At a Glance

The Department of Veterans Affairs (VA) plays an important role in financing housing for eligible veterans and others by guaranteeing that originating lenders will be partially protected from losses if borrowers do not repay their mortgages in full. Since the Congress authorized VA to guarantee mortgages in 1944, the program has backed more than 25 million loans.

The annual dollar volume of VA’s loan guarantees began to increase in 2000 before reaching a peak in 2003 and then declining through 2007. Since the financial crisis of the late 2000s, VA’s guarantees have generally increased both in dollar volume and as a share of total federal loan guarantees. Fiscal year 2020 was a record year for VA, with guarantees totaling more than $375 billion and accounting for 12 percent of all single-family home mortgages issued that year.

This report by the Congressional Budget Office describes VA’s mortgage guarantee program, including eligibility and underwriting criteria, the structure of the guarantees, and the volume and characteristics of borrowers who obtain such guarantees. The report also describes CBO’s estimates of the budgetary costs of the program and compares those costs with expenditures for other federal guarantees.

CBO’s findings are as follows:

- Under the accounting rules used in the federal budget (as specified in the Federal Credit Reform Act of 1990, or FCRA), the guarantees of $268 billion in new mortgages that VA is projected to issue in fiscal year 2022 would increase the budget deficit by about $2.8 billion.

- Subsidies that reduce fees for VA’s borrowers are the primary driver of those budgetary costs. Such fees are lower, on average, than those for mortgages guaranteed by the Federal Housing Administration, Fannie Mae, and Freddie Mac. When compared with the other three mortgage guarantee programs, VA’s is the only one that has net budgetary costs on a FCRA basis.

- Under fair-value accounting—in which estimates of costs are based on the market value of the government’s obligations—that 2022 cohort of VA guarantees would increase the deficit by $9.7 billion.

Notes

Notes

Results are based on the Congressional Budget Office’s July 2021 baseline budget projections.

Unless this report indicates otherwise, all years referred to are federal fiscal years, which run from October 1 to September 30 and are designated by the calendar year in which they end.

Numbers in the text, table, and figures may not add up to totals because of rounding. Dollar values are expressed in nominal amounts.

Summary

The mortgage guarantee program administered by the Department of Veterans Affairs (VA) is designed to help eligible veterans, service members, surviving spouses, and members of the reserves or National Guard obtain a mortgage to purchase a home or refinance an existing mortgage. VA accomplishes that goal by providing a guarantee against some losses to lenders who originate those home loans.

Since the Congress authorized VA to guarantee mortgages in 1944, the program has backed more than 25 million loans, including more than 1.2 million mortgages with a combined loan balance of $375 billion in 2020. In the Congressional Budget Office’s July 2021 baseline, VA is projected to guarantee $268 billion in mortgages in fiscal year 2022.

How Does VA Support Mortgages for Veterans and Other Eligible Borrowers?

To be eligible for VA’s mortgage guarantee program, a borrower generally must meet military service and discharge conditions. Many exceptions exist: For example, certain surviving spouses or service members who were discharged because of a service-connected disability are also eligible.1

Unlike guarantees offered by the Federal Housing Administration (FHA) on single-family mortgages, VA-backed guarantees leave originating lenders (also known as originators) with some risk of loss if borrowers do not repay their mortgages in full. That risk, as a share of the original balance of the mortgage, increases with the mortgage amount.

Although VA’s guarantee is considered a benefit of military service, not all mortgage applications from eligible veterans are approved. Borrowers must have satisfactory credit profiles and an income sufficient to meet their expected financial obligations after the mortgage documents are signed.

