The 2013 Long-Term Projections for Social Security: Additional Information

Spending on the Social Security program will exceed its dedicated tax revenues, on average, by about 12 percent over the next decade, CBO projects. The gap will grow larger in the 2020s and will exceed 30 percent of revenues by 2030.

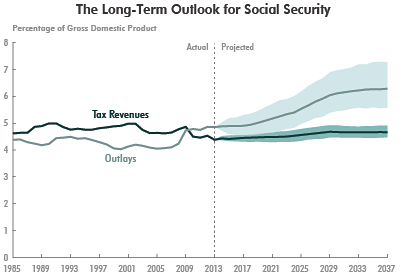

Summary

Social Security is the federal government’s largest single program. Of the 58 million people who currently receive Social Security benefits, about 70 percent are retired workers or their spouses and children, and another 11 percent are survivors of deceased workers; all of those beneficiaries receive payments through Old-Age and Survivors Insurance (OASI). The other 19 percent of beneficiaries are disabled workers or their spouses and children; they receive Disability Insurance (DI) benefits.

In fiscal year 2013, Social Security’s outlays totaled $808 billion, almost one-quarter of federal spending; OASI payments accounted for about 83 percent of those outlays, and DI payments made up about 17 percent. Each year, CBO prepares long-term projections of revenues and outlays for the program. The most recent set of 75-year projections was published in September 2013. This publication (shown below) presents additional information about those projections.

Social Security has two primary sources of tax revenues: payroll taxes and income taxes on benefits. Roughly 96 percent of those revenues derive from a payroll tax—generally, 12.4 percent of earnings—that is split evenly between workers and their employers; self-employed people pay the entire tax. The payroll tax applies only to taxable earnings—earnings up to a maximum annual amount ($113,700 in 2013). The remaining share of tax revenues—4 percent—is collected from income taxes that higher-income beneficiaries pay on their benefits. Revenues credited to the program totaled $745 billion in fiscal year 2013.

Revenues from taxes, along with intra-governmental interest payments, are credited to Social Security’s two trust funds—one for OASI and one for DI—and the program’s benefits and administrative costs are paid from those funds. Although legally separate, the funds often are described collectively as the OASDI trust funds. In a given year, the sum of receipts to a fund along with the interest that is credited on balances, minus spending for benefits and administrative costs, constitutes that fund’s surplus or deficit.

In calendar year 2010, for the first time since the enactment of the Social Security Amendments of 1983, annual outlays for the program exceeded annual tax revenues (that is, outlays exceeded total revenues excluding interest credited to the trust funds). In 2012, outlays exceeded noninterest income by about 7 percent, and CBO projects that the gap will average about 12 percent of tax revenues over the next decade. As more members of the baby-boom generation retire, outlays will increase relative to the size of the economy, whereas tax revenues will remain at an almost constant share of the economy. As a result, the gap will grow larger in the 2020s and will exceed 30 percent of revenues by 2030.

CBO projects that under current law, the DI trust fund will be exhausted in fiscal year 2017, and the OASI trust fund will be exhausted in 2033. If a trust fund’s balance fell to zero and current revenues were insufficient to cover the benefits specified in law, the Social Security Administration would no longer have legal authority to pay full benefits when they were due. In 1994, legislation redirected revenues from the OASI trust fund to prevent the imminent exhaustion of the DI trust fund. In part because of that experience, it is a common analytical convention to consider the DI and OASI trust funds as combined. Thus, CBO projects, if some future legislation shifted resources from the OASI trust fund to the DI trust fund, the combined OASDI trust funds would be exhausted in 2031.

The amount of Social Security taxes paid by various groups of people differs, as do the benefits that different groups receive. For example, people with higher earnings pay more in Social Security payroll taxes than do lower-earning participants, and they also receive benefits that are larger (although not proportionately so). Because Social Security’s benefit formula is progressive, replacement rates—annual benefits as a percentage of average annual lifetime earnings—are lower, on average, for workers who have had higher earnings. As another example, the amount of taxes paid and benefits received will be greater for people who were born more recently because they typically will have higher earnings over a lifetime, even after an adjustment for inflation, CBO projects.

Scheduled and Payable Benefits

CBO prepares two types of benefit projections. Benefits as calculated under the Social Security Act, regardless of the balances in the trust funds, are called scheduled benefits. However, if the trust funds were depleted, the Social Security Administration would no longer have legal authority to pay full benefits when they were due. If that were to occur, annual outlays would be limited to annual revenues in the years after the exhaustion of the trust funds. Benefits thus reduced are called payable benefits. In such a case, all receipts to the trust funds would be used, and the trust fund balances would remain essentially at zero. When presenting projections of Social Security’s finances, CBO generally focuses on scheduled benefits because, by definition, the system would be fully financed if payable benefits were all that was disbursed.

