?

- Would Medicare or Medicaid providers be required to participate in the public option?

- How would the public option’s administrative activities and administrative costs compare with those of private insurers?

- Would the public option participate in the risk-adjustment system, which transfers funds among insurers on the basis of the relative health of their enrollees?

- How would the public option be funded? How would excess premiums or shortfalls be handled?

- Would the public option be offered everywhere or only in geographic areas with low insurer participation or high premiums?

Conformity With State Regulations

An important question for policymakers is whether, or to what extent, the public option would conform with state insurance regulations. Because it would be administered by a federal entity, the public option would not necessarily be subject to those regulations, but the Congress could nevertheless specify that the public option conform with them. For example, each state sets its own requirements for coverage of specific services for nongroup insurers in the marketplaces, resulting in variation among states in the services that insurers must cover.1 The public option could offer a single national benefit package that covered all services that were mandated by any state. In that case, the public option’s benefit package would be more generous than private plans in some states. If, instead, the public option was designed to provide a single national benefit package that did not conform with all state regulations, it could be less generous than private plans in some states. A third option would be to design a public option benefit package that matched each state’s set of required benefits. Such a plan would align more closely with existing private plans, but it would be more complex to administer.

In addition to benefit-package requirements, private insurers are subject to other state regulations and to a review of their premiums. Some states allow less variation in premiums by age than the federal government permits.2 If the public option’s premiums were set using the Affordable Care Act’s broader age requirements and did not conform with state requirements, the public option in such states would be more attractive to younger enrollees, who are healthier, on average. Also, determining the benchmark plan and premium tax credit would pose significant implementation challenges if the public option did not adhere to state premium-setting rules. Policymakers would also need to decide whether the public option would voluntarily conform with rules, which vary from state to state, regarding the amount of reserve funds that private insurers are required to hold to prevent insolvency. Furthermore, states use a variety of qualitative and quantitative standards to measure network adequacy. Policymakers could decide whether state regulators would need to approve the network adequacy of the public option or if the public option would have its own standards. If the public option had its own standards, private insurers could be subject to stricter standards than the public option in some states and looser standards in others.

Metal Tiers and Availability Outside the Marketplaces

The public option could be offered in all the metal tiers of marketplace insurance plans (bronze, silver, gold, and platinum) or in only a subset; for this analysis, the Congressional Budget Office assumed that the public option would always be offered in the metal tier of the benchmark plan.3 Moreover, multiple public plans could be offered within a metal tier or just a single plan. If multiple plans were offered in a tier, they might have varying combinations of cost sharing and deductibles and provide different benefits, such as coverage of dental and vision care.

Additionally, the public option could be offered exclusively in the marketplaces, or it could also be available for purchase outside the marketplaces, which would require a separate enrollment platform.4 An off-marketplace nongroup public option could be more attractive to certain segments of the population than one offered in the marketplaces. For example, premiums of off-marketplace silver plans are often lower than those of marketplace silver plans because in many cases private insurers cover the costs of cost-sharing reductions—that is, discounts that reduce the out-of-pocket expenses of qualifying individuals—by increasing premiums for silver plans offered through the marketplaces.5 If the costs of cost-sharing reductions for the public option were also covered through the premium of the marketplace silver plan, the premium of a silver plan outside the marketplace could be lower than that of a marketplace silver plan, making the off-marketplace public option more attractive to unsubsidized enrollees. Additionally, an off-marketplace public option would be more attractive to employees with an individual coverage health reimbursement arrangement—a tax-advantaged account that employers can offer to employees for the purchase of a nongroup plan. Employees can use their contributions to such an account, which reduce their taxable income, to purchase off-marketplace coverage; that tax benefit is not available for the purchase of marketplace coverage.6

In-Network Provider Payment Rates for Medical Services

One key factor influencing a health plan’s premiums is the payment rates paid to providers for covered services. There are two broad approaches to determining in-network provider payment rates that the federal government could consider—administering rates or negotiating them.

