At a Glance

The Congressional Budget Office regularly publishes reports presenting projections of what federal budget deficits, debt, revenues, and spending—and the economic path underlying them—would be for the current year and for the following 10 years if current laws governing taxes and spending generally remained unchanged. For this report, the latest in the series, the projections are based on the laws in effect as of January 12, 2021. CBO’s economic assessment is identical to the forecast the agency published on February 1, 2021.

- Deficits. CBO projects a federal budget deficit of $2.3 trillion in 2021, nearly $900 billion less than the shortfall recorded in 2020. At 10.3 percent of gross domestic product (GDP), the deficit in 2021 would be the second largest since 1945, exceeded only by the 14.9 percent shortfall recorded last year. Those deficits, which were already projected to be large by historical standards before the onset of the 2020–2021 coronavirus pandemic, have widened significantly as a result of the economic disruption caused by the pandemic and the enactment of legislation in response.

In CBO’s projections, annual deficits average $1.2 trillion a year from 2022 to 2031 and exceed their 50-year average of 3.3 percent of GDP in each of those years. They decline to 4.0 percent of GDP or less from 2023 to 2027 before increasing again, reaching 5.7 percent of GDP in 2031. By the end of the period, both primary deficits (which exclude net outlays for interest) and interest outlays are rising.

- Debt. Federal debt held by the public—which stood at 100 percent of GDP at the end of fiscal year 2020—is projected to reach 102 percent of GDP at the end of 2021, dip slightly for a few years, and then rise further. By 2031, debt would equal 107 percent of GDP, the highest in the nation’s history.

- Revenues. Federal revenues are projected to generally increase relative to GDP as a result of the expiration of temporary pandemic-related provisions, scheduled increases in taxes, and other factors.

- Outlays. Projected outlays decline relative to GDP for the next few years, as pandemic-related spending wanes and low interest rates persist. Outlays then increase relative to GDP, owing to rising interest costs and greater spending for major entitlement programs.

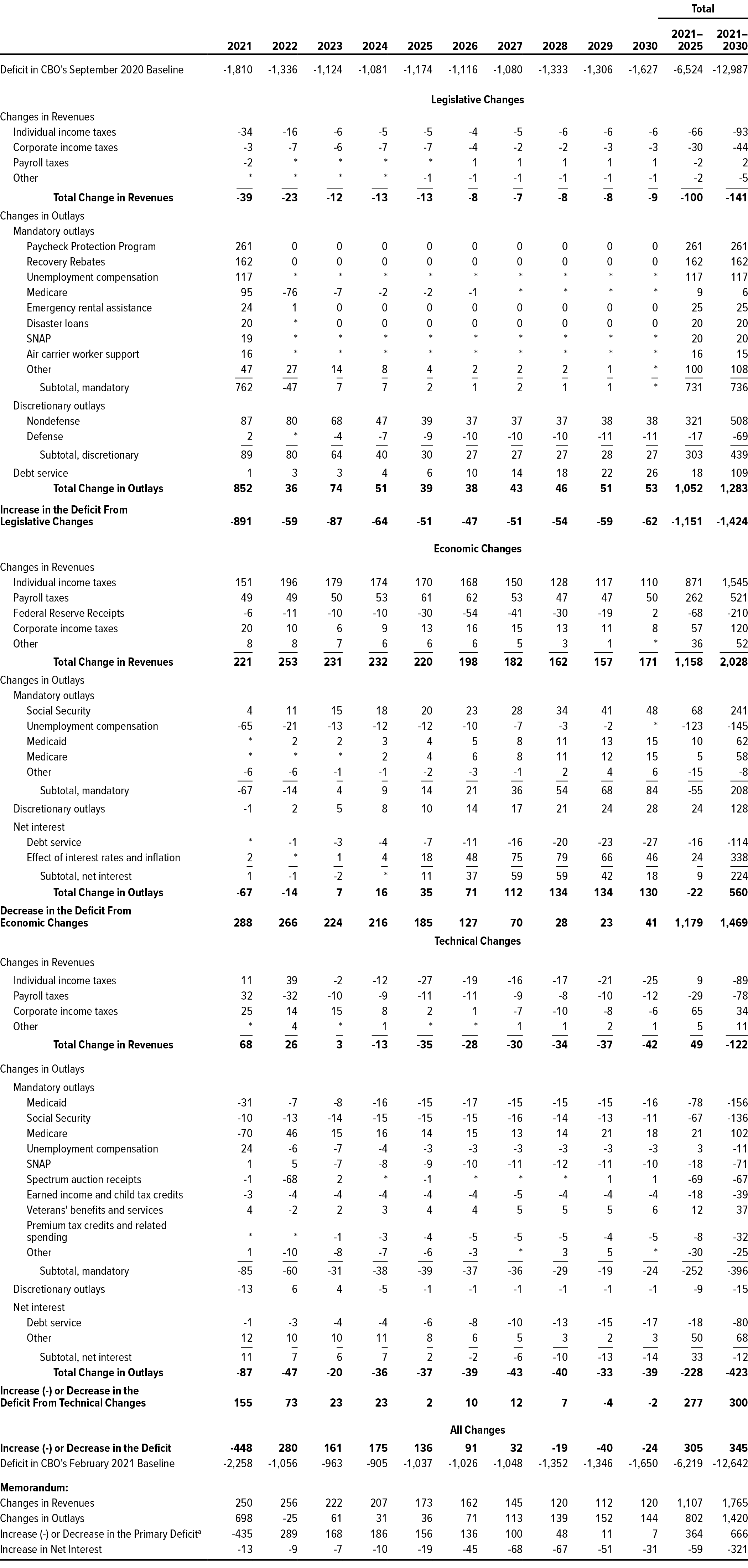

- Changes Since CBO’s Previous Projections. Relative to its estimates from September 2020, CBO’s estimate of the deficit for 2021 is now $448 billion (or 25 percent) larger, and its projection of the cumulative deficit between 2021 and 2030 (at $12.6 trillion) is now $345 billion (or 3 percent) smaller. In 2021, the costs of recently enacted legislation are partly offset by the effects of a stronger economy. In subsequent years, the largest changes stem from revisions to the economic forecast. CBO now projects stronger economic activity, higher inflation, and higher interest rates, boosting both revenues and outlays—the former more than the latter.

- The Economy. As expanded vaccination reduces the spread of COVID-19 (the disease caused by the coronavirus) and the extent of social distancing declines, real (inflation-adjusted) GDP is projected to grow by 3.7 percent in 2021, returning to its prepandemic level by the middle of the year. With growth averaging 2.6 percent over the 2021–2025 period, real GDP surpasses its potential (maximum sustainable) level in early 2025. The unemployment rate gradually declines through 2026, and the number of employed people returns to its prepandemic level in 2024.

Real GDP growth averages 1.6 percent over the 2026–2031 period. That average growth rate of output is less than its long-term historical average, primarily because the labor force is expected to grow more slowly than it has in the past. Over the forecast period, the interest rate on 10-year Treasury notes is projected to rise gradually, reaching 3.4 percent in 2031.

Notes

Notes

The budget projections in this report include the effects of legislation enacted through January 12, 2021, and are based on the Congressional Budget Office’s economic projections. Those economic projections reflect economic developments through January 12, 2021, including the estimated effects on the economy of the Consolidated Appropriations Act, 2021 (Public Law 116-260). The projections do not include budgetary or economic effects of subsequent legislation, economic developments, administrative actions, or regulatory changes.

The economic projections were also published separately on February 1, 2021, to provide the Congress with information as promptly as possible as it continued to address the consequences of the 2020–2021 coronavirus pandemic (www.cbo.gov/publication/56965).