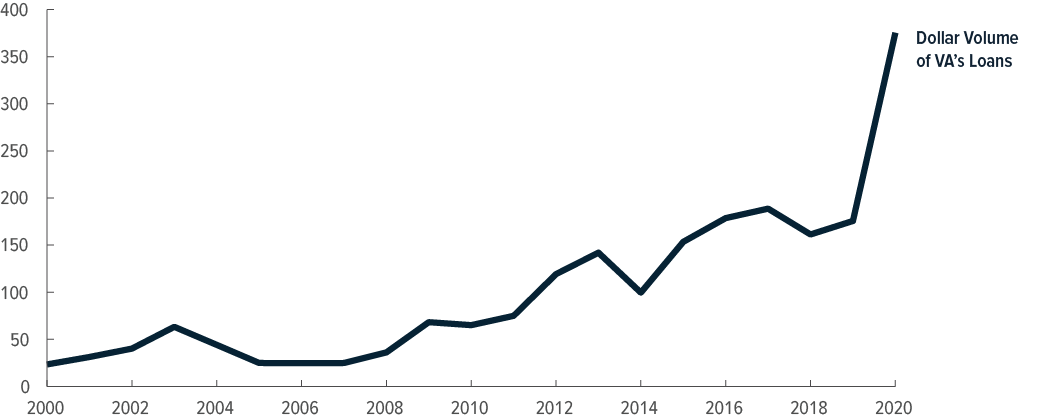

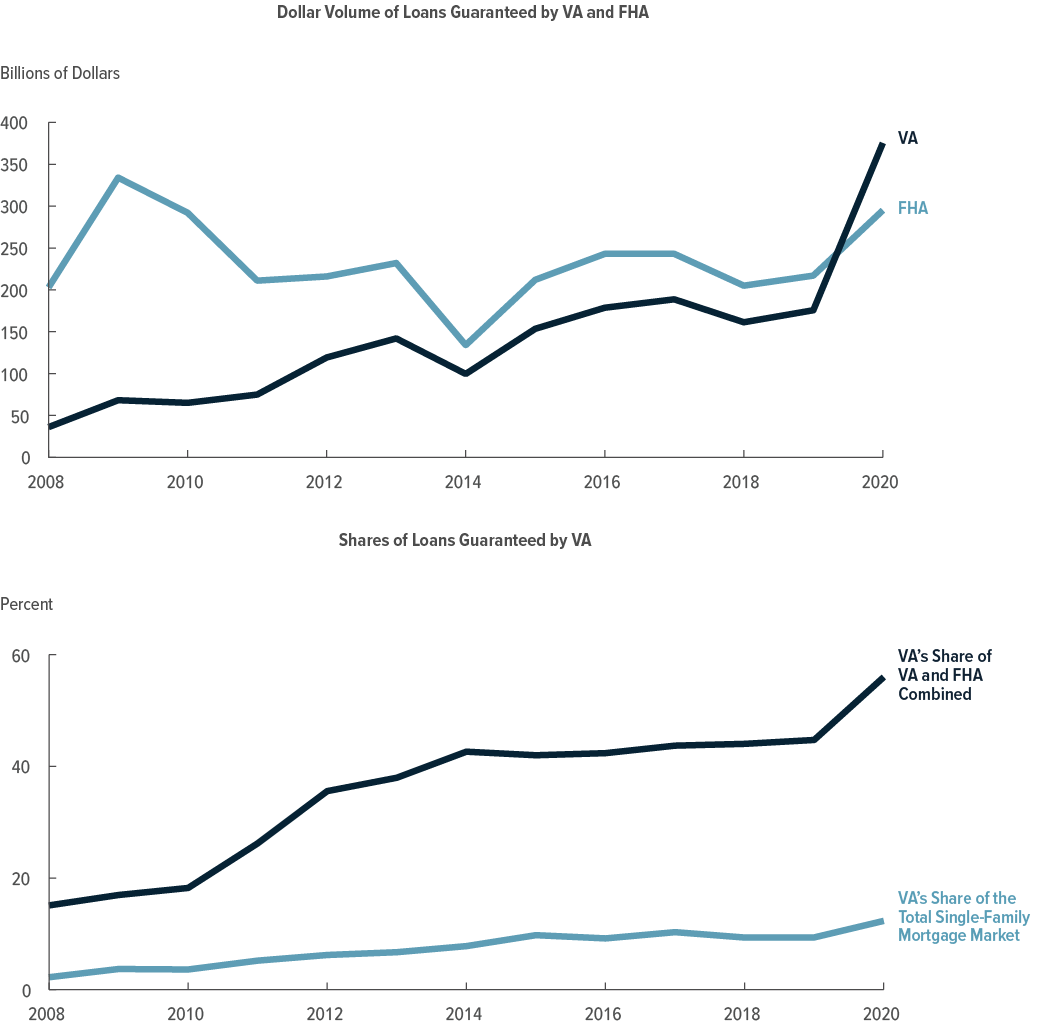

The dollar volume of VA’s guarantees increased from $23 billion in 2000 to $63 billion in 2003 (resulting from a sharp increase in refinancing) and then declined through 2007 (see Figure 1). Since the financial crisis of the late 2000s, VA’s guarantees have generally increased both in dollar volume and as a share of total federal loan guarantees made by both VA and FHA (see Figure 2). Fiscal year 2020 was a record year for VA with guarantees totaling more than $375 billion. That increase was attributable, in part, to the low interest rates put in place by the Federal Reserve in an effort to lessen the economic effects of the 2020–2021 coronavirus pandemic in the United States.

Figure 1.

Dollar Volume of Loans Guaranteed by VA

Billions of Dollars

Data sources: Department of Veterans Affairs, Veterans Benefits Administration Reports, Annual Benefits Report Archive (accessed August 6, 2021), www.benefits.va.gov/REPORTS/abr/archive.asp, and VBA Annual Benefits Report, Fiscal Year 2020 (updated June 2021), www.benefits.va.gov/REPORTS/abr/. See www.cbo.gov/publication/57024#data.

VA = Department of Veterans Affairs.

Figure 2.

Dollar Volume and Shares of Loans Guaranteed by VA and FHA

Data sources: Department of Veterans Affairs, Veterans Benefits Administration Reports, Annual Benefits Report Archive (accessed August 6, 2021), www.benefits.va.gov/REPORTS/abr/archive.asp, and VBA Annual Benefits Report, Fiscal Year 2020 (updated June 2021), www.benefits.va.gov/REPORTS/abr/; Department of Housing and Urban Development, FHA-Insured Single-Family Mortgage Market Share Report, 2020—Quarter 4 (accessed June 14, 2021), https://go.usa.gov/x7evx. See www.cbo.gov/publication/57024#data.

FHA = Federal Housing Administration; VA = Department of Veterans Affairs.

What Are the Federal Budgetary Costs of VA’s Mortgage Guarantees?

VA’s mortgage guarantee program covers a share of the shortfall between the outstanding balance of a mortgage and the funds VA recovers when the mortgage terminates through a borrower’s default. (The originator is responsible for the remainder of that shortfall.) Those guarantees cost the federal government because the costs are only partly offset by the funding fee that VA charges many borrowers for its guarantee.

Using the accrual-based accounting approach prescribed by the Federal Credit Reform Act of 1990 (FCRA), CBO projects that those guarantees will result in a federal budgetary cost of approximately $2.8 billion—yielding a subsidy rate of +1.1 percent.2 Using the fair-value approach—an alternative method that more fully accounts for the cost of the risk that the government takes when it guarantees loans—CBO projects a budgetary cost of $9.7 billion and a subsidy rate of +3.6 percent for guarantees issued in fiscal year 2022.

Subsidy estimates are sensitive to factors such as interest rates and the growth rate and volatility of home prices, which in this analysis are based on CBO’s macroeconomic forecast. Those estimates are also sensitive to estimates of the types of mortgages guaranteed by VA. CBO’s estimates of the subsidy rate for 2022 reflect the average across the range of potential outcomes that are attributable to those factors.

CBO’s estimate of the FCRA subsidy rate for 2022 is higher than the Administration’s estimate of -0.08 percent largely because CBO projects more cumulative lifetime defaults. That difference in defaults is the result of differences in CBO’s and the Administration’s modeling approaches.

How Do the Costs of VA’s Program Compare With Those of Other Federal Mortgage Guarantee Programs?

VA’s loan guarantees differ in many ways from those provided by FHA and two government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac. Those differences result in differences in budgetary costs. By CBO’s estimate, VA’s single-family mortgage guarantee program is the only one with a positive FCRA subsidy rate—+1.1 percent. By contrast, FHA’s guarantees are estimated to have a subsidy rate of -3.2 percent, and the GSEs’ guarantees are estimated to have a subsidy rate of -2.3 percent.3 Lower projected fees for VA’s mortgage guarantee program are the primary driver of that difference.