Administered Rates

The federal government could specify formula-driven payment rates in law or regulation. It could use the Medicare fee-for-service rates, a multiplier of Medicare rates, or a new fee schedule.7 A multiplier could be an across-the-board increase to Medicare rates—120 percent or 150 percent of the Medicare FFS rate schedule, for example—or policymakers could make targeted increases to Medicare rates.8 Medicare already has payment policies in place to preserve access to rural health care, but the public option could apply further increases—say, 125 percent of the Medicare FFS rate schedule—in rural areas.9 Basing payment rates on Medicare rates would leverage the existing infrastructure for setting Medicare payments and thereby decrease administrative costs for the public option. That approach would also incorporate geographic variation in payment rates, though the geographic variation in commercial prices is much greater than the variation in Medicare payment rates.10 If the federal government developed a new fee schedule, it could be based on average or median commercial rates. Such an approach would be more administratively complex than using the existing Medicare FFS rate schedule because it would require the development of a system for collecting and processing commercial claims data.

Negotiated Rates

The federal government could negotiate with health care providers to determine payment rates, as commercial insurers currently do. In general, the outcomes of negotiations over payment rates reflect the negotiating leverage of insurers and providers. Insurers with larger market shares are typically able to negotiate lower payment rates, and hospitals and physician groups with large market shares are typically able to negotiate higher payment rates.11 Providers might also accept lower rates to participate in a narrower network. The federal government would need to develop an approach to conducting those negotiations; it could either negotiate directly with thousands of health care providers or contract with an outside party to conduct negotiations.

Although negotiated payment rates would not be set in statute, policymakers could impose certain constraints on the negotiations, such as upper or lower limits on the rates. Such limits on the public option’s negotiated rates could be based on Medicare rates or on commercial rates.12 Those limits could be specified for particular procedures or services, or they could be based on an aggregate measure and apply to all services. A provider who did not accept the public option’s final payment rate offer would be out of the public option’s network. Regardless of the specific approach chosen, negotiating rates would be more administratively complex than adopting a formula-driven approach to rate setting and would involve additional expenses.

Implementation Challenges

If the public option’s payment rates were negotiated, the negotiations would be administratively complex and difficult to implement. The federal government could choose to negotiate directly with thousands of health care providers, but policymakers would need to develop a new infrastructure and system for conducting the negotiations. Alternatively, the federal government could choose to contract with one or more third parties to negotiate with providers; but without transferring insurance risk, aligning contractors’ incentives to negotiate lower rates with the government’s incentives could be difficult. In addition, the government would incur significant expenses to hire contractors for such purposes. Moreover, priorities could shift from one Administration to the next—a situation that would lead to greater uncertainty in payment rates over time. For example, one Administration might prioritize negotiating low payment rates, whereas another might prioritize attracting providers and thus agree to higher rates.

If the public option’s payment rates, whether administered or negotiated, were tied to commercial rates, several implementation challenges would arise. First, using commercial rates to determine the public option’s rates would create additional administrative complexities and costs, and policymakers would have to determine which commercial rates to include, which sources of data to use, and how frequently to update the data. Tying the public option’s payment rates to those in the fully insured group market and self-insured market would most likely result in higher rates than tying them only to the nongroup market’s rates.

Similarly, policymakers would need to decide whether the relevant commercial price was an average among all geographic areas or specific to each rating area. If the commercial price of all markets was averaged and that average price was the upper bound in rate negotiations, the government would face difficult coordination challenges when negotiating with multiple hospital and provider systems in multiple markets. If, instead, the commercial price was measured in each rating area separately, some of those implementation challenges would be mitigated, but more-detailed data on private payment rates would be required.

Finally, basing the public option’s payment rates on commercial rates could affect providers’ negotiations with private insurers. In some cases, providers might be less willing to give price concessions to private insurers because those concessions would not only lower private payments but also decrease the price used to determine public option rates.

Paying providers at or around Medicare rates for enrollees in the public option could negatively affect the revenues of some providers. However, because the nongroup market accounts for a relatively small share of total enrollment in the broader commercial market, the effect on providers’ revenues would be limited.

