Options for Changing the Retirement System for Federal Civilian Workers

CBO analyzes the impact of retirement benefits on the federal budget and on the compensation, recruitment, and retention of its employees. It assesses the short-term and long-term effects of potential changes to those benefits.

Summary

The federal government employs about 2.7 million civilian workers—1.8 percent of the U.S. workforce. Like many employers, the federal government compensates its employees with salaries, wages, and other benefits that are paid as they are earned, as well as deferred compensation in the form of retirement benefits. Lawmakers have expressed interest in examining the current structure of retirement benefits to ensure that the government provides adequate compensation to attract and retain skilled employees while not paying more than needed to accomplish that goal. Therefore, this report analyzes several potential changes to the federal retirement system and their impact on the federal budget over 75 years.

What Retirement Systems Does the Federal Government Operate for Its Civilian Employees?

The federal government currently provides its civilian employees with pensions under two different systems: The Civil Service Retirement System (CSRS), which is phasing out and has been closed to new participants since 1983, and the Federal Employees Retirement System (FERS), in which almost all current workers participate. In addition, it operates the Thrift Savings Plan (TSP), a defined contribution plan for federal civilian employees. The TSP is similar to 401(k) accounts, which are common in the private sector. (The federal government also provides health care to retirees through the Federal Employees Health Benefits, or FEHB, program and operates a few other smaller retirement programs, though those are not the focus of this report.)

How Much Does the Federal Government Spend on Its Retirement Systems?

In 2016, the federal government spent $91 billion on retirement benefits for most of its civilian employees: $70 billion for CSRS pensions for civilian retirees and their survivors; $13 billion for FERS pensions for civilian retirees and their survivors; and $8 billion for contributions to TSP. Those expenditures were partially offset by $3 billion in revenues from employees’ contributions to the CSRS and FERS pension plans.

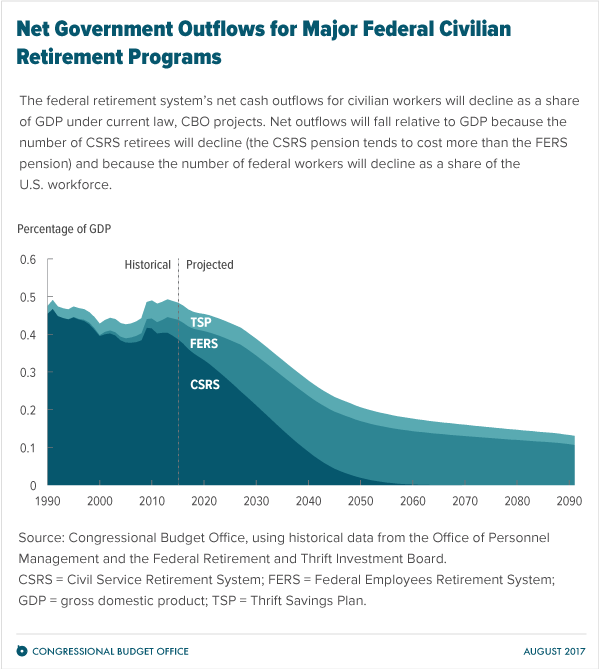

Under current law, the government’s net cash outflows for the federal civilian retirement system (that is, the system’s outlays minus its revenues) are projected to grow by an average of about 2.8 percent annually between 2018 and 2027. Over a longer time horizon—75 years—they would decline sharply as a share of gross domestic product (GDP)—from 0.48 percent of GDP in 2016 to 0.13 percent of GDP in 2091, CBO projects. Also, the composition of that spending would change. By the 2060s, CSRS would be almost completely phased out. Almost all spending would be on the pensions provided through FERS and on contributions to TSP (see figure below).

How Does FERS Affect Current Pay and Retirement Income?

The structure of FERS affects federal workers’ current pay as well as their retirement income—the amount of income they will receive from the pension and from their TSP accounts. For the purposes of this report, “current pay” is defined as the worker’s salary or other cash compensation minus the amount of the contributions he or she is statutorily required to make to the pension plan and voluntarily makes to TSP. Workers hired in 2018 who will eventually receive a pension will contribute 12 percent of their salary, on average, to the pension plan and TSP, CBO projects. The federal government will contribute an amount equal to 15.5 percent of those workers’ salaries for those purposes, CBO projects.

The amount of income from the pension depends on a worker’s age, years of service at retirement, and earnings history, whereas income from a TSP account depends on the employer’s and the employee’s contributions and the employee’s investment decisions. For workers with the same number of years of federal service, the replacement rate—retirement income as a share of preretirement earnings—is generally higher for workers who join the government at older ages than for workers who join at younger ages. Moreover, for workers who join at older ages, a larger share of retirement income will come from the pension than from TSP.

How Does FERS Affect Recruitment and Retention?

The effect FERS has on recruitment depends on the career plans of the workers whom agencies want to hire. Because the value of the pension grows with the number of years of service, the pension attracts workers who anticipate a long career in the federal government but not workers who do not expect to remain in federal service for a long time. In contrast, TSP probably enhances recruitment among a broader group of workers because employees are eligible for federal contributions of up to 5 percent of their salary regardless of their age and tenure.