Description of VA’s Mortgage Guarantee Program

The end of World War II created the need to reintegrate nearly 16 million U.S. veterans into civilian society and the economy.4 For example, some service members returning from military service found it difficult to transition from the structured environment that the military provided—overseeing everything from employment and housing to health care. Seeking to avoid some of the difficulties encountered by veterans of World War I, lawmakers enacted the Servicemen’s Readjustment Act of 1944—commonly known as the GI Bill—to assist veterans in their readjustment to civilian life.5

An important element of that adjustment was the ability of veterans and their families to find and afford adequate housing. In response, the GI Bill included a provision for the Veterans Administration (now called the Department of Veterans Affairs) to guarantee mortgages for certain veterans for the purchase or construction of homes and business properties or for the purchase of farms. That guarantee program—which is one of the main components of the original GI Bill still in effect today—helped finance nearly one-fifth of all single-family homes constructed between World War II and 1966.6

Since the inception of the mortgage guarantee program in 1944, the Congress has continued to expand VA’s role and has created additional programs to support the housing needs of service members, veterans, and their families. Those programs provide that support in a variety of ways, including the following: direct mortgages for eligible Native American veterans and their spouses, direct mortgages for veterans and nonveterans for the purchase of homes acquired by VA through foreclosure, and grants to veterans with certain service-connected disabilities to help them build or modify their homes.

Although those programs are important components of VA’s support for veterans’ housing, the focus of this report is on VA’s mortgage guarantee program because it is much larger and has grown much faster than other VA programs that support veterans’ housing. For example, in 2000, VA guaranteed nearly 200,000 mortgages while providing fewer than 600 direct mortgages and housing grants (to Native American veterans and to veterans with a service-connected disability, respectively).7 By 2020, the number of mortgage guarantees had increased to more than 1.2 million, whereas direct mortgages to Native American veterans and housing grants for disabled veterans together served only about 2,100 participants.8

Borrowers’ Service Eligibility and Entitlement

Unlike guarantee programs administered by FHA, Fannie Mae, and Freddie Mac—which are available to almost any borrower who meets their underwriting criteria and makes a down payment on the home that is used as collateral for the guaranteed mortgage—borrowers using VA-backed mortgages qualify for that benefit primarily on the basis of their military service. However, because VA provides only a partial guarantee, borrowers often need to meet an originator’s credit and income requirements to get a VA-guaranteed mortgage.

To be eligible for a VA loan guarantee, a borrower generally must meet length-of-service requirements or have a discharge or release from active duty under honorable conditions. Many exceptions exist, including those granting eligibility to certain surviving spouses, members of the reserves or National Guard, or service members who were discharged because of a service-connected disability before reaching the required length-of-service threshold.9

The amount of the guarantee liability that VA will assume for eligible borrowers—referred to as the borrower’s entitlement—is limited. Specifically, the borrower’s entitlement ($36,000 on loans of up to $144,000) is a lifetime limit and is reduced by the amount used on previous mortgages.10 Entitlement that has been used before can be restored, however, once the previous mortgage is repaid or other restoration conditions are met.

Borrowers obtain a VA-guaranteed mortgage through a private originator once they have received a certificate of eligibility from VA. Although many veterans would be eligible for a mortgage not guaranteed by VA, a VA guarantee might encourage the originator to offer borrowers a lower interest rate than the one that might be available otherwise. In addition, eligibility provides a number of benefits to borrowers that are not available through other mortgage programs. Those benefits include different underwriting and down-payment requirements (discussed below), caps on fees charged by the originator, and assistance for borrowers who might encounter difficulties that affect their ability to repay their mortgage.

Amount and Structure of the Guarantees

Unlike guarantees offered by FHA on single-family mortgages, VA-backed guarantees leave originators—or issuers of securities backed by VA-guaranteed mortgages—with some risk of loss if borrowers do not repay their mortgages in full. (For a description of such securities, see the section of the report titled “The Role of Ginnie Mae.”) The amount of VA’s guarantee to an originator or issuer is related to the mortgage amount. For mortgages of less than $45,000, VA will guarantee 50 percent of that amount to the originator or issuer. The amount guaranteed by VA to eligible borrowers with their full entitlement is $22,500 for mortgages with an original balance that is between $45,000 and $56,250, which means that VA’s guarantee decreases from 50 percent of the original balance to 40 percent as the balance increases in that range. For mortgages with an original balance that is between $56,250 and $144,000, VA’s guarantee is 40 percent of the mortgage amount or $36,000, whichever is less. For mortgages with an original balance that is greater than $144,000, VA’s guarantee is 25 percent of the balance.11

For example, if a borrower has a VA-guaranteed mortgage with an original balance of $200,000, VA will compensate the originator or issuer for a loss of up to $50,000. (That loss is defined as the difference between the loan balance at the time of default and the funds received from the borrower or from the sale of the home.) If that borrower defaults when the outstanding balance is still $200,000 and the net proceeds from a foreclosure sale are $150,000—generating a $50,000 loss—the originator or issuer will be compensated by VA for the $50,000 shortfall. If, however, proceeds from the sale are $100,000, VA will pay the originator or issuer $50,000 (25 percent of the $200,000 outstanding balance), and the originator or issuer will incur a loss of $50,000.

Underwriting Criteria

Although VA’s guarantee is considered a benefit of military service, not all mortgage applications from eligible veterans are approved. Borrowers must have satisfactory credit profiles and income sufficient to meet their expected financial obligations after the mortgage is closed.