Out-of-Network Benefits and Payment Rates for Out-of-Network Providers

Another important design consideration for the public option is whether out-of-network care would be covered and, if so, under what circumstances. At one extreme, the public option could operate like a health maintenance organization (HMO) and not cover any out-of-network care beyond emergency services, which are required to be covered without prior authorization under the Affordable Care Act and the Consolidated Appropriations Act, 2021 (Public Law 116-260).13 An HMO-style benefit would reduce the public option’s claims costs but would require enrollees to pay for most or all of their care if they elected to receive nonemergency out-of-network services, particularly if the provider network was narrow. At the other extreme, the public option could cover all out-of-network care with no additional cost sharing for patients. That approach would provide more comprehensive protection for enrollees, but it would also increase the public option’s claims costs and limit the plan’s ability to steer enrollees toward higher quality or more cost-effective providers. Another approach would be for the public option to cover out-of-network care but require enrollees to pay a larger share of the cost for that care. In many plans currently offered in the marketplaces, enrollees face very high cost sharing for out-of-network care.14 If out-of-network care was covered under the public option, it would also be important to determine whether providers would be allowed to bill patients for amounts beyond their required copayments and coinsurance.15

How the out-of-network payment standard would influence in-network payment rates for the public option would depend on several factors: the extent to which the public option covered out-of-network care, patients’ share of the cost for such care (including whether patients were required to pay any costs in addition to their required copayments and coinsurance), and providers’ ability to turn away out-of-network patients. Those factors would affect the attractiveness to providers of staying out of network versus accepting in-network payment rates. However, the specific effects of out-of-network standards on in-network rates would depend on how payment rates were set and the degree of leverage providers had in securing higher in-network rates.

Pricing of Prescription Drugs

In addition to deciding how the prices of medical services would be set, policymakers would need to specify an approach to determining prices for prescription drugs under the public option. The prices paid for prescription drugs vary widely among health plans and federal programs, and they depend, in part, on the approach policymakers adopt.16 Policymakers could consider several different strategies, including authorizing the Secretary of Health and Human Services (HHS) to negotiate drug prices with manufacturers, contracting with a private pharmacy benefit manager (PBM) to negotiate prices, or setting prices in law or regulation.17

Authorize the Secretary of Health and Human Services to Negotiate Prices

The effectiveness of authorizing the HHS Secretary to negotiate drug prices, as several recent legislative proposals would do, would depend on the degree of leverage granted to the Secretary, which could vary substantially, and on the extent to which the Secretary exercised that leverage.18 The Secretary’s bargaining position could be enhanced by using tools such as a tiered formulary (a list with drugs divided into different tiers that require beneficiaries to pay varying amounts) and the ability to exclude one or more drugs in a therapeutic class (a group of drugs that treat a common condition) or to require preauthorization for their use. The ability to require preauthorization for drugs that do not have therapeutic competition would add additional leverage.

Conversely, other policies, such as requiring certain drugs to be covered, could weaken the Secretary’s bargaining position. An illustration of such a policy is provided by the requirement, which does not apply to commercial insurers, that Medicare Part D plans cover certain drugs—specifically, all drugs in six “protected” therapeutic classes. That requirement improves beneficiaries’ access to those drugs, but it also diminishes the leverage of plans to obtain lower net prices for them. Without the ability to exclude a drug from a formulary, the authority to negotiate would, on its own, be unlikely to yield prices below those paid by commercial plans and could result in prices that were higher than the prices paid by those plans.

Authorizing the HHS Secretary to negotiate prescription drug prices would be a new approach, so resolving implementation challenges would probably take more time. Moreover, if the Secretary was granted discretion in the negotiation of drug prices, the Secretary’s willingness to limit access to certain high-priced drugs to secure lower average prices could change with Administrations.

Contract With a Private Entity

Contracting with a pharmacy benefit manager and granting it the authority to negotiate with drug manufacturers on behalf of the public option would be most similar to the approach taken by private insurers and self-insured employers. In that scenario, a PBM would negotiate prices with drug manufacturers under market conditions similar to those that private insurers face and thus would most likely reach agreement on similar prices. Many of the same bargaining tools that would be available to an HHS Secretary who was authorized to negotiate drug prices would also be available to a PBM, and any requirements placed on the public option’s formularies—such as a minimum number of drugs within a therapeutic class that it must cover—could weaken the PBM’s leverage, just as they would the Secretary’s leverage.