Because the timing of the Consolidated Appropriations Act, 2021, did not allow enough time for all of the analysis and writing that CBO typically performs, this report omits some material that has often appeared in past editions. Certain long-term budget projections will be published separately on February 16, 2021. Other material will be published separately later this year.

Unless this report indicates otherwise, all years referred to in describing the budget outlook are federal fiscal years, which run from October 1 to September 30 and are designated by the calendar year in which they end. Years referred to in describing the economic outlook are calendar years.

Numbers in the text, tables, and figures may not add up to totals because of rounding.

Supplemental data for this analysis are available on CBO’s website (www.cbo.gov/publication/56970), as are a glossary of common budgetary and economic terms (www.cbo.gov/publication/42904), a description of how CBO prepares its baseline budget projections (www.cbo.gov/publication/53532), a description of how CBO prepares its economic forecast (www.cbo.gov/publication/53537), and previous editions of this report (https://go.usa.gov/xQrzS).

Chapter 1The Budget Outlook

This chapter provides the Congressional Budget Office’s latest baseline budget projections, spanning fiscal years 2021 through 2031. These projections are based on the economic forecast that the agency developed in January 2021. (For CBO’s assessment of the economic outlook, see Chapter 2, which is identical to the assessment the agency published on February 1, 2021.) These projections incorporate legislation enacted through January 12, 2021, as well as information available as of that date.

CBO’s projections are constructed in accordance with the Balanced Budget and Emergency Deficit Control Act of 1985 (Public Law 99-177) and the Congressional Budget and Impoundment Control Act of 1974 (P.L. 93-344). Those laws require CBO to construct its baseline under the assumption that current laws governing revenues and spending will generally stay the same and that discretionary appropriations in future years will match current funding, with adjustments for inflation.

In consultation with the House and Senate Committees on the Budget, however, CBO deviated from those standard procedures when constructing its current baseline for discretionary spending. Because of the unusual size and nature of the emergency funding provided in response to the 2020–2021 coronavirus pandemic, the agency did not extrapolate the $184 billion in discretionary budget authority that has been provided for such purposes so far in 2021. Emergency funding provided for purposes unrelated to the pandemic was projected to continue in the future with increases for inflation each year after 2021.

CBO’s baseline is not intended to provide a forecast of future budgetary outcomes; rather, it provides a benchmark that policymakers can use to assess the potential effects of future policy decisions. Future legislative action could lead to markedly different outcomes. Even if federal laws remained unaltered for the next decade, though, actual budgetary outcomes would probably differ from CBO’s baseline—not only because of unanticipated economic developments, but also as a result of the many other factors that affect federal revenues and outlays.

This presentation of CBO’s budget projections is much shorter than usual. The information is less detailed so that CBO can provide it to lawmakers as quickly as possible as they continue to address the consequences of the pandemic. CBO will publish more detailed information about these projections and supplementary information later this year.