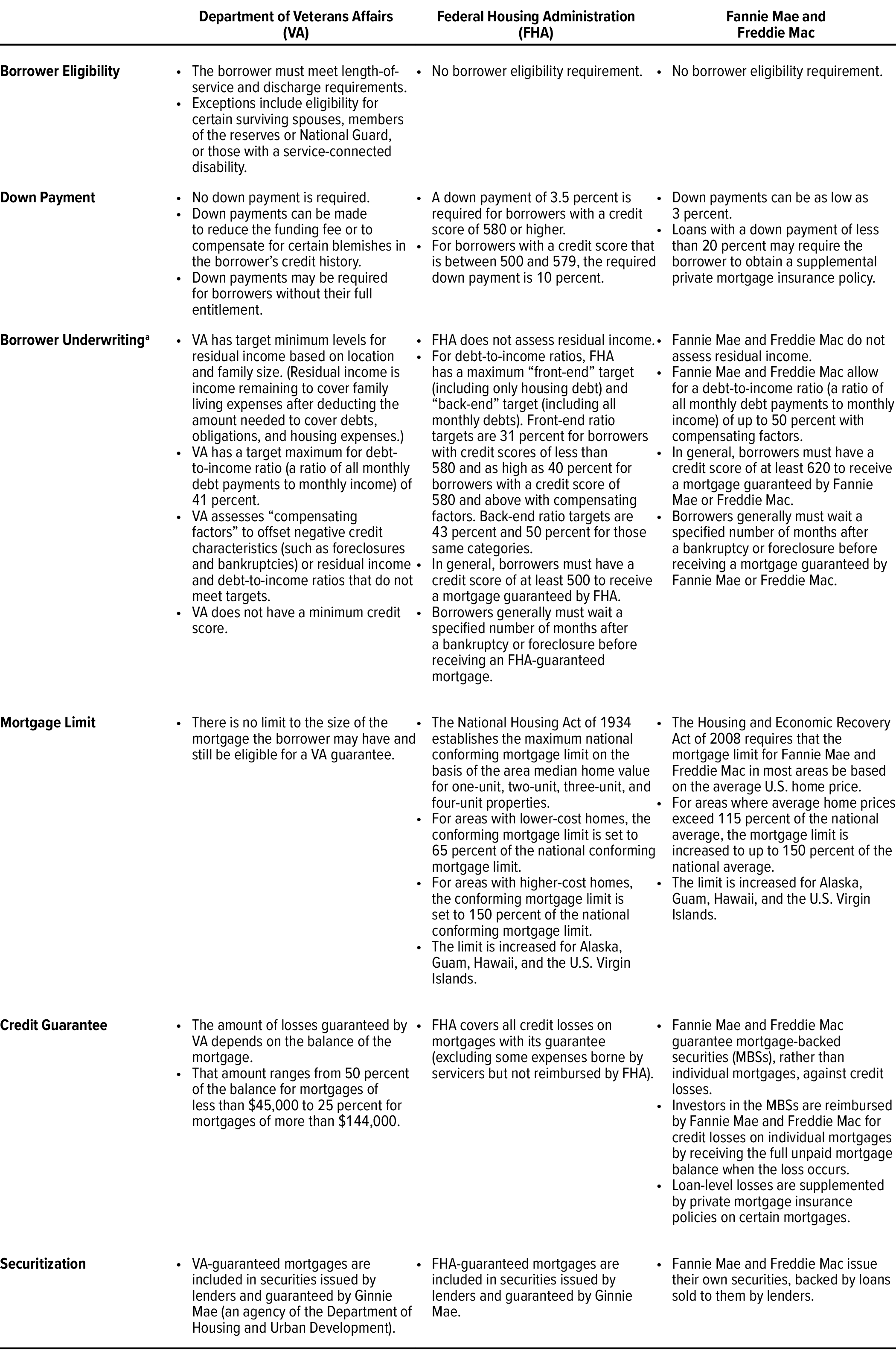

Compared with guarantees offered by FHA, Fannie Mae, and Freddie Mac, VA does not have as many underwriting restrictions based on the borrower’s credit profile. (For a comparison of loans guaranteed by VA, FHA, and Fannie Mae and Freddie Mac, see Table 1.) VA does, however, require that originators review the borrower’s credit report to ensure that the borrower’s history of repayment of other obligations indicates that he or she is likely to repay a VA-guaranteed mortgage.12 Adverse credit events—such as bankruptcy or foreclosure—do not disqualify a borrower from receiving a VA-guaranteed mortgage but do require the originator to perform an in-depth analysis of the circumstances underlying those events.

Table 1.

Comparing Loans Guaranteed by the Department of Veterans Affairs, the Federal Housing Administration, and Fannie Mae and Freddie Mac

Data source: Congressional Budget Office.

a. Although target maximum debt-to-income ratios for VA and FHA are lower than the absolute maximums for Fannie Mae and Freddie Mac (government-sponsored enterprises, or GSEs), mean values tend to be higher for VA and FHA mortgages. For example, see Ginnie Mae, Global Market Analysis Report (May 2020), p. 29, https://go.usa.gov/xFNnH.

Originators must also evaluate and verify a borrower’s income to ensure that it is stable, reliable, and sufficient to meet anticipated expenses. A unique element of the assessment of borrowers’ income for a VA-guaranteed loan is the calculation of “residual income,” which is income remaining to cover a family’s living expenses after deducting the amount needed to cover debts, obligations (such as child support), and housing expenses. VA establishes guidelines for minimum residual income based on a family’s size and location. Similar to assessments of a borrower’s credit, residual income below the minimum threshold does not trigger an automatic rejection of a borrower’s mortgage application.

Another difference between VA’s program and other government-guaranteed mortgage programs is that borrowers are not generally required to make a down payment or obtain private mortgage insurance. The only requirement for a VA-guaranteed mortgage is that the borrower have sufficient funds to cover any down payment required by VA or the originator and any closing costs not financed in the mortgage amount.13

Many borrowers must pay VA an up-front funding fee to obtain a guaranteed mortgage. That fee (which can be financed in the mortgage amount) varies on the basis of a number of factors, including the amount of the down payment, the mortgage type (for purchasing a home or the refinancing of an existing mortgage), and whether the borrower has used VA’s guarantee in the past. In 2021, that fee ranged from 0.5 percent to 3.6 percent of the loan amount. That year, approximately one-half of borrowers—specifically, those receiving compensation for a service-related disability or spouses of veterans who died in service—were exempt from the funding fee.

Borrowers are charged interest on the loan, at a rate set primarily by the originator, and pay a variety of costs—such as appraisal fees, title fees, credit report fees, and state and local taxes—at closing.

VA’s Role After the Guarantee Is Made

Once the loan has closed, VA continues to work with the servicer of the mortgage to monitor the borrower’s repayment, particularly borrowers who have missed a scheduled monthly payment. Like FHA and other guarantors, VA has developed a number of options that servicers may offer to help delinquent borrowers avoid foreclosure, including modifying the terms of the mortgage to help make the payment more affordable or offering alternatives to foreclosure such as short sales (whereby the borrower arranges for the sale of the home at a price that is lower than the outstanding balance of the mortgage) and “deeds-in-lieu” (whereby the borrower cedes ownership of the home to the owner of the mortgage in exchange for being released from the mortgage obligation).