The net prices paid for prescription drugs under the public option would be greatly affected by the rebates that the PBM received from drug manufacturers. PBMs can secure rebates by including a manufacturer’s drug on a plan’s formulary or by placing the drug in a tier that requires beneficiaries to pay a smaller amount, making it more attractive to beneficiaries than competing drugs.19 Thus, the prices paid by the public option would depend on the leverage available to the PBM to negotiate rebates, which would, in turn, depend on whether the public option managed beneficiaries’ use of prescription drugs through tiered formularies and similar approaches.20

Set Prices in Law or Regulation

If prices were set by statute, the administered prices could vary widely on the basis of how those prices were determined. For example, if prices were set around the average prices paid in Medicare Part D, they would be substantially higher than if they were based on prices paid in Medicaid. (The Medicaid Drug Rebate Program, which specifies the rebates that drug manufacturers must pay to state Medicaid agencies, keeps prices in the program relatively low.) Policymakers could also grant the public option the authority to use prices in the federal supply schedule for pharmaceuticals, which establishes prices for all federal purchasers that buy drugs directly from wholesalers or manufacturers and provide their own dispensing services. Those prices, which are determined by statutory rebates and negotiation between the Department of Veterans Affairs and drug manufacturers, fall between Medicaid prices and Medicare Part D prices. The simplest approach, administratively, would be for the statute to require that prices be based on an existing fee schedule.

Tying drug prices in the public option to prices in private markets or in another federal program could have spillover effects on other payers. In Medicaid, for example, manufacturers currently owe a rebate that is based in part on the lowest price paid by any buyer, excluding certain government programs. That rebate makes it more costly for manufacturers to offer large discounts to those buyers because doing so increases the rebate under Medicaid; consequently, they charge higher prices in the private market than they would otherwise for brand-name drugs. That spillover effect is greater for drugs with a larger Medicaid market share.21 If the public option paid lower prices for drugs, that could also hinder pharmaceutical innovation, especially if it had a sizable effect on manufacturers’ revenue streams from different pharmaceutical products. However, any such effect would probably be negligible because the nongroup public option’s market share is expected to be relatively small.

Provider Participation and Ties to Participation in Medicare and Medicaid

To construct a provider network for the public option, policymakers could tie participation in the public option to participation in other public programs. They could, for example, make participation in the public option a condition of participating in Medicare.22 Tying participation in the public option to participation in other public programs could result in a broader provider network and thus increase the attractiveness of the public option. Survey data suggest that according to some measures—such as patients’ having a usual source of care and providers’ acceptance rates for new patients—Medicare beneficiaries’ access to care is comparable to or better than that of people with private health insurance.23

For many types of care, the Medicare provider network would probably provide sufficient coverage for public option enrollees. However, some types of providers, including pediatricians, are currently underrepresented in Medicare, so limiting required participation to Medicare-certified providers might not result in an adequate provider network for a nongroup public option. If provider payment rates were determined through negotiation, requiring Medicare providers to participate in the public option would give the public option more negotiating leverage and could support lower payment rates. CBO does not expect that requiring Medicare providers to participate in the public option would cause a substantial number of providers to opt out of Medicare because the number of people enrolled in marketplace plans is much smaller than the number enrolled in Medicare. However, for the specialties that are underrepresented in Medicare, the public option’s negotiating leverage associated with participation requirements would be substantially weaker.

Policymakers could extend the participation requirement to providers who participate in Medicaid. Doing so would increase patient access and add to the number of providers in specialties such as pediatrics in the public option’s network, though Medicaid patients’ access to physicians tends to be more limited than that of privately insured or Medicare patients. The limited access to care in Medicaid is driven by several factors, including that the program has lower payment rates and higher rates of denied claims than private insurance and Medicare.24 However, the public option might not have those issues: It would have different plan characteristics from Medicaid, so, even without a statutory requirement, Medicaid providers might find participating in the public option attractive.

Requiring providers who participate in Medicare or Medicaid to also participate in the public option would not, in itself, guarantee access to care for public option enrollees. For instance, providers might limit the availability of appointments for public option enrollees or see enrollees only at certain clinics. In addition to tying participation in the public option to participation in other public programs, policymakers could specify access standards. For example, they could ensure that a minimum percentage of contracted providers were accepting new patients, or they could establish maximum wait times for appointments with providers.25 The Centers for Medicare & Medicaid Services and state Medicaid agencies might have difficulty enforcing those standards.

Alternatively, policymakers could choose not to require Medicare or Medicaid providers to participate in the public option.26 In that case, provider payment rates would be one important factor in a provider’s decision to participate in the program. Another factor that could affect provider participation would be whether the program was structured to require certain providers to opt in or out. If, for example, Medicare providers had to opt out—that is, if those providers participated in the public option by default—participation would probably be greater than if providers had to opt in. Policymakers could also use a number of other strategies to encourage participation, such as forgiving qualifying providers’ medical school loans.