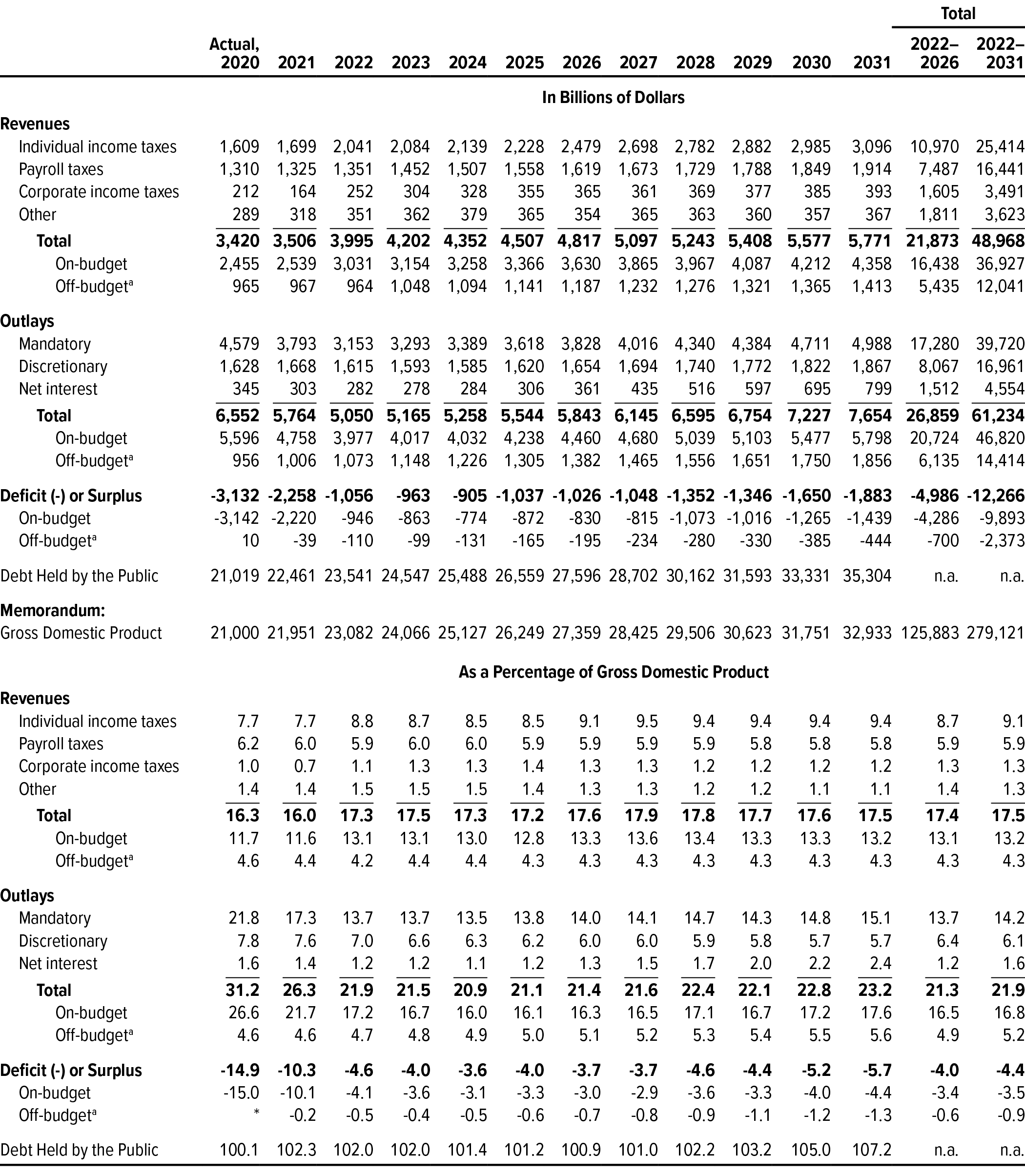

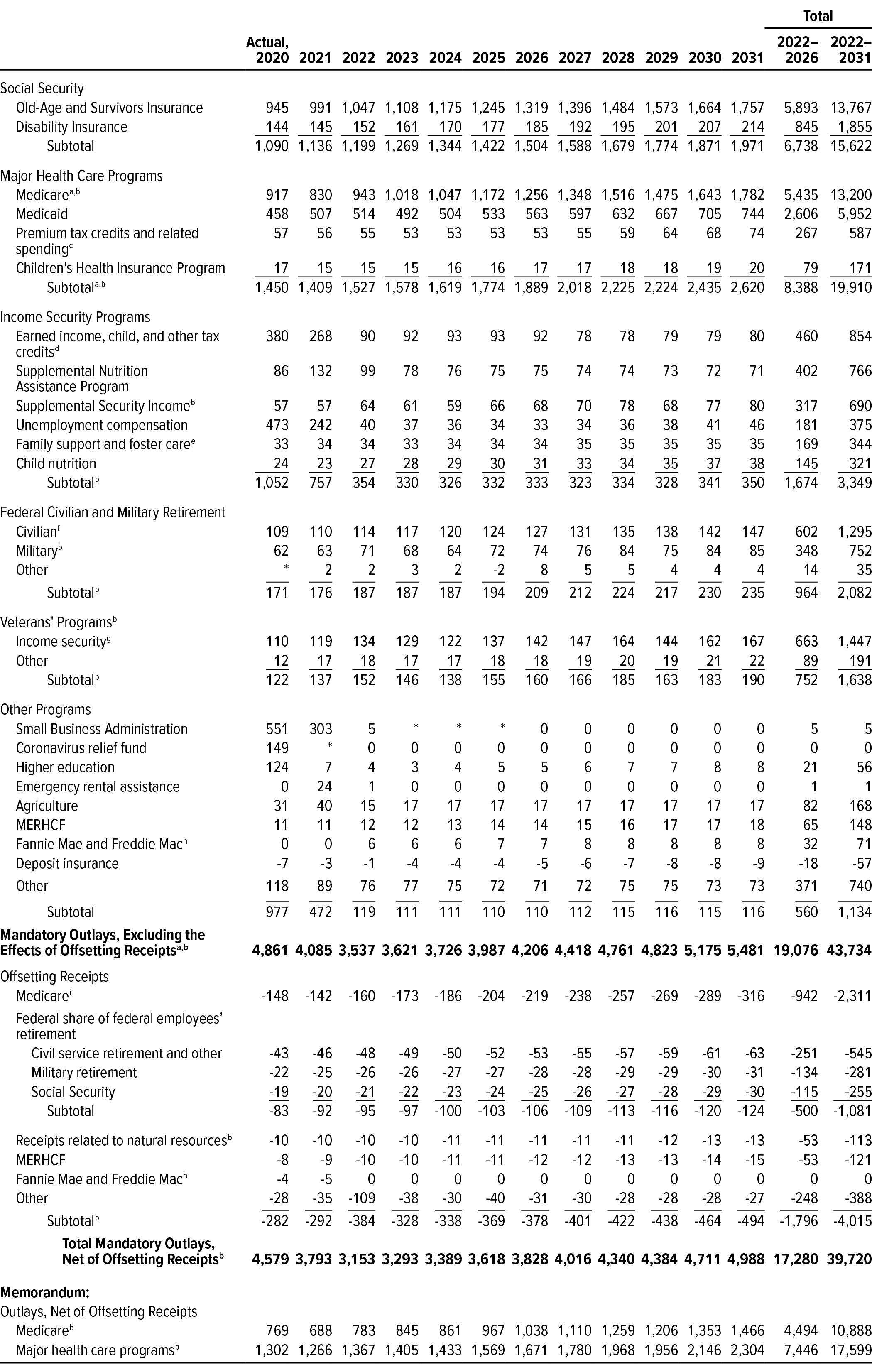

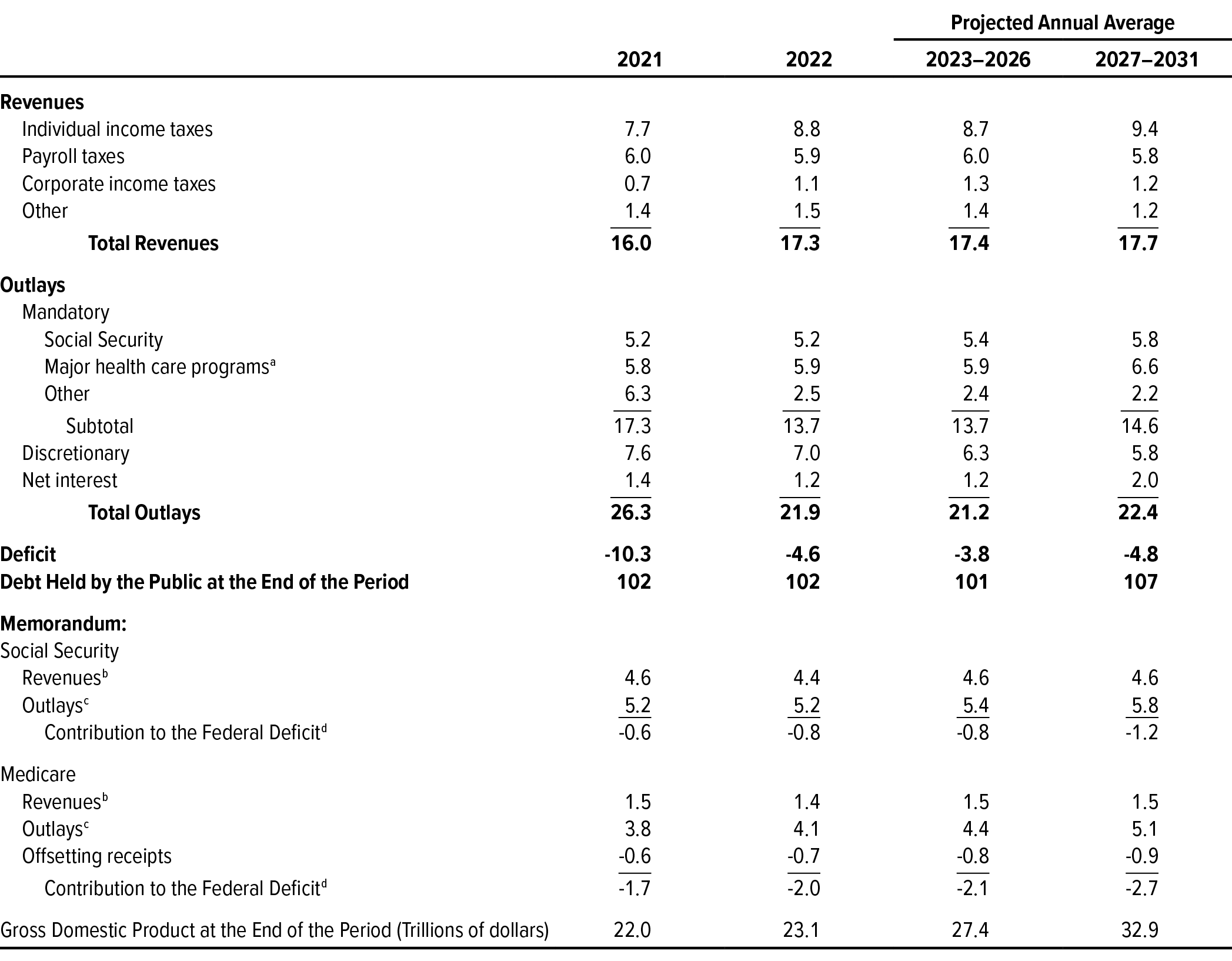

This chapter comprises six tables. The first one shows CBO’s projections for the budget, by major category; projected deficits amount to $2.3 trillion in fiscal year 2021 and $12.3 trillion over the 2022–2031 period (see Table 1-1). Next are CBO’s projections of federal debt; debt held by the public is projected to reach $35.3 trillion, or 107 percent of gross domestic product (GDP), in 2031 (see Table 1-2). Then additional details are presented about mandatory outlays; taken together, outlays for Social Security and Medicare are projected to almost double over 10 years (see Table 1-3).1 Additional details follow about discretionary spending; annual discretionary outlays from 2022 through 2026 are projected to be less than outlays in 2021, which were boosted by pandemic-related spending (see Table 1-4).2 The next table gives a summary of key projections as specified in section 3111 of S. Con. Res. 11, the Concurrent Resolution on the Budget for Fiscal Year 2016; projected deficits average 4.8 percent of GDP from 2027 through 2031 (see Table 1-5). Finally, detailed information is provided about how CBO’s projections have changed since September 2020; deficits are larger in 2021 but smaller in total from 2021 through 2030 than CBO projected in September (see Table 1-6). For CBO’s analysis of the budgetary effects of tax expenditures in 2021, see the appendix.