Dollar Volume of Loans

The dollar volume of VA guarantees increased from $23 billion in 2000 to $63 billion in 2003 (resulting from a sharp increase in refinancing) and then declined through 2007 (see Figure 1). Since the financial crisis of the late 2000s, VA’s guarantees have increased both in dollar volume and as a share of total guarantees made by VA and FHA combined. In 2008, VA guaranteed $36 billion in loans—about 2 percent of the total single-family mortgage market and 15 percent of all guarantees provided by VA and FHA. By 2020, the dollar volume of VA guarantees rose to $375 billion, or nearly 12 percent of the total market and 49 percent of combined VA and FHA guarantees.14

The growth in the dollar volume of VA’s guarantees may have resulted from a number of factors, including the stricter underwriting requirements adopted by originators as a result of the housing crisis of the late 2000s and greater use by borrowers of refinancing options through VA. For example, in 2008, 21 percent of VA-guaranteed mortgages were used to refinance an existing mortgage—much lower than the 53 percent share for the total mortgage market. By 2015, however, refinancing transactions as a share of VA’s guarantees exceeded the percentage for the broader market. In 2019, 38 percent of mortgages guaranteed by VA were for refinancing, 7 percentage points higher than the 31 percent share in the total market. Since 2016, both VA and Ginnie Mae, an agency of the Department of Housing and Urban Development, have made changes to curb transactions involving the refinancing of mortgages currently guaranteed by VA into new VA-guaranteed loans—particularly those transactions that do not provide a tangible benefit to the borrower.15 CBO’s estimate of the dollar volume and cost of the program in its baseline reflects those changes.

As is the case with other mortgage programs, borrowers’ use of VA-guaranteed mortgages—either to purchase a home or refinance an existing mortgage—is driven by market interest rates. In periods of low or falling interest rates, a larger share of VA-guaranteed mortgages is used to refinance existing mortgages. For example, nearly 70 percent of VA-guaranteed mortgages were defined as “interest rate reduction” mortgages in 2003.16 By 2019, the share of such mortgages had dropped to 15 percent. By contrast, 62 percent of mortgages were used to purchase a home and 23 percent were used to extract equity from the home through refinancing or to refinance a mortgage not currently guaranteed by VA.17 Of the borrowers purchasing a home with a guarantee made in 2019, 42 percent were classified as first-time homebuyers and 80 percent made no down payment to purchase their home.

The Role of Ginnie Mae

With traditional mortgages, originators raise funds to make new mortgages by selling the mortgages they originate, often to securitizers such as Fannie Mae and Freddie Mac. Those GSEs’ mission is to promote access to mortgages by providing a stable flow of funding for such loans.18 Securitizers pool those mortgages to create mortgage-backed securities (MBSs), which they sell to investors with a guarantee against most losses from defaults on the underlying mortgages.

VA-backed mortgages are also used to create securities, which are guaranteed by Ginnie Mae. Ginnie Mae guarantees that investors who buy MBSs with VA mortgages (as well as loans guaranteed by FHA and the Rural Housing Service) will receive timely payment of principal and interest on the securities, providing a backup to the guarantee of the underlying mortgages provided by VA and the issuing lender (or issuer). In 2020, Ginnie Mae granted new guarantees of MBSs with a principal balance of $749 billion, of which nearly 44 percent (or approximately $330 billion) were backed by loans with a VA guarantee.19

Those securities help issuers fund VA-backed mortgages in the capital markets at a lower cost than using alternatives such as retaining ownership of the mortgages or selling the mortgages individually. In addition to increasing liquidity and reducing costs, Ginnie Mae’s securitization program is projected to generate budgetary savings of about $2.2 billion in 2022 because the fees that Ginnie Mae charges for its guarantees slightly exceed the costs of those guarantees when measured according to FCRA.20

The Budgetary Costs of VA’s Mortgage Guarantees

VA’s mortgage guarantee program generates budgetary costs for the federal government because of the structure of the guarantee, which requires the department to cover a share of the shortfall between the outstanding balance of a mortgage and the funds received from the borrower when the mortgage terminates.21 (The originator or issuer covers the remainder of that shortfall.) Those costs are partly offset by the funding fee that VA charges many borrowers for its guarantee.

In its July 2021 baseline budget projections, CBO estimates that VA will guarantee $268 billion in new mortgages in fiscal year 2022. Using the accrual accounting approach specified by FCRA, CBO projects that VA-guaranteed mortgages will increase the federal budget deficit by about $2.8 billion in 2022. (FCRA requires that the financial impact of VA’s guarantees, like that of other federal credit programs, be recorded in the federal budget on a present-value basis.)22 There will be a subsidy cost for the cohort of new mortgages guaranteed in 2022 because the present value of projected cash outflows from VA is greater than the present value of the payments that VA is projected to collect over the lifetime of those mortgages.

Although FCRA estimates are used in the federal budget for most credit programs, CBO often prepares fair-value estimates as well to provide a more comprehensive picture of programs’ long-term costs.23 Unlike FCRA estimates of the costs of federal mortgage guarantees, fair-value estimates account for the market value of the government’s obligations and reflect the cost of those obligations’ risks for taxpayers and beneficiaries of government programs. The main difference between FCRA and fair-value measures involves their treatment of market risk. Much of the risk associated with financial investments can be avoided by having a diverse portfolio; however, market risk represents the component of financial risk that remains even after a portfolio has been diversified as much as possible. It results from shifts in macroeconomic conditions, such as productivity and employment, and from changes in expectations about future macroeconomic conditions.24

On a fair-value basis, the mortgages that VA is projected to guarantee in 2022 will increase the federal budget deficit by $9.7 billion, CBO estimates.

Comparing the Budgetary Costs of VA’s Mortgage Guarantee Program With the Costs of Other Federal Mortgage Guarantee Programs

The loans guaranteed by VA differ in many ways from those guaranteed by FHA and the GSEs. Those differences result in differences in loan performance and in the budgetary costs associated with each program.

