Transitioning to Alternative Structures for Housing Finance: An Update

CBO analyzes four alternative structures for the secondary mortgage market, in which the government would play varying roles in guaranteeing mortgage-backed securities, and provides estimates of federal costs under each approach.

Summary

Policymakers are considering ways to restructure the housing finance system that could attract more private capital and could change the secondary (resale) market for mortgages. That market is dominated by Fannie Mae and Freddie Mac, two government-sponsored enterprises (GSEs) that have been under the control of the federal government since the financial crisis of 2008. Fannie Mae and Freddie Mac help finance the majority of home loans in the United States by purchasing and securitizing new mortgages. In the securitization process, mortgages are pooled into mortgage-backed securities (MBSs), which represent claims on the principal and interest payments that borrowers make on the loans in the pool. The GSEs guarantee those securities against most losses from defaults on the underlying loans and sell them to investors. CBO projects that under current policy, the GSEs will guarantee almost $12 trillion in new MBSs over the next 10 years and that those guarantees will cost the government about $19 billion.

Alternative proposals for the secondary mortgage market involve different choices about whether the federal government should continue to guarantee payment on certain types of mortgage-backed securities—and if so, what the scope, structure, and pricing of those guarantees should be. Policymakers also face choices about how the secondary market should be structured. For example, should it be organized around a single federal agency, a limited number of highly regulated private firms, or many private firms?

This report updates a 2014 study by CBO that analyzed various broad approaches for the future of the secondary mortgage market. This report considers the same alternative market structures as the 2014 study, but CBO’s illustrative transition paths to those structures are now only half as long because of improvements in the mortgage and housing markets since 2014. In addition, unlike the previous study, this report provides estimates of federal costs under the new approaches as well as under the transitions to them.

Which Illustrative Structures for the Secondary Market Did CBO Consider, and What Would a Transition to Them Involve?

For this analysis, CBO created illustrative transition paths that, between 2019 and 2023, would move the secondary mortgage market from dominance by Fannie Mae and Freddie Mac to one of four alternative structures:

- A secondary market in which a single, fully federal agency would guarantee qualifying MBSs. That approach would leave taxpayers exposed to much of the securities’ credit risk (the net losses incurred when borrowers default on their mortgages); they would also benefit from the revenues that those securities provide. Because no significant amount of new private capital would be required, the transition from the two GSEs to a fully federal agency could be accomplished without changing the structure of the guarantees, raising the guarantee fees that the GSEs charge, or altering the current limits on the size of mortgages that the GSEs are allowed to guarantee.

- A hybrid public-private market in which the government and several private guarantors would share the credit risk on eligible MBSs. In that approach, private guarantors would bear most of the losses on MBSs in normal economic times, but the federal government would share more of those losses in a financial crisis. Policymakers would need to make some critical design choices about the structure of a public-private system and the capital requirements for private guarantors. During the transition to that system, the main change would be that the GSEs would share more of the credit risk on their mortgages with private investors.

- A secondary market in which the government would play a very small role during normal times but would act as the “guarantor of last resort” during a financial crisis by fully guaranteeing most new mortgages issued during the crisis (absorbing all losses and gains on the securities backed by those mortgages, which it would not do in the hybrid market). Compared with the hybrid structure, under this arrangement the government would bear less risk on mortgages issued in normal times and more risk on mortgages issued in periods of financial crisis. The key policy change during the transition to that system would be the use of auctions to allocate limited amounts of federal guarantees.

- A largely private model in which there would be no federal guarantees in the secondary mortgage market (beyond those currently provided by the Government National Mortgage Association, or Ginnie Mae). During the transition to such a structure, policymakers could begin attracting more private capital to the secondary market by raising Fannie Mae’s and Freddie Mac’s guarantee fees and lowering the size limits on mortgages they can guarantee.

How Would the New Illustrative Structures Affect the Government’s Exposure to Credit Risk and Estimated Costs?

CBO currently views Fannie Mae and Freddie Mac as fully federal agencies because they are controlled and mostly owned by the government. Therefore, if lawmakers opted for a market structure with a single, fully federal agency and kept the existing pricing policies for federal mortgage guarantees, the government’s exposure to credit risk would essentially remain the same. As a result, estimates of federal subsidy costs for those guarantees would not change much (when measured using the budgetary approach that CBO employs for the two GSEs).