Table 1-1.

CBO’s Baseline Budget Projections, by Category

Data source: Congressional Budget Office. See www.cbo.gov/publication/56970#data.

n.a. = not applicable; * = between zero and 0.05 percent.

a. The revenues and outlays of the Social Security trust funds and the net cash flow of the Postal Service are classified as off-budget.

Table 1-2.

CBO’s Baseline Projections of Federal Debt

Billions of Dollars

Data sources: Congressional Budget Office; Department of the Treasury. See www.cbo.gov/publication/56970#data.

GDP = gross domestic product.

a. Factors not included in budget totals that affect the government’s need to borrow from the public. Those factors include changes in the government’s cash balances, as well as cash flows associated with federal credit programs such as student loans (because only the subsidy costs of those programs are reflected in the budget deficit).

b. Debt held by the public minus the value of outstanding student loans and other credit transactions, cash balances, and various financial instruments.

c. Federal debt held by the public plus Treasury securities held by federal trust funds and other government accounts.

d. The amount of federal debt that is subject to the overall limit set in law. That measure of debt excludes debt issued by the Federal Financing Bank and reflects certain other adjustments that are excluded from gross federal debt. The debt limit was most recently set at $22.0 trillion but has been suspended through July 31, 2021. On August 1, 2021, the debt limit will be raised to its previous level plus the amount of federal borrowing that occurred while the limit was suspended. For more details, see Congressional Budget Office, Federal Debt and the Statutory Limit, February 2019 (February 2019), www.cbo.gov/publication/54987.

Table 1-3.

Mandatory Outlays Projected in CBO’s Baseline

Billions of Dollars

Data source: Congressional Budget Office. See www.cbo.gov/publication/56970#data.

Data on outlays for benefit programs in this table generally exclude administrative costs, which are discretionary.

MERHCF = Department of Defense Medicare-Eligible Retiree Health Care Fund (including TRICARE for Life); * = between zero and $500 million.

a. Excludes the effects of Medicare premiums and other offsetting receipts. (Net Medicare spending, which includes those offsetting receipts, is shown in the memorandum section of the table.) The projections include the estimated effects of a final rule that would eliminate safe harbor protections for rebates paid by pharmaceutical manufacturers to health plans and pharmacy benefit managers in Medicare Part D. On January 29, 2021, the effective date for that rule was delayed from January 1, 2022, to January 1, 2023. CBO will reflect the effects of the postponement and any other subsequent actions in future projections.

b. When October 1 (the first day of the fiscal year) falls on a weekend, as it will in calendar years 2022, 2023, and 2028, certain payments that would ordinarily have been made on that day are instead made at the end of September and thus are shifted into the previous fiscal year.

c. Premium tax credits are federal subsidies for health insurance purchased through the marketplaces established by the Affordable Care Act. Related spending consists almost entirely of payments for risk adjustment and the Basic Health Program.

d. Includes outlays for recovery rebates for individuals, the American Opportunity Tax Credit, and other credits.

e. Includes Temporary Assistance for Needy Families, Child Support Enforcement, Child Care Entitlements to States, and other programs that benefit children.

f. Includes benefits for retirement programs in the civil service, foreign service, and Coast Guard; benefits for smaller retirement programs; and annuitants’ health care benefits.

g. Includes veterans’ compensation, pensions, and life insurance programs. (Outlays for veterans’ health care are classified as discretionary.)

h. Cash payments from Fannie Mae and Freddie Mac to the Treasury are recorded as offsetting receipts in 2020 and 2021. Beginning in 2022, CBO’s estimates reflect the net lifetime costs—that is, the subsidy costs adjusted for market risk—of the guarantees that those entities will issue and of the loans that they will hold. CBO counts those costs as federal outlays in the year of issuance.

i. Includes premium payments, recoveries of overpayments made to providers, and amounts paid by states from savings on Medicaid’s prescription drug costs.

Table 1-4.

CBO’s Baseline Projections of Discretionary Spending

Billions of Dollars

Data source: Congressional Budget Office. See www.cbo.gov/publication/56970#data.

CBO’s current baseline projections incorporate the assumption that the caps on discretionary budget authority and the automatic enforcement procedures specified in the Budget Control Act of 2011 (as amended) remain in effect through 2021. The cap on defense funding in 2021 was set at $671.5 billion, and the nondefense cap was set at $626.5 billion. Total budget authority in 2021 exceeds the sum of those amounts because of adjustments made to those caps as provided in law, changes in mandatory programs that are credited against appropriations, and certain other funding that does not count toward those caps. For more information, see Congressional Budget Office, Final Sequestration Report for Fiscal Year 2021 (January 2021), www.cbo.gov/publication/56955.

Nondefense discretionary outlays are usually greater than budget authority because of spending from the Highway Trust Fund and the Airport and Airway Trust Fund that is subject to obligation limitations set in appropriation acts. The budget authority for such programs is provided in authorizing legislation and is considered mandatory.

n.a. = not available; * = between zero and $500 million.

a. Certain laws require CBO to construct its baseline under the assumption that discretionary appropriations in future years will match current funding, with adjustments for inflation. In consultation with the House and Senate Committees on the Budget, however, CBO deviated from those standard procedures when constructing its current baseline for discretionary spending. Because of the unusual size and nature of the emergency funding provided in legislation enacted specifically in response to the 2020–2021 coronavirus pandemic, the agency did not extrapolate the $184 billion in discretionary budget authority that has been provided for such purposes so far in 2021. Emergency funding provided for purposes unrelated to the pandemic was projected to continue in the future with increases for inflation each year after 2021.

b. The Department of the Treasury does not distinguish between outlays stemming from emergency funding and outlays stemming from nonemergency funding. Consequently, the budget does not record any actual amounts attributed specifically to that category of funding.

Table 1-5.

Key Projections in CBO’s Baseline

Percentage of Gross Domestic Product

Data source: Congressional Budget Office. See www.cbo.gov/publication/56970#data.

This table satisfies a requirement specified in section 3111 of S. Con. Res. 11, the Concurrent Resolution on the Budget for Fiscal Year 2016.

a. Consists of outlays for Medicare (net of premiums and other offsetting receipts), Medicaid, the Children’s Health Insurance Program, subsidies for health insurance purchased through the marketplaces established under the Affordable Care Act, and related spending.

b. Includes payroll taxes other than those paid by the federal government on behalf of its employees; those payments are intragovernmental transactions. Also includes income taxes paid on Social Security benefits, which are credited to the trust funds.

c. Does not include outlays related to the administration of the program, which are discretionary. For Social Security, outlays do not include intragovernmental offsetting receipts stemming from the employer’s share of payroll taxes paid to the Social Security trust funds by federal agencies on behalf of their employees.

d. The net increase in the deficit shown in this table differs from the change in the trust fund balance for the associated program. It does not include intragovernmental transactions, interest earned on balances, or outlays related to the administration of the program.

Table 1-6.

Changes in CBO’s Baseline Projections of the Deficit Since September 2020

Billions of Dollars

Data source: Congressional Budget Office. See www.cbo.gov/publication/56970#data.

SNAP = Supplemental Nutrition Assistance Program; * = between -$500 million and $500 million.

a. Primary deficits exclude net outlays for interest.