Defaults

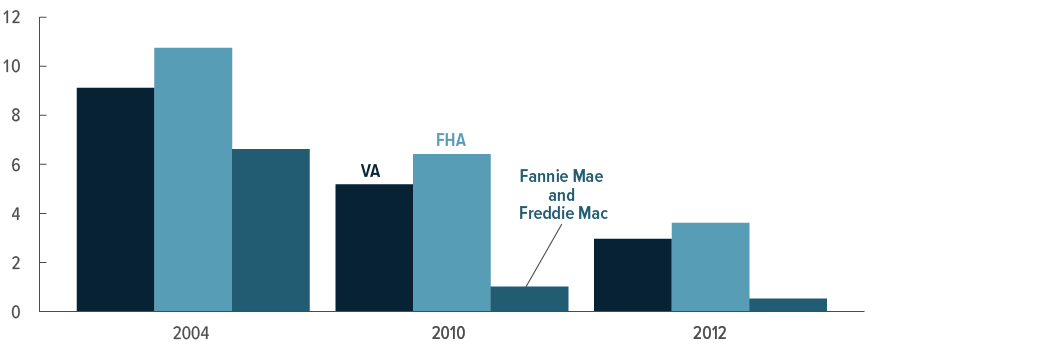

Historically, VA’s loans have had lower average default rates than loans guaranteed by FHA and higher default rates than those guaranteed by the GSEs. Default rates for all guarantors tend to vary over time, depending on the economic climate. For example, as of 2020, the rate of cumulative lifetime defaults for loans guaranteed in 2004 was 9.1 percent for VA, 10.8 percent for FHA, and 6.6 percent for the GSEs (see Figure 3). For loans guaranteed in 2012, the rate of cumulative lifetime defaults as of 2020 was 3.0 percent for VA, 3.6 percent for FHA, and 0.5 percent for the GSEs. Those relative differences for the 2012 guarantees persist across almost all credit scores—with the exception of loans issued to borrowers with very low credit scores (see Figure 4). Researchers and industry participants have given several explanations for the differences, particularly with respect to FHA, including VA’s partial guarantee (which leaves lenders with a stake in the borrower’s performance), its better property-valuation screening, its use of residual income, and its more rigorous foreclosure prevention.25

Figure 3.

Cumulative Lifetime Defaults for Loans Guaranteed in 2004, 2010, and 2012

Percent

Data source: Congressional Budget Office, using data from the Federal Housing Finance Agency’s National Mortgage Database, https://go.usa.gov/x7eeB. See www.cbo.gov/publication/57024#data.

Data for cumulative lifetime defaults for loans guaranteed in 2004, 2010, and 2012 are as of 2020.

FHA = Federal Housing Administration; VA = Department of Veterans Affairs.

Figure 4.

Cumulative Lifetime Defaults for Loans Guaranteed in 2012, by Credit Score

Percent

Data source: Congressional Budget Office, using data from the Federal Housing Finance Agency’s National Mortgage Database, https://go.usa.gov/x7eeB. See www.cbo.gov/publication/57024#data.

FHA = Federal Housing Administration; VA = Department of Veterans Affairs.

By CBO’s estimate, the projected cumulative lifetime default rate for loans guaranteed by VA in 2022 is 5.3 percent, below the 8.5 percent that CBO estimates for FHA. For VA, the projected rate of default on mortgages for home purchases is higher than the rate for mortgages used to refinance an existing obligation; for FHA, the opposite is true. For guarantees provided in 2022, the expected cumulative lifetime default rates of mortgages for home purchases (which represent approximately 71 percent of VA’s expected guarantees and 67 percent of FHA’s expected guarantees) are 5.8 percent for VA and 8.0 percent for FHA. For mortgages used to refinance an existing obligation, the expected cumulative lifetime default rate of VA guarantees is also lower than that for FHA—4.0 percent and 9.4 percent, respectively.

The projected cumulative lifetime default rate on mortgages guaranteed by VA in 2022 is higher than that on loans guaranteed by the GSEs during that year—5.3 percent for VA and 1.6 percent for the GSEs. That can be attributed to the fact that a larger share of borrowers have VA loans with high loan-to-value (LTV) ratios at origination and low credit scores. The projected average LTV of VA-guaranteed loans is 95 percent, with 71 percent of those loans having an LTV that is greater than 95 percent. For the GSEs, the projected average original LTV is 78 percent, with only 3 percent of those loans having an LTV that is greater than 95 percent. Loans with higher LTVs at origination have a greater likelihood of negative equity—wherein the loan balance is greater than the current value of the home—which is a strong predictor of default. The projected average credit score for VA’s 2022 guarantees is 715, with 32 percent of loan volume attributed to borrowers having a score of 680 or below. That is lower than the average credit score expected for GSE guarantees—733, with 9 percent of loans going to borrowers who have a credit score of 680 or below, CBO estimates.

Subsidy Rates

The subsidy rate is calculated as the difference between the present value of losses from defaults (net of recoveries) that are expected to occur and the fees that are expected to be collected on those guarantees over their lifetime, expressed as a percentage of the original unpaid principal balance of the loan. In its July 2021 baseline, CBO estimates that, on a FCRA basis, the $268 billion in new mortgage guarantees that VA is projected to issue in 2022 have a subsidy rate of +1.1 percent (and budgetary costs of about $2.8 billion); that is because the present value of losses from defaults (net of recoveries) is projected to exceed the present value of fees.

To estimate the subsidy cost of VA’s mortgage guarantees under FCRA, the cash flows of the program are discounted to the date the loans are disbursed, using an interest rate for each year of the cash flows that corresponds to the interest rate on Treasury securities of comparable maturity. For example, the projected yield on Treasury securities maturing in two years is used to discount cash flows two years from the disbursement date, a three-year Treasury rate is used for cash flows three years from disbursement, and so on.

In addition to FCRA estimates, CBO routinely provides fair-value estimates of mortgage guarantees to lawmakers on a supplemental basis. On a fair-value basis, the new guarantees that VA is projected to issue in 2022 are estimated to result in a subsidy rate of +3.6 percent (and budgetary costs of about $9.7 billion). The difference between the FCRA and fair-value estimates occurs because participants in financial markets would assign a higher cost than the FCRA measure would to losses on VA’s guarantees. The reason is that VA’s losses tend to be larger when overall economic conditions are weak. In financial markets, transactions in which losses fluctuate with overall economic conditions are said to have market risk. By including the cost of market risk in the program’s costs, fair-value estimates more closely match how the private sector evaluates the costs of financial transactions with such risks. Investors would generally demand more compensation to bear losses in weak economic conditions than in strong economic conditions. When the federal government takes on market risk in its programs, the cost of that risk is effectively passed on to taxpayers and beneficiaries of federal programs because they ultimately bear the consequences of the government’s financial losses.

