Revisions to CBO's Projection of Potential Output Since 2007

CBO examines the change in its projections of potential output for the year 2017: The estimate for that year that CBO prepared in February 2014 is about 7 percent lower than what it projected in January 2007.

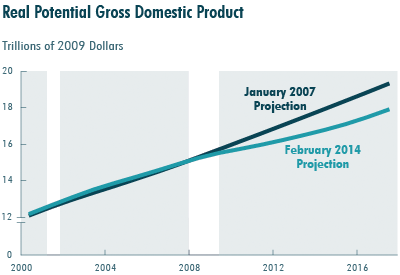

Summary

As part of its economic and budgetary projections, CBO estimates past and future potential output—also called potential gross domestic product (GDP), and defined as the maximum sustainable amount of real (inflation-adjusted) output that the economy can produce. For various reasons, CBO’s projections for potential GDP in a specific year can change over time. This report examines a change in CBO’s projections of potential output for the year 2017, comparing the projection it published in January 2007 with the one it released in February 2014. From the earlier projection to the more recent, CBO’s projection for potential output in 2017 declined by 7.3 percent (see the figure below).

How Does CBO Use Estimates of Potential Output?

CBO uses potential output to guide its projection of actual output. CBO’s projections of economic activity in the later years of the standard 10-year projection periods are based not on forecasts of cyclical fluctuations in the economy but on the assumption that actual output will gradually approach potential output. For example, in The Budget and Economic Outlook: 2014 to 2024, CBO projects that actual economic output will return to its historical relationship with potential output in 2017 and later years. Because of the central role that projections of potential output play in forming the baseline projections of economic activity and income, projections of potential output also play a critical role in CBO’s baseline projections of federal revenue and spending.

How Does CBO Estimate Potential Output?

CBO makes its estimates of potential output on the basis of data on capital, labor, productivity, and actual GDP; statistical and other modeling methods for assessing cyclical influences and long-term trends in the economy; and analyses of the economic effects of federal tax and spending policies. In general, CBO’s projections for 10 year periods are based on its estimates of economic trends during the most recent full business cycle and in the as-yet-incomplete, current cycle. CBO’s projections also incorporate predictions of the effects of federal tax and spending policies embodied in current law.

Why Has CBO Revised Its Projection of Potential Output?

CBO revises projections of potential output with each semiannual economic forecast to take into consideration changes in current law, revised and new data, and new analysis and improvements in its methods of estimation. To assess the role of the most recent recession in those revisions, this report focuses on the change between the projections that CBO published in January 2007 and in February 2014 for 2017, the last projection year they had in common. From the earlier projection to the later one, CBO reduced by 7.3 percent the amount it projects for potential GDP in 2017. That calculation excludes changes in CBO’s projection that arise from the recent revisions (described below) to the definition of GDP by the Commerce Department’s Bureau of Economic Analysis (BEA).

Four main sources account for that 7.3 percent reduction, in CBO’s judgment, of its projection of potential GDP for 2017 (see the table below):

- The impact of cyclical weakness in the economy accounts for just 1.8 percentage points, or about one fourth, of the difference from the 2007 projection, even though the downward revision to potential GDP coincided with the severe recession of 2007–2009 and the subsequent slow recovery.

- Reassessments of economic trends that were in process before the recession began account for 4.8 percentage points, or about two-thirds, of the revision. For example, after the National Bureau of Economic Research designated the fourth quarter of 2007 as a business cycle peak, CBO concluded that trend rates of growth in the 2000s had generally been lower than they were in the 1990s.

- Revisions to historical data for the period before the recent recession lowered the projection of potential output by 0.1 percentage points, a very small share of the revision.

- The effects of changes in federal tax and spending policies, higher federal deficits, changes in the relative size of various sectors of the economy, and other factors after 2007 apart from cyclical conditions account for the remaining 0.7 percentage-point reduction, or about one-tenth of the revision.

| Contributions to the Revision of CBO's Projection of Potential Output for 2017 Between 2007 and 2014 | |||||||

| (In percentage points) | Recession and Weak Recovery | Reassessment of Trends | Revisions to Prerecession Data | Fiscal Policy and Other Factors | All Sources | ||

| Nonfarm Business Sector | |||||||

| Potential labor hours | -0.7 | -3.0 | -0.3 | 1.2 | -2.7 | ||

| Capital services | -0.6 | -0.7 | 0.2 | -1.3 | -2.4 | ||

| Potential total factor productivity | -0.5 | -0.7 | -0.6 | 0.4 | -1.4 | ||

| Other Sectors | n.a. | -0.3 | 0.7 | -1.0 | -0.7 | ||

| Total (Percent) | -1.8 | -4.8 | -0.1 | -0.7 | -7.3 | ||

| Note: The contributions to the revision reported in the table exclude changes in CBO’s projection that are the result of the revised definition of gross domestic product presented in the comprehensive revision to the national income and product accounts released by the Bureau of Economic Analysis in July 2013. | |||||||

Most of the total downward adjustment in potential GDP is in the nonfarm business sector; other sectors of the economy account for smaller portions.

This accounting of the sources of the revision is rough and subject to considerable uncertainty. In particular, because the factors that affect potential GDP interact with one another in complex ways, it is difficult to separate their various effects. For example, CBO estimates that increases in federal spending and decreases in federal tax revenues that led to the surge in federal debt over the period from 2007 to 2014 moderated the negative effects of the weak economy on potential GDP. In this analysis, however, that increase in debt is counted solely as having led to a reduction in capital investment and hence to a reduction in the growth of services from capital assets such as equipment, structures, inventories, and land.

How Did CBO Account for Revisions to the National Income and Product Accounts?

CBO’s current projections incorporate data from the comprehensive revision to the national income and product accounts released by BEA in July 2013. That revision expanded the definition of GDP, raising its values relative to those used by CBO in 2007. The most notable change was in the measure of investment, which now includes new categories for intellectual property products and an expanded set of ownership transfer costs for home purchases. Overall, BEA raised its estimates of nominal GDP in each year between 1950 and 2012 by an average of about 3.2 percent. In addition, BEA’s revision changed the reference year for prices and real output: BEA now reports prices in each year relative to prices in 2009, and real output is reported in 2009 dollars; previously, BEA had used 2005 as its reference year.

To account for the revision to the measure of real output and to facilitate comparisons between its current and previous estimates of potential output, CBO adjusted the earlier projections presented in this analysis in two ways. First, to account roughly for the change in the definition of GDP—to put GDP in the previous and latest projections on a consistent basis—CBO adjusted its previous projections of nominal output upward by about 3.2 percent for all years. Second, CBO adjusted the reference year for the calculation of inflation-adjusted values in its previous projections to 2009, so that earlier projections of real potential output are presented here in 2009 dollars.