1. Mandatory spending consists of outlays for some federal benefit programs, such as Social Security, Medicare, and Medicaid, and certain other payments to people, businesses, nonprofit institutions, and state and local governments. It is governed by statutory criteria and is not normally controlled by the annual appropriation process.

2. Discretionary spending is controlled by appropriation acts that specify the amounts that are to be provided for a broad array of government activities, including, for example, defense, law enforcement, and transportation.

Chapter 2The Economic Outlook

The 2020–2021 coronavirus pandemic caused severe economic disruptions last year as households, governments, and businesses adopted a variety of mandatory and voluntary measures—collectively referred to here as social distancing—to limit in-person interactions that could spread the virus. The impact was focused on particular sectors of the economy, such as travel and hospitality, and job losses were concentrated among lower-wage workers.

Over the course of the coming year, vaccination is expected to greatly reduce the number of new cases of COVID-19, the disease caused by the coronavirus. As a result, the extent of social distancing is expected to decline. In its new economic forecast, which covers the period from 2021 to 2031, the Congressional Budget Office therefore projects that the economic expansion that began in mid-2020 will continue (see Table 2-1). Specifically, real (inflation-adjusted) gross domestic product (GDP) is projected to return to its prepandemic level in mid-2021 and to surpass its potential (that is, its maximum sustainable) level in early 2025.1 In CBO’s projections, the unemployment rate gradually declines through 2026, and the number of people employed returns to its prepandemic level in 2024.

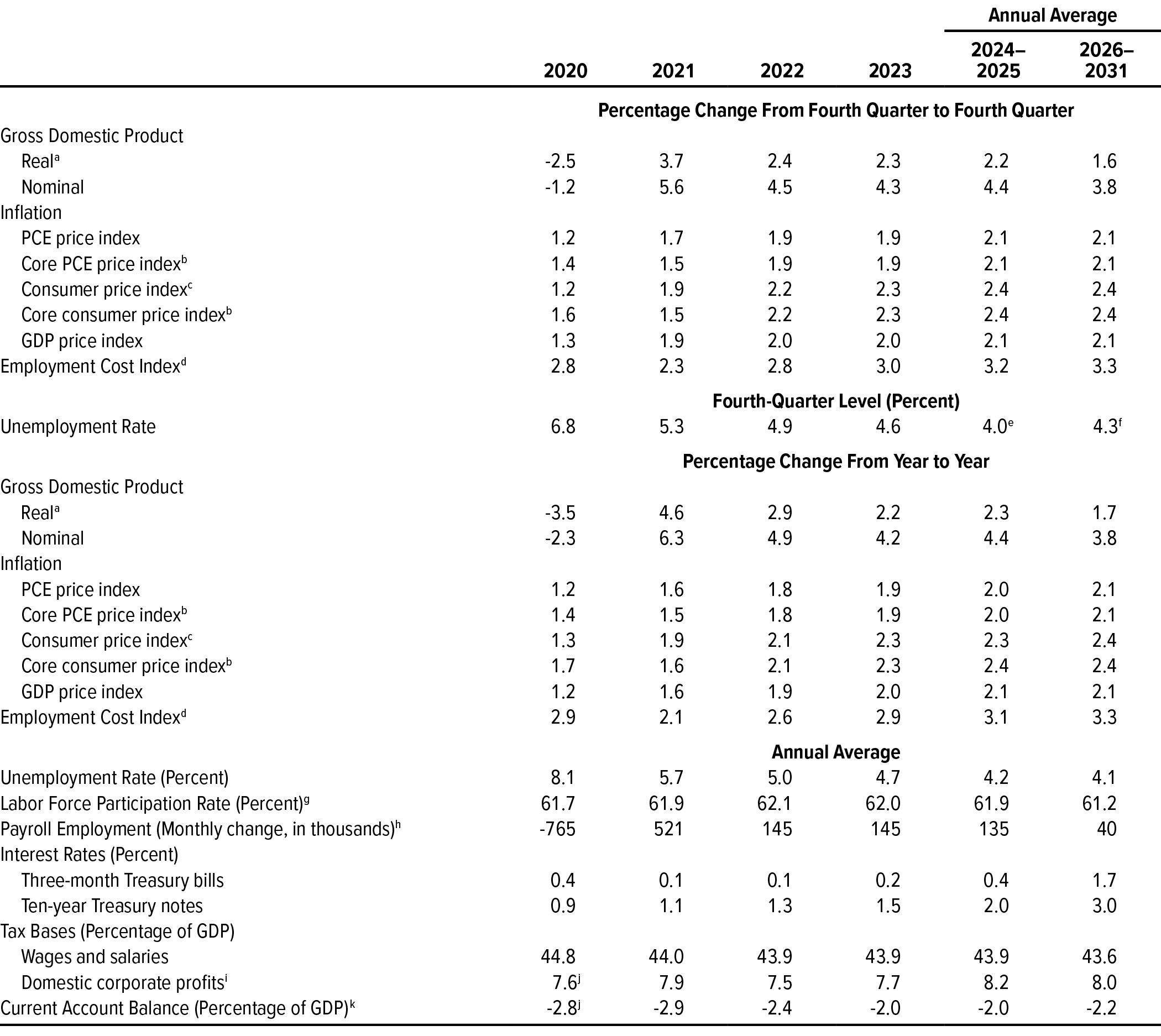

Table 2-1.

CBO’s Economic Projections for Calendar Years 2021 to 2031

Data sources: Congressional Budget Office; Bureau of Economic Analysis; Bureau of Labor Statistics; Federal Reserve. See www.cbo.gov/publication/56970#data.

GDP = gross domestic product; PCE = personal consumption expenditures.

a. Real values are nominal values that have been adjusted to remove the effects of changes in prices.

b. Excludes prices for food and energy.

c. The consumer price index for all urban consumers.

d. The employment cost index for wages and salaries of workers in private industry.

e. Value for the fourth quarter of 2025.

f. Value for the fourth quarter of 2031.

g. The share of the civilian noninstitutionalized population age 16 or older that has jobs or that is available for and actively seeking work.

h. The average monthly change in the number of employees on nonfarm payrolls, calculated by dividing the change from the fourth quarter of one calendar year to the fourth quarter of the next by 12.

i. Adjusted to remove distortions in depreciation allowances caused by tax rules and to exclude the effects of changes in prices on the value of inventories.

j. Estimated value for 2020.

k. Represents net exports of goods and services, net capital income, and net transfer payments between the United States and the rest of the world.

This forecast underlies the budget projections that are presented in Chapter 1. The forecast incorporates economic and other information available as of January 12, 2021, as well as estimates of the economic effects of all legislation (including pandemic-related legislation) enacted up to that date.

The Economic Outlook for 2021 to 2025

In CBO’s projections, which incorporate the assumptions that current laws governing federal taxes and spending (as of January 12) generally remain in place and that no significant additional emergency funding or aid is provided, the economy continues to strengthen during the next five years.

- Real GDP expands rapidly over the coming year, reaching its previous business-cycle peak (which was attained in the fourth quarter of 2019) in mid-2021 and surpassing its potential level in early 2025. The annual growth of real GDP averages 2.6 percent during the five-year period, exceeding the 1.9 percent growth rate of real potential GDP (see Figure 2-1).

Figure 2-1.

The Relationship Between GDP and Potential GDP

In CBO’s projections, the annual growth of real (inflation-adjusted) GDP exceeds that of real potential GDP until 2026.

The output gap between real GDP and real potential GDP is positive for several years, starting in 2025, before moving back toward its historical average.

Data sources: Congressional Budget Office; Bureau of Economic Analysis. See www.cbo.gov/publication/56970#data.