When compared with FHA’s FCRA subsidy rate of -3.2 percent and the GSEs’ rate of -2.3 percent, VA’s is the only single-family mortgage guarantee program of the three with a positive FCRA subsidy rate (see Table 2). A positive FCRA rate represents the average subsidy that is granted to borrowers by the guarantor.

Table 2.

Subsidy Rate Components and Estimates of Lifetime Default Rates for Mortgages Guaranteed by VA, FHA, and the GSEs in 2022 Under Two Accounting Approaches

Percent

Data source: Congressional Budget Office. See www.cbo.gov/publication/57024#data.

The subsidy rate is calculated as the difference between the present value of losses from defaults (net of recoveries) that are expected to occur and the fees that are expected to be collected on those guarantees over their lifetime, expressed as a percentage of the original unpaid principal balance of the loan.

The costs of most credit programs are currently accounted for in the federal budget using procedures prescribed by the Federal Credit Reform Act of 1990. FCRA specifies that an accrual-based accounting method be used to record those costs. (Accrual measures summarize in a single number the anticipated net financial effects at a specific time of a commitment that will affect federal cash flows many years into the future.)

CBO often prepares fair-value estimates as well to provide a more comprehensive picture of programs’ long-term costs. Unlike FCRA estimates of the costs of federal mortgage guarantees, fair-value estimates account for the market value of the government’s obligations and reflect the cost of those obligations’ risks for taxpayers and beneficiaries of government programs.

VA = Department of Veterans Affairs; FCRA = Federal Credit Reform Act of 1990; FHA = Federal Housing Administration; GSEs = government-sponsored enterprises.

a. FHA is a part of the Department of Housing and Urban Development.

b. The GSEs are Fannie Mae and Freddie Mac. In its baseline budget projections for the coming 10 years, CBO accounts for the GSEs’ operations as though they are being conducted by a federal agency. CBO measures the cost of their mortgage guarantees on a fair-value basis. The FCRA estimates of the budgetary costs of loan guarantees made by Fannie Mae and Freddie Mac provided in this report are solely for the purpose of comparison with the estimated costs of VA’s and FHA’s guarantees.

Lower projected fees for the VA mortgage guarantee program are the primary driver of that difference. VA has an average fee rate—that is, the component of the subsidy rate representing the present value of collected fees—of -0.8 percent, and FHA and the GSEs have average fee rates of -7.5 percent and -2.8 percent, respectively. VA’s average fee rate is lower in part because a significant share of borrowers are exempt from that fee. VA’s fees are also lower because of the structure of the funding fee—which includes only an up-front fee for borrowers who do not receive a waiver and no ongoing premium for any borrowers. Both FHA and the GSEs charge nearly all borrowers a combination of up-front fees and ongoing premiums.

The programs’ subsidy rates also differ because the programs have different rates of default. VA’s cumulative lifetime default rate of 5.3 percent translates into net default losses of +1.9 percent. FHA’s projected cumulative lifetime defaults of 8.5 percent result in net default losses of +4.4 percent, and the GSEs’ 1.6 percent cumulative defaults generate +0.5 percent in net default losses. Net losses from defaults (as a percentage of the original mortgage amount) are lower than cumulative lifetime defaults (also as a percentage of the original mortgage amount) for all programs for several reasons:

- First, net losses from defaults are a present-value measure, meaning that the losses associated with defaults that occur in future years are less costly than losses from defaults occurring today.

- Second, losses from defaults are partly mitigated by recoveries—such as those stemming from the proceeds received when a foreclosed home is sold.

- Third, net losses from defaults as a component of the subsidy rate reflect the share of total losses borne by other parties. For VA, with its partial guarantee, those losses are shared with the originating financial institution. For the GSEs, those losses are shared with private mortgage insurers. For FHA, which provides a full credit guarantee, no risk is shared.

On a fair-value basis, VA also has the highest subsidy rate at +3.6 percent, compared with +3.0 percent for FHA and +0.4 percent for the GSEs. However, VA has a smaller difference between FCRA and fair-value subsidy rates (+2.6 percent) than either FHA (+6.2 percent) or the GSEs (+2.7 percent). VA’s partial guarantee—which leaves catastrophic losses to the originator or issuer—reduces the effect of risk adjusting projected defaults under the fair-value approach. In addition, VA’s fee structure—which includes only up-front funding fees—reduces the effect of risk adjusting income from fees under the fair-value approach.

Comparing CBO’s Estimate of the Budgetary Costs of VA’s Mortgage Guarantee Program With the Administration’s Estimate

Subsidy rate estimates for VA’s mortgage guarantee program are included in the government’s annual Federal Credit Supplement, a document detailing the status of federal direct loans and loan guarantees that is released as a part of the Administration’s proposed budget.26 Those estimates are calculated according to the method specified by FCRA, consistent with the approach used for CBO’s estimates of the federal subsidy rate for the VA program. VA’s estimate of the program’s subsidy rate in the Federal Credit Supplement is -0.08 percent for 2022, which is based on losses from defaults (net of recoveries) of +0.67 percent and fee rates of -0.75 percent.

CBO’s estimate of the subsidy rate is higher than the one published by VA largely because CBO projects more cumulative lifetime defaults. Based on CBO’s review of VA’s model, the difference in defaults is the result of a difference in modeling approaches. In short, VA’s modeling approach generates an expected cumulative default rate for the 2022 guarantees that is similar to those experienced by loans guaranteed since the financial crisis of the late 2000s, a period (before the coronavirus pandemic) marked by rising home prices, stable interest rates, and low unemployment.

CBO’s projection of defaults reflects a longer period with more variability in economic conditions, which is consistent with its estimates for FHA and the GSEs.27 Although CBO’s projection for the amount of loans guaranteed in 2022 is based on recent guarantees, the performance of those loans is based on CBO’s macroeconomic forecast, which projects growth rates in housing prices that are based on more than just recent actual growth rates. For example, the index of home prices used in CBO’s projections (the House Price Index released by the Federal Housing Finance Agency) grew by 5.3 percent per year, on average, from 2012 to 2020. In CBO’s July 2021 baseline, that same index is projected to grow by an average annual rate of 3.7 percent over the 2022–2031 period.28

Sensitivity Analysis of CBO’s Estimates of Budgetary Costs

To estimate subsidy rates and budgetary costs of VA’s mortgage guarantee program, CBO uses a model that simulates the cash flows of those mortgages on the basis of various factors, such as the characteristics of borrowers who take out VA-guaranteed loans and the overall economic environment. The model uses a simulation of unemployment rates, home prices, and interest rates (drawing from 1,000 possible paths for those variables, which are centered on CBO’s baseline macroeconomic forecast). The cash flows for each path are weighted by the expected distribution across 50 borrower profiles that are based on LTV groups, credit-score groups, and loan type (purchase or refinancing). The weighted cash flows are then discounted back to the origination date using the appropriate discount rate. To calculate the subsidy rate, the sum of the discounted cash flows—which equals the subsidy cost per loan—is divided by the expected volume of mortgages projected to be guaranteed in 2022.