Quantifying Uncertainty

To quantify the uncertainty in its Social Security projections, CBO, using its long-term model, created a distribution of outcomes from 500 simulations. In those simulations, the values for most of the key demographic and economic factors that underlie the analysis—for example, fertility and mortality rates, interest rates, and the rate of growth of productivity—were based on historical patterns of variation. Several exhibits in this publication show the simulations’ 80 percent range of uncertainty: That is, in 80 percent of the 500 simulations, the value in question fell within the range shown; in 10 percent of the simulations, the value was above that range; and in 10 percent, it was below.

Long-term projections are necessarily uncertain, and that uncertainty is illustrated in this publication; nevertheless, under a variety of values for key factors, the general conclusions of this analysis are unchanged. In contrast to previous reports, the uncertainty analysis in this year’s report focuses on the next 25 years. Beyond that period, the projected ratio of debt held by the public to gross domestic product (GDP) is well outside historical experience in a significant share of simulations. Projections of economic outcomes under those circumstances are unreliable, precluding analysis of the uncertainty of those outcomes.

Changes in CBO’s Long-Term Social Security Projections Since 2012

The shortfalls for Social Security that CBO is currently projecting are larger than those the agency projected a year ago.

Spending and Revenues Measured Relative to Taxable Payroll

The 75-year imbalance has increased from 1.95 percent to 3.36 percent of taxable payroll. The higher projection results from a number of factors, including increases in projections of life expectancy and of the disability incidence rate, both of which raise projected outlays for benefits, and decreases in the projection of income taxes on benefits. This year, rather than using the Social Security trustees’ projections of life expectancy (as done for earlier analyses), CBO used its own, which incorporate faster growth of that measure than the Social Security trustees anticipate. In addition, CBO increased its projection of the share of workers who will receive Social Security disability benefits, resulting in higher projected spending for Social Security. Of the 1.4 percentage-point increase in the 75 year imbalance, a higher projection of life expectancy accounts for 0.6 percentage points, a higher projection of the disability incidence rate accounts for 0.1 percentage point, reductions in income tax rates enacted in January 2013 (which reduce the revenues for Social Security from income taxes on benefits) account for 0.4 percentage points, and other factors (including a projection period that extends a year later and updated data) account for 0.4 percentage points.

When measured as a share of taxable payroll, long-term tax revenues are lower than those that CBO projected in 2012, but long-term outlays are higher. Compared with last year’s projection, the 75-year income rate—a measure of Social Security’s tax revenues—is 0.3 percentage points lower because revenues from income taxes on benefits are now projected to be lower as a result of the American Taxpayer Relief Act of 2012. The 75 year cost rate—a measure of outlays—is 1.1 percentage points higher. Outlays are a higher share of taxable payroll because of the increases in projections of life expectancy and the incidence of disability.

Spending and Revenues Measured Relative to GDP

When measured as a share of GDP, the projection of the income rate is slightly lower than it was in last year’s report. CBO reduced its projection of how much a new excise tax on some employment-based health insurance plans with premiums above a certain threshold will affect the mix of compensation that employees receive, resulting in a lower projection of taxable earnings. That reduction in taxable earnings was partly offset by a lower projection of growth in health care costs, which implies that a larger share of compensation will be paid as taxable earnings, rather than nontaxable health benefits. As a result of those partially offsetting changes, CBO projects that taxable earnings will make up a smaller share of compensation than the amount estimated last year. Together with the reductions in income tax rates, those changes imply that the income rate will be slightly lower than the level estimated last year.

The current projection of Social Security spending as a percentage of GDP is lower than last year’s projection through 2028—for much of that period, almost entirely because of revisions to GDP. For years after 2028, Social Security spending as a percentage of GDP is higher than or equal to the amounts CBO projected last year, and the difference is greater if the amounts projected in last year’s report are adjusted to incorporate revised values for GDP. The higher projection results from the same factors that increase costs as a share of taxable payroll, including increases in projections of life expectancy and the disability incidence rate.

The 75-year imbalance is greater as a share of GDP for the same reasons that it is greater as a share of taxable payroll. The imbalance rose from 0.73 percent of GDP to 1.17 percent.