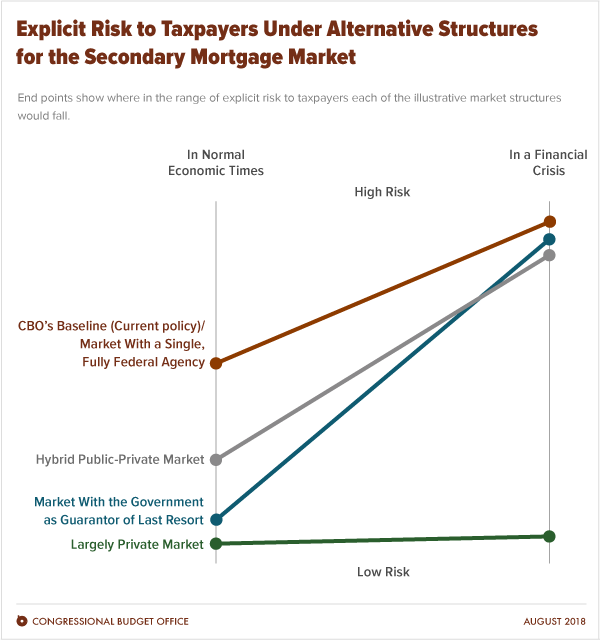

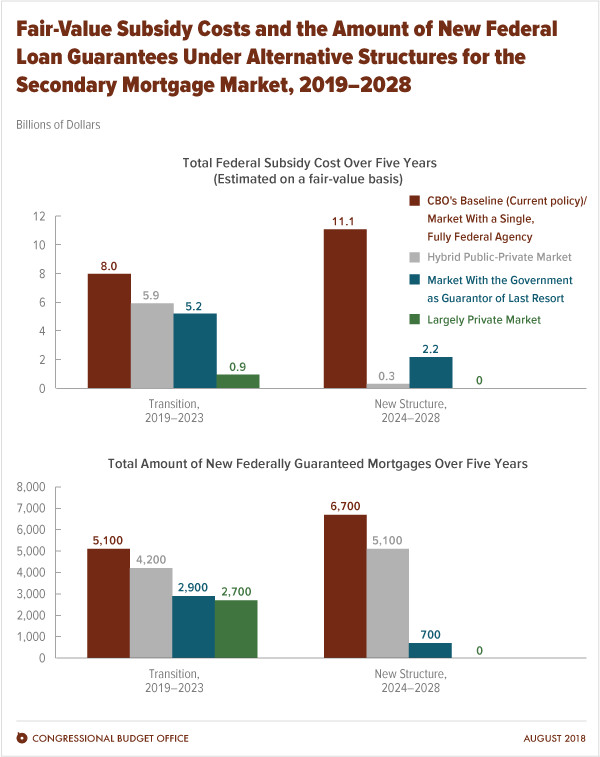

New market structures that emphasized private capital would significantly reduce federal costs, compared with current policy, and would decrease the government’s risk exposure by having private guarantors and investors bear more of the risk of losses from defaults (see figure below). CBO’s estimates of federal subsidy costs and of the amount of new federally guaranteed mortgages decline as more private capital enters the secondary market under those illustrative structures (see figure below). However, mortgage borrowers would face slightly higher interest rates under those approaches.

In a hybrid public-private market or a market with the government as guarantor of last resort, the government’s risk exposure would be reduced not only by the addition of private guarantors and investors but also by the reduction in the volume of federal loan guarantees. During normal economic times, explicit credit risk to the government would be much lower under a hybrid public-private system than under current policy, would be nearly eliminated if the government served as guarantor of last resort, and would be eliminated under a largely private system.

During a severe financial crisis, by contrast, the government would probably bear most of the risks and costs of new guarantees under all of the structures except a largely private market—as it would under current policy. On guarantees issued before a crisis, however, the government’s exposure to losses would be greater under the fully federal approach than under either a hybrid market or a market with the government as guarantor of last resort.

Under a largely private approach, the government would bear no explicit risk. But in a crisis, the government might ultimately be expected to step in to guarantee privately issued MBSs and prevent the supply of private financing from drying up, resulting in costs to taxpayers. Such an implicit federal guarantee would be free for private issuers of MBSs, allowing them to pay lower interest rates on their securities.

How Would the New Illustrative Structures Affect Mortgage Borrowers, the Housing Market, and the Federal Housing Administration?

The effects of new structures for the secondary mortgage market would depend on the extent of the decline in federal subsidies, the degree of the market’s reliance on the private sector, and the speed of the transition.

- During normal economic times, most mortgage borrowers would face somewhat higher interest rates under the structures that attracted more private capital, CBO estimates (because the GSEs’ current guarantee fees are probably a bit lower than the prices that CBO judges private firms would charge). Home prices, however, are not particularly sensitive to small increases in interest rates, so the downward pressure on home prices from those increases would probably be modest. Under the fully federal approach, by contrast, mortgage interest rates would probably decline slightly, and home prices might edge up a bit.

- During a financial crisis, borrowers could face significant constraints on the availability of mortgages and higher interest rates under the largely private market (but not under the other three approaches) if the government did not step in to guarantee privately issued MBSs. The resulting downward pressure on home prices could be significant.

- Under the approaches that would raise the cost or otherwise limit the volume of guarantees by a new federal entity, some borrowers would shift to mortgages insured by the Federal Housing Administration (FHA) or other government agencies. The government’s exposure to credit risk would not change. But because the government generally collects higher fees on FHA-backed loans than the GSEs do on their guarantees, if everything else remained the same, such a switch would reduce federal costs.