Real values are nominal values that have been adjusted to remove the effects of changes in prices. Potential GDP is CBO’s estimate of the maximum sustainable output of the economy. Growth of real GDP and of real potential GDP is measured from the fourth quarter of one calendar year to the fourth quarter of the next.

The output gap is the difference between GDP and potential GDP, expressed as a percentage of potential GDP. A positive value indicates that GDP exceeds potential GDP; a negative value indicates that GDP falls short of potential GDP. Values for the output gap are for the fourth quarter of each year.

The shaded vertical bars indicate periods of recession, which extend from the peak of a business cycle to its trough. The National Bureau of Economic Research (NBER) has determined that an expansion ended and a recession began in February 2020. Although the NBER has not yet identified the end of that recession, CBO estimates that it ended in the second quarter of 2020.

GDP = gross domestic product.

- Labor market conditions continue to improve. As the economy expands, many people rejoin the civilian labor force who had left it during the pandemic, restoring it to its prepandemic size in 2022.2 The unemployment rate gradually declines throughout the period, and the number of people employed returns to its prepandemic level in 2024.

- Inflation, as measured by the price index for personal consumption expenditures, rises gradually over the next few years and exceeds 2.0 percent after 2023, as the Federal Reserve maintains low interest rates and continues to purchase long-term securities.

- Interest rates on federal borrowing rise. The Federal Reserve maintains the federal funds rate (the rate that financial institutions charge each other for overnight loans of their monetary reserves) near zero through mid-2024 and then starts to raise that rate gradually. The interest rate on 3-month Treasury bills closely follows the federal funds rate. The interest rate on 10-year Treasury notes rises as the Federal Reserve reduces the pace of its asset purchases and investors anticipate rising short-term interest rates later in the decade.

CBO’s projections of economic growth have been boosted by various laws enacted in 2020.3 Most recently, in late December, the Consolidated Appropriations Act, 2021 (Public Law 116-260), appropriated funds for the remainder of fiscal year 2021, provided additional emergency funding for federal agencies to respond to the public health emergency created by the pandemic, and provided financial support to households, businesses, and nonfederal governments affected by the economic downturn, among other measures. CBO estimates that the pandemic-related provisions in that legislation will add $774 billion to the deficit in fiscal year 2021 and $98 billion in 2022.4 Those provisions will boost the level of real GDP by 1.8 percent in calendar year 2021 and by 1.1 percent in calendar year 2022, CBO estimates.

The Economic Outlook for 2026 to 2031

In CBO’s projections, the economy continues to expand from 2026 to 2031. Real GDP grows by 1.6 percent per year, on average (see Table 2-2). Real potential GDP grows slightly more rapidly (see Table 2-3). For most of the period, the Federal Reserve allows inflation to remain above its target level; the level of real GDP likewise remains above the level of real potential GDP for several years. Eventually, less accommodative policies on the part of the Federal Reserve help push GDP back toward its historical average relationship with potential GDP.

Table 2-2.

The Projected Growth of Real GDP and Its Components

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/56970#data.

Real values are nominal values that have been adjusted to remove the effects of changes in prices.

GDP = gross domestic product; * = between zero and 0.05 percentage points.

a. Consists of personal consumption expenditures.

b. Comprises business fixed investment and investment in inventories.

c. Consists of purchases of equipment, nonresidential structures, and intellectual property products.

d. Includes the construction of single-family and multifamily structures, manufactured homes, and dormitories; spending on home improvements; and brokers’ commissions and other ownership transfer costs.

e. Based on the national income and product accounts.

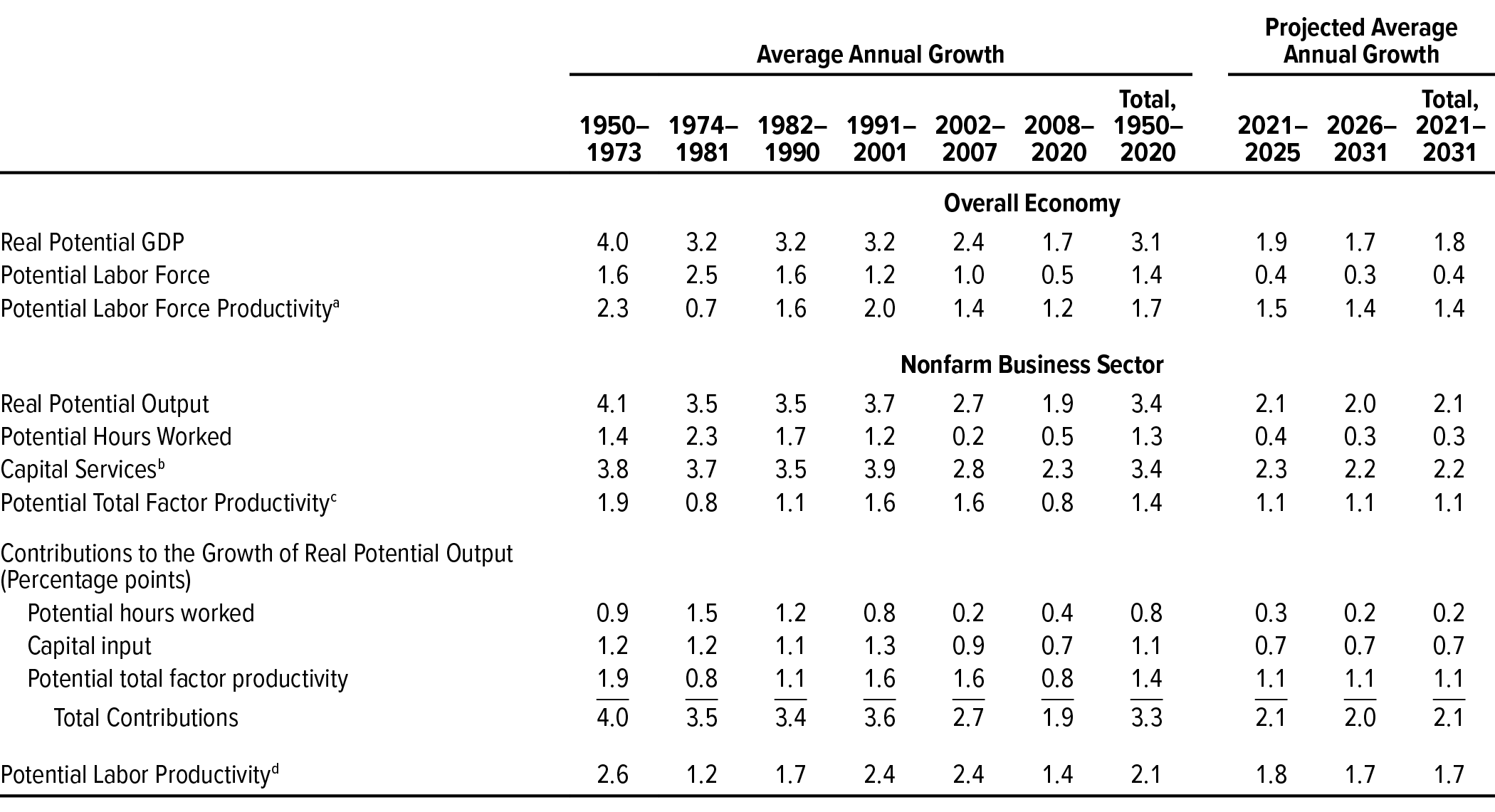

Table 2-3.

Key Inputs in CBO’s Projections of Real Potential GDP

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/56970#data.

Real values are nominal values that have been adjusted to remove the effects of changes in prices. Potential GDP is CBO’s estimate of the maximum sustainable output of the economy.

