Policy Options for the Social Security Disability Insurance Program

The Disability Insurance program provided benefits to 8.3 million disabled workers in 2011. By 2022, CBO projects, the program will provide benefits to over 10 million disabled workers and spending on benefits will exceed $190 billion.

Summary

The Social Security Disability Insurance (DI) program pays cash benefits to nonelderly adults (those younger than age 66) who are judged to be unable to perform “substantial” work because of a disability but who have worked in the past; the program also pays benefits to some of those adults’ dependents.

The Number of DI Beneficiaries Has Increased Nearly Sixfold Since 1970

In 2011, the DI program provided benefits to 8.3 million disabled workers, nearly six times the 1.4 million disabled workers who received benefits in 1970. Including the dependent spouses and children of those workers further increases the number of people receiving support from the program in 2011 to 10.3 million. The growth in the program can be attributed to changes in multiple factors, including demographics, the labor force, federal policy, opportunities for work, and compensation (earnings and benefits) during employment.

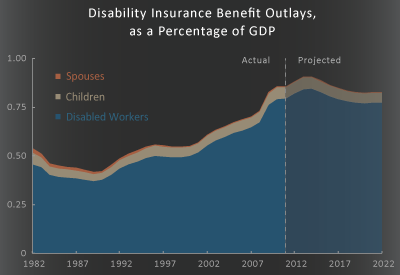

DI Program Outlays Have Outpaced Dedicated Revenues and That Trend Will Continue in the Future, CBO Estimates

Over the past 40 years, outlays for benefits from the DI program (adjusted for inflation) have grown by more than nine times. During that period, the average benefit received by disabled workers rose from about $560 per month to about $1,050 per month in 2010 dollars. (Other programs also support workers with disabilities.)

Since 2009, the program has paid out more each year in benefits than it received in dedicated revenues. In 2011, total benefit outlays for DI were $128 billion, or 0.86 percent of gross domestic product (GDP); by contrast, the program’s revenues totaled about $94 billion, or 0.63 percent of GDP. In 2022, the program’s spending and revenues will be roughly the same shares of economic output as in 2011, according to CBO’s estimates. By 2037, revenues as a percentage of GDP will be little changed, but spending as a share of output will have fallen slightly, as the proportion of the working-age population that is age 50 or older (and thus more likely to receive DI benefits) declines.

There Are Several Possible Approaches to Changing the DI Program

CBO and the staff of the Joint Committee on Taxation (JCT) have estimated the budgetary effects of a variety of potential modifications to the DI program. Restoring the DI program to a sound budgetary position would require combinations of the policies discussed below or other changes to the program.

Two policy options that would alter the taxes that support the program—shown in the top of the graphic—would result in higher revenues of $13 billion or $28 billion in 2022 in CBO’s and JCT’s estimation.

Seven policy options—shown in the middle of the graphic—that would modify benefits could lead to declines in the rate of growth of the number of participants in the program and to cuts in the program’s spending relative to CBO’s estimates based on current law. For those options, cuts would range between about $1 billion and about $22 billion in 2022 according to CBO’s estimates.

In addition, CBO estimated the longer-run effects of each option. Relative to the agency’s estimates under current law for 2037, the two revenue options would increase DI tax receipts by 8 percent or 22 percent, and the seven spending options would reduce DI outlays by between 2 percent and 14 percent.

Alternatively, lawmakers could choose to modify the DI program in ways that would provide greater support to certain DI beneficiaries and increase spending for the program (see the bottom panel of the graphic). CBO examined two policy options of that sort. Those options would increase DI outlays by $8 billion or $16 billion in 2022 and by 5 percent or 6 percent in 2037.

Policymakers could also alter the DI program in more fundamental ways. Modifications might include promoting disabled beneficiaries’ return to work—for example, by moving to a partial disability system that related benefits to the degree of disability. Various European nations have experimented with such modifications, but the changes in policy that those countries have instituted generally have been in place for such a short time that their fiscal impact is uncertain. Overall, CBO concludes, such fundamental changes might help move the United States’ DI program toward budgetary balance in the long run but are unlikely to provide sufficient immediate cost savings to resolve the program’s near-term financial pressures.