The pension and TSP also affect the retention of federal workers differently. For midcareer employees, the pension benefit provides an incentive to stay in government in order to qualify for a larger pension. By contrast, that incentive is limited for workers who are early in their careers because they will have to work for the government many more years before they retire. For workers who are eligible to retire with a full pension, working for an additional year would mean forgoing pension payments for that year, so for them, the plan may serve as a disincentive to stay. TSP probably provides an incentive to stay in government at most points in a career because the value of the benefit does not depend on how long the worker has been employed or how far from retirement he or she is.

What Are Some Options to Change FERS?

To explore how changing FERS would affect spending in the long term, CBO assessed two types of options (see table below). One type would modify the pension plan either by changing employees’ contributions to the plan or by changing the formula used to calculate benefits. The other type would replace the pension for new employees with larger contributions from the government to employees’ TSP accounts—a change that would be similar to the shift during recent decades from defined benefit to defined contribution retirement plans in many private-sector companies and some state governments. The options CBO analyzes in those categories are illustrative; other options could be designed to be more or less costly to the government.

CBO estimated the net costs of the options on both a cash basis and on an accrual basis. On a cash basis, federal outlays (pension payments and the government’s contributions to TSP) and revenues (employees’ contributions to the pension plan) are recorded at the time when those transactions occur. For pension payments, those transactions can be many years after the obligation to make those payments was incurred. On a cash basis, CBO measured net federal outflows in nominal terms over the next 10 years and in present-value terms over the 75-year projection period. By contrast, when measuring net costs on an accrual basis, CBO approximated the percentage of workers’ salaries that the government would need to set aside each year to fully fund those workers’ benefits. For illustrative purposes, CBO compared the cash and accrual costs for federal employees who would be hired in 2018.

Change the FERS Pension Plan. Three options would change the terms of the FERS pension:

- Option 1. Increase the pension contribution to 4.4 percent of salary for all employees. (Currently that rate is 0.8 percent for employees hired before 2013 and 3.1 percent for employees hired in 2013. It is already 4.4 percent for employees hired after 2013.)

- Option 2. Decrease the pension contribution rate to 0.8 percent for all employees.

- Option 3. Decrease pensions by basing the retirement benefit on the five years of highest salary (instead of the three years of highest salary, as in current law).

Option 1 would reduce the federal government’s net costs for retirement for employees enrolled in FERS by 14 percent on a cash basis over the next 10 years, and by 3 percent on a present-value basis over the 75-year projection period. Because the option would affect only current workers hired in 2013 or earlier, the government’s savings would gradually decline as those workers retire or leave government. For the same reason, retirement costs for new federal employees would remain unchanged on an accrual basis. Correspondingly, CBO expects that the federal government’s ability to recruit new employees would be unaffected. However, the option would increase the number of employees who chose to leave federal service because their current pay would be reduced. The most experienced and highly qualified employees would be those most likely to leave.

Option 2 would increase the government’s net retirement costs for employees enrolled in FERS by 10 percent on a cash basis over the next 10 years, and by 13 percent over the 75-year period. On an accrual basis, the option would increase retirement costs for new employees by 22 percent. However, this option would enable the government to recruit and retain a more highly qualified workforce by increasing both current pay and the value of the pension plan (net of the employees’ contributions) for workers who were hired recently as well as those who will be hired in the future.

Option 3 would reduce the government’s net retirement costs for employees enrolled in FERS by 1 percent on a cash basis over the next 10 years, and by 3 percent over the 75-year period. The option would reduce costs by 4 percent on an accrual basis for new employees. CBO expects a small decrease in the recruitment and retention of highly qualified workers because the reduction in the pension is relatively small and because changes in retirement benefits would have less effect than would a similar change in current pay.

Replace the FERS Pension With Larger Government Contributions to TSP for New Employees. Two options would eliminate the FERS pension for new employees and replace it with larger TSP contributions. On a cash basis, such options would impose costs in the near term because they would require larger outlays at the time the benefit is earned, but costs would be lower in the future, when employees affected by the options retired.

- Option 4. Eliminate the FERS pension, increase the government’s automatic TSP contribution to 8 percent of salary, and require the government to match up to 7 percent of additional contributions for new employees.

- Option 5. Eliminate the FERS pension, increase the government’s automatic TSP contribution to 10 percent of salary, and eliminate the government’s matching contribution to TSP.

Option 4 would increase the government’s net retirement costs for employees enrolled in FERS on a cash basis by 24 percent over the next 10 years and by 10 percent over the 75-year period. However, the net cash cost of this option would be lower than the cost under current law if the analysis was projected over a sufficiently long period to incorporate the full savings from reduced future liabilities. On an accrual basis, net retirement costs for new federal employees would be about 6 percent lower than costs under current law. The option would probably increase the recruitment and retention of early-career and retirement-eligible employees, though it would reduce the retention of midcareer employees.

Option 5 would increase the government’s net retirement costs for employees enrolled in FERS on a cash basis by 17 percent over the next 10 years and reduce them by about 3 percent over the 75-year period. On an accrual basis, the option would reduce costs by 29 percent for new federal employees. The effect of the option on recruitment is uncertain. CBO expects that the option would increase retention of early-career and retirement-eligible employees, but by less than Option 4.