The table shows compound annual growth rates over the specified periods. Those rates are calculated from the fourth quarter of the year immediately preceding each period to the fourth quarter at the end of that period.

GDP = gross domestic product.

a. The ratio of potential GDP to the potential labor force.

b. The services provided by capital goods (such as computers and other equipment) that constitute the actual input in the production process.

c. The average real output per unit of combined labor and capital services, excluding the effects of business cycles.

d. The ratio of potential output to potential hours worked in the nonfarm business sector.

A mild increase in productivity growth causes potential output in CBO’s projections to grow more quickly over the 2021–2031 period than it has grown since the 2007–2009 recession. However, potential output still grows more slowly than it has grown since 1950, mainly because of an ongoing, long-term slowdown in the growth of the labor force.

Uncertainties in the Economic Outlook

CBO’s projections reflect an average of possible outcomes under current law. But these projections are subject to an unusually high degree of uncertainty, and that uncertainty stems from many sources, including the course of the pandemic, the effectiveness of monetary and fiscal policies, and the response of global financial markets to substantial increases in public deficits and debt. As a result, the economy could expand substantially more quickly or more slowly than CBO projects. Labor market conditions could likewise improve more quickly or slowly than projected, and inflation and interest rates could rise more rapidly or slowly as well. Also uncertain is the impact of the pandemic on the economy over the longer term, including its effects on productivity, the labor force, and technological innovation.

Comparisons With Previous Projections

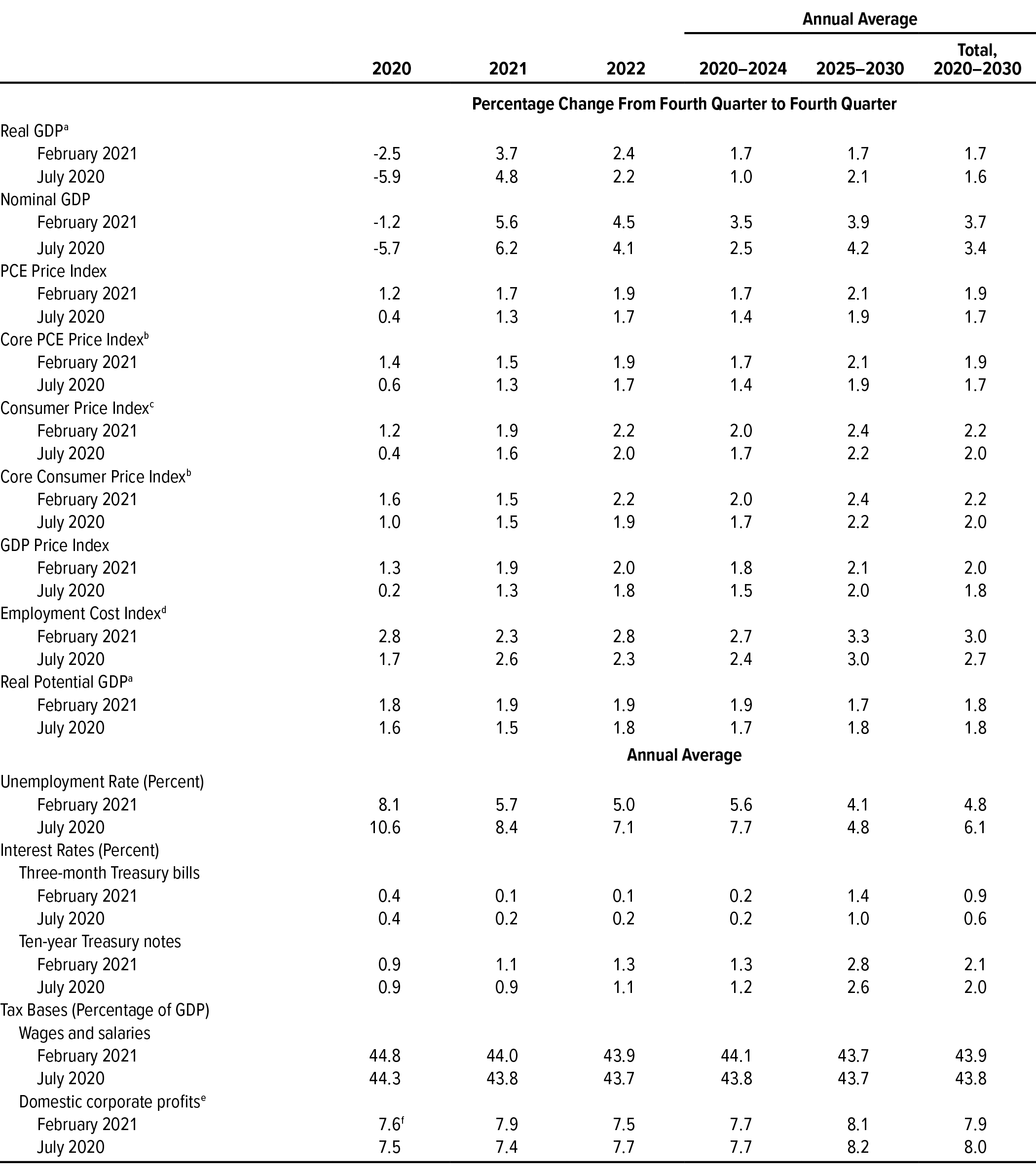

CBO currently projects a stronger economy than it did in July 2020, in large part because the downturn was not as severe as expected and because the first stage of the recovery took place sooner and was stronger than expected (see Table 2-4).5 GDP and employment are projected to be higher and to be accompanied by modestly higher inflation and higher interest rates than they were in CBO’s July projections. The fact that the downturn was less severe and the recovery stronger than previously projected also changed the projected pattern of growth: CBO’s current projections of GDP growth are stronger, on average, for the 2021–2025 period than they were in July but weaker for the 2026–2031 period.

Table 2-4.

CBO’s Current and Previous Economic Projections for Calendar Years 2020 to 2030

Data sources: Congressional Budget Office; Bureau of Labor Statistics; Federal Reserve. See www.cbo.gov/publication/56970#data.

GDP = gross domestic product; PCE = personal consumption expenditures.

a. Real values are nominal values that have been adjusted to remove the effects of changes in prices.

b. Excludes prices for food and energy.

c. The consumer price index for all urban consumers.

d. The employment cost index for wages and salaries of workers in private industry.

e. Adjusted to remove distortions in depreciation allowances caused by tax rules and to exclude the effects of changes in prices on the value of inventories.

f. Estimated value for 2020.

CBO made those changes to its economic projections even though it expects social distancing to be more pronounced and to last longer than projected in July. The projected effects of the Consolidated Appropriations Act, 2021, played a part in improving the economic outlook.

1. As applied to GDP, the term “prepandemic” refers to its level in the fourth quarter of 2019; applied to employment, it refers to its level in February 2020.

2. The labor force is the number of people age 16 or older in the civilian noninstitutionalized population who have jobs or who are available for work and are actively seeking jobs.

3. See Congressional Budget Office, The Effects of Pandemic-Related Legislation on Output (September 2020), www.cbo.gov/publication/56537.

4. Those provisions are contained in divisions M, N, and EE of the Consolidated Appropriations Act, 2021.

5. For the July projections, see Congressional Budget Office, An Update to the Economic Outlook: 2020 to 2030 (July 2020), www.cbo.gov/publication/56442.