Administrative Activities and Taxes

The costs of administering the public option would depend on the design choices made by policymakers. A nationally standardized public option—for example, one that used administered rates based on Medicare, the Medicare provider network, and a single benefit package—would have larger economies of scale and lower administrative costs than a public option with negotiated payment rates, a tailored provider network, and benefit packages that varied by state.

One important determinant of administrative costs is the care management strategies that are used, such as requiring prior authorization for medical services and referrals for specialty care. Such strategies increase the administrative costs of operating the plan but decrease the quantity of health care services utilized and thus lower the overall costs of the plan. Medicare fee-for-service employs fewer care management tools than Medicare Advantage or commercial insurers, on average. For example, the program does not require prior authorization (except under limited circumstances), it does not require patients to obtain a referral before their initial visit to many types of specialists, and it does not impose direct limits on the number of appointments with physicians that it will cover each year.27 If the public option used care management strategies that were more intensive than those used by Medicare FFS, it would have to define those protocols. CBO expects that the reductions in utilization and claims costs associated with care management strategies could offset the increased administrative costs of using them, but the offsetting effects are generally uncertain.28

Policymakers could choose whether the public option would advertise and, if so, whether the advertising campaign would be specifically for the public plan or for marketplace coverage more broadly.29 Similarly, policymakers could choose whether to pay brokers to help people enroll in the public option, as private insurers often do.30

The public option’s administrative costs could include several types of taxes and fees that private insurers are required to pay, or the public option could be exempted from those taxes and fees.31 For example, private insurers must pay a user fee to offer plans through the online health insurance marketplace platform operated by the federal government; the public option could be exempted from that fee.32 States generally do not have the authority to impose taxes on federal programs, such as Medicare Advantage, Medicare Part D, and Federal Employees Health Benefits plans.33 The Congress could, however, require the public option to make payments to states instead of paying taxes on premiums. Additionally, it could specify that the public option would pay states that operated their own marketplace platform a fee to use the platform.

Risk-Adjustment Transfers

Enrollees in the nongroup plans available in the marketplaces are part of a single risk pool, and the private insurers offering those plans participate in a risk-adjustment system that spreads the risk among themselves.34 Insurers with healthier enrollees make payments to insurers with less healthy enrollees within a state to limit the financial incentive that insurers have to seek out healthier enrollees and avoid sicker ones. The total value of funds in the risk-adjustment pool depends in part on a state’s average premium.

Policymakers would need to decide whether the public option would share a risk pool with private insurers in the nongroup market. If private insurers and the public option were part of a single risk pool, risk-adjustment transfers would be made among private insurers and the public option on the basis of the relative health of the plans’ enrollees. If the public option attracted disproportionately sicker enrollees, private insurers would make transfer payments to the public option. However, risk adjustment does not perfectly capture differences in individual health risk, so those transfers would not fully reflect the underlying health risk of enrollees. Moreover, evidence from other markets suggests that insurers might behave strategically to increase the risk score that they report for their enrollees.35 If private insurers engaged in that behavior more than the public option did, risk-adjustment transfers would favor private insurers, and the public option’s premiums would be higher as a result.

If people enrolled in the public option made up their own separate risk pool, differences between the public option’s premiums and those of private plans would reflect differences in enrollees’ health status. Private insurers’ incentive to use strategies to attract healthier enrollees would be stronger than it is under the current system. Healthier enrollees who would otherwise have enrolled in the public option might instead purchase coverage from those private insurers, worsening the public option’s risk pool. Furthermore, if the public option’s risk pool was separate from that of private insurers, the premium of the benchmark plan could reflect enrollees with substantially different health risks from those enrolled in the public option.

Funding and Treatment of Excess Revenues and Shortfalls

The public option could be funded through premium payments (including premium tax credit payments as well as enrollees’ premium contributions) and separate appropriations from the Congress. Those appropriations could be made annually, or policymakers could provide only start-up funding. CBO anticipates that the start-up costs for a public option could be substantial. Such costs would include those associated with establishing payment rates, enrolling providers, advertising, addressing unforeseen implementation problems, and providing sufficient reserve funds to cover initial claims costs. Policymakers could require the public option to use its premium revenues to pay back the start-up costs over a specified period of time.36 In general, the public option’s premiums would be lower if it was not required to repay any start-up funding it received through the appropriation process.