Effects of Changes to Interest Rates, Discount Rates, and Home Prices

The estimates of subsidy rates are sensitive to factors such as average interest rates, discount rates, and the growth rate and volatility of home prices; projections of those factors are based on CBO’s macroeconomic forecast. Those estimates are also sensitive to values for various aspects of VA’s guarantee program that are used in CBO’s model. CBO’s estimates of the subsidy rate reflect the average across the range of potential outcomes for those macroeconomic factors.

Interest Rates. The long-term interest rate used for CBO’s baseline subsidy estimate comes from the agency’s forecast of the rate on 10-year Treasury notes in 2022. That rate is used in CBO’s model to construct the borrower’s initial interest rate and to determine, on the basis of the difference between that initial interest rate and current market rates, if the borrower has an incentive to refinance.

Raising that market interest rate and the borrower’s initial interest rate by 1 percentage point would increase the estimated subsidy rate for VA in 2022 from +1.1 percent to +1.2 percent on a FCRA basis and from +3.6 percent to +4.0 percent on a fair-value basis because the higher interest rate would increase the borrowers’ monthly mortgage payments. Higher monthly payments increase the projected likelihood of default, raising the cost of the guarantee to VA. That increase would be partially offset because borrowers with higher initial interest rates are more likely to prepay their mortgages. Higher prepayment rates decrease defaults because fewer borrowers are left in the cohort of loans at risk of default, lowering the cost of the guarantee. Reducing the market interest rate and the borrower’s initial interest rate by 1 percentage point would decrease the estimated subsidy rate by similar amounts—to +0.9 percent on a FCRA basis and to +3.3 percent on a fair-value basis.

Discount Rates. Subsidy rates are also sensitive to the interest rate on Treasury securities used to discount cash flows underlying the subsidy calculation. Doubling the rate on Treasury securities of all maturities would reduce the estimated subsidy rate to +0.9 percent on a FCRA basis and to +2.9 percent on a fair-value basis. Subsidy rates would decline because higher discount rates reduce the present value of losses from defaults, net of recoveries, but have no effect on the present value of fees, which are collected at the time of a loan’s origination. Reducing the rate on Treasury securities of all maturities by 50 percent would increase the estimated subsidy rate to +1.2 percent on a FCRA basis and to +4.2 percent on a fair-value basis.

Home Prices. Estimated subsidy rates move in the opposite direction from changes in the growth rate of home prices. Higher growth in home prices drives down the subsidy rate on a VA guarantee, and lower growth in home prices drives that rate up. The forecast for the average national growth of home prices used in the CBO’s projections comes from the agency’s macroeconomic forecast.

Lowering the average growth rate of home prices nationwide by 1 percent in each year would increase VA’s projected subsidy rate from +1.1 percent to +1.4 percent under the FCRA approach and from +3.6 percent to +3.9 percent under the fair-value approach. Lower growth in home prices increases defaults and foreclosures and reduces the future value of homes when a default or a foreclosure occurs. Together, those effects would increase the estimated subsidy rate of a VA-guaranteed mortgage on both a FCRA and a fair-value basis. Conversely, raising the growth rate of home prices by 1 percent would decrease the subsidy rate to +0.8 percent under FCRA and to +3.4 percent on a fair-value basis.

Effects of Changes in Borrowers’ Characteristics

Estimates of federal subsidy rates and costs are also sensitive to projections of the characteristics of borrowers who are expected to take out a guaranteed loan in 2022. CBO’s projection for loans guaranteed in 2022 is based on recent guarantees. Over time, the characteristics of guarantees have changed as the program has evolved, the characteristics of borrowers receiving a guarantee have changed, and the mortgage market has shifted periodically to one dominated by refinancing during periods of low or falling interest rates.

To test the sensitivity of subsidy rates and budgetary costs to the uncertainty surrounding the characteristics of potential guarantees, CBO reran its model using the loans guaranteed by VA during each year between 2000 and 2019. As part of that process, CBO incorporated the assumption that each of those annual loan cohorts represented the loans that were projected to be guaranteed in 2022. Because funding fees charged to specific borrowers have varied over time, the analysis focused on the default component of the subsidy cost (which is equal to losses from defaults net of any recoveries). In CBO’s 2022 baseline, that default component of the subsidy cost equals +1.9 percent.

That exercise produced 20,000 scenarios for net losses from defaults—the product of 20 annual cohorts and 1,000 possible paths of interest rates and home prices for each cohort. The median value across those results was a net default loss of +1.7 percent, or 11 percent below the value used in the 2022 baseline. The results varied widely. For those scenarios with net default losses below the median, 25 percent were below +1.2 percent and 5 percent were below +0.8 percent. For those scenarios with net default losses above the median, 25 percent were above +2.4 percent and 5 percent were above +4.7 percent.

Greater variability in net losses from defaults occurs for specific years. The highest median result, which was +2.7 percent, was generated using the 2001 cohort; 5 percent of the scenarios that year had net default losses above +7.2 percent. That result was driven by the large share of loans used for home purchases in the 2001 cohort; those loans generally have higher net default losses than refinancing loans in VA’s guarantee program. The 2014 cohort produced the lowest results, with median net losses from default of about +1.2 percent and 5 percent of the scenarios above +3.1 percent.

1. A service-connected disability is a medical condition that develops or worsens during a service member’s time in the military.

2. Accrual measures summarize in a single number the anticipated net financial effects at a specific time of a commitment that will affect federal cash flows many years into the future. The subsidy rate measures the difference between the expected cost of a loan guarantee and any fees received by the guarantor as a percentage of the original unpaid principal balance. Programs with positive subsidy rates