Appendix: Tax Expenditures

The tax rules that form the basis for the Congressional Budget Office’s projections include an array of exclusions, deductions, preferential rates, and credits. Those provisions reduce revenues for any given level of tax rates in both the individual and corporate income tax systems. Many of those provisions are called tax expenditures because, like government spending programs, they provide financial assistance for particular activities as well as to certain entities or groups of people.1

Tax expenditures contribute to the budget deficit just as federal spending does. They also influence people’s choices about working, saving, and investing, and they affect the distribution of income. The Congressional Budget and Impoundment Control Act of 1974 (Public Law 93-344) requires the federal budget to list tax expenditures and for CBO to report the levels of tax expenditures under existing law. Every year, the staff of the Joint Committee on Taxation (JCT) and the Treasury’s Office of Tax Analysis each publish estimates of individual and corporate income tax expenditures.2

Unlike many spending programs, tax expenditures are not subject to annual appropriations. In fact, most tax expenditures are not explicitly recorded in the federal budget but rather are reflected in the total amount of revenues. The one exception is the portion of refundable tax credits that exceeds a filer’s tax liability; that amount is recorded as mandatory spending in the budget. Because of that budgetary treatment, tax expenditures can be less transparent than discretionary spending or spending on benefit programs.

Tax expenditures have a large effect on the federal budget. In fiscal year 2021, the value of the more than 200 tax expenditures in the individual and corporate income tax systems will total an estimated $1.8 trillion—or 8.2 percent of gross domestic product—if their effects on payroll taxes as well as income taxes are included.3 That amount, which was calculated by CBO on the basis of estimates prepared by JCT, equals about half of all federal revenues that are projected to be collected in 2021 and exceeds all projected discretionary outlays combined (see Figure A-1).4

Figure A-1.

Outlays, Revenues, and Tax Expenditures in 2021

Percentage of Gross Domestic Product

Tax expenditures, which are projected to total an estimated $1.8 trillion in 2021, reduce revenues and, like spending programs, contribute to the deficit.

Data source: Congressional Budget Office, using estimates by the staff of the Joint Committee on Taxation. Those estimates were prepared before the enactment of the Consolidated Appropriations Act, 2021 (Public Law 116-260), and do not include the effects of that law. See www.cbo.gov/publication/56970#data.

a. The outlay portions of refundable tax credits are included in tax expenditures as well as mandatory outlays. In 2021, they are estimated to total 0.4 percent of gross domestic product (GDP). The additional recovery rebates for individuals enacted in P.L. 116-260 are included in mandatory outlays but not in the tax expenditure estimates presented here because the tax expenditures were estimated before the enactment of that law. Outlays for those additional rebates are estimated to total 0.7 percent of GDP in 2021.

b. This total is the sum of the estimates for all of the separate tax expenditures and does not account for interactions among them. However, CBO estimates that in 2021, the total of all tax expenditures roughly equals the sum of each considered separately. Because estimates of tax expenditures are based on people’s behavior with current provisions of the tax code in place, they do not reflect the amount of revenues that would be raised if those provisions were eliminated and taxpayers adjusted their activities in response.

Estimates of tax expenditures measure the difference between households’ and businesses’ tax liabilities under current law and the tax liabilities they would have incurred if the provisions generating those tax expenditures were repealed but taxpayers’ behavior was unchanged. Such estimates do not represent the amount of revenues that would be raised if those provisions were eliminated, because the changes in incentives that would result from eliminating those provisions would lead households and businesses to modify their behavior in ways that would lessen the effect on revenues.

1. Sec. 3(3) of the Congressional Budget and Impoundment Control Act of 1974, codified at 2 U.S.C. §622(3) (2006), defines tax expenditures as “those revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability.”

2. For this analysis, CBO followed JCT’s definition of tax expenditures as deviations from a “normal” income tax structure. For the individual income tax, that structure incorporates existing regular tax rates, the standard deduction, personal exemptions, and deductions of business expenses. For the corporate income tax, that structure includes the statutory tax rate, generally defines income on an accrual basis, and allows for cost recovery according to a specified depreciation system that is less favorable than under current law. For more information, see Joint Committee on Taxation, Estimates of Federal Tax Expenditures for Fiscal Years 2020–2024, JCX-23-20 (November 2020), www.jct.gov/publications/2020/jcx-23-20/. The Treasury’s definition of tax expenditures is broadly similar to JCT’s. See Office of Management and Budget, Budget of the U.S. Government, Fiscal Year 2021: Analytical Perspectives (February 2020), pp. 147–198, https://go.usa.gov/xscrh (PDF, 4.8 MB).

3. That total does not incorporate the recent changes to tax law made by the Consolidated Appropriations Act, 2021 (P.L. 116-260). JCT estimated that the law will reduce revenues and increase refundable tax credits by about $204 billion in 2021. That amount includes $166 billion for additional recovery rebates for individuals, which are considered tax expenditures, but like other refundable credits are recorded as mandatory spending in the budget. Unlike JCT, CBO includes estimates of the largest payroll tax expenditures. As defined by CBO, a normal payroll tax structure includes the existing payroll tax rates as applied to a broad definition of compensation—which consists of cash wages and fringe benefits. Tax expenditures that reduce the tax base for payroll taxes also decrease spending for Social Security by reducing the earnings base on which Social Security benefits are calculated.

4. For more information on the size of each tax expenditure, see Joint Committee on Taxation, Estimates of Federal Tax Expenditures for Fiscal Years 2020–2024, JCX-23-20 (November 2020), www.jct.gov/publications/2020/jcx-23-20/. For more information on the estimated budgetary effects of the tax provisions of P.L. 116-260, see Joint Committee on Taxation, Estimated Budget Effects of the Revenue Provisions Contained in Rules Committee Print 116-68, The “Consolidated Appropriations Act, 2021,” JCX-24-20 (December 2020), www.jct.gov/publications/2020/jcx-24-20/.

About This Document

This document is one of a series of reports on the state of the budget and the economy that the Congressional Budget Office issues each year. It satisfies the requirement in section 202(e) of the Congressional Budget Act of 1974 for CBO to submit to the Committees on the Budget periodic reports about fiscal policy and to provide baseline projections of the federal budget. In keeping with CBO’s mandate to provide objective, impartial analysis, this report makes no recommendations.

The estimates in this report are the work of more than 100 staff members at CBO and the staff of the Joint Committee on Taxation. Barry Blom wrote Chapter 1, and Aaron Feinstein, Avi Lerner, Amber Marcellino, and Dan Ready compiled the projections. Christina Hawley Anthony, Theresa Gullo, Leo Lex, John McClelland, Sam Papenfuss, and Joshua Shakin provided guidance. Robert Shackleton wrote Chapter 2, with contributions from Aaron Betz, Yiqun Gloria Chen, Erin Deal, Daniel Fried, Edward Gamber, Ronald Gecan, Mark Lasky, Junghoon Lee, Michael McGrane, Jaeger Nelson, Sarah Robinson, Jeffrey Schafer, John Seliski, and Christopher Williams. Robert Arnold, Devrim Demirel, John Kitchen, and Jeffrey Werling provided guidance. Kathleen Burke wrote the appendix; John McClelland and Joshua Shakin provided guidance. Erin Deal, Aaron Feinstein, Avi Lerner, Bayard Meiser, Tess Prendergast, Dan Ready, Sarah Robinson, and Olivia Yang fact-checked the report and prepared the supplemental material.

CBO consulted with members of its Panel of Economic Advisers during the preparation of this report. Although CBO’s outside advisers provided considerable assistance, they are not responsible for the contents of this report.

Mark Doms, Mark Hadley, Jeffrey Kling, and Robert Sunshine reviewed the report. Christine Bogusz and Benjamin Plotinsky were the editors, and Casey Labrack was the graphics editor. This report is available on CBO’s website (www.cbo.gov/publication/56970).

CBO continually seeks feedback to make its work as useful as possible. Please send any comments to communications@cbo.gov.

Phillip L. Swagel

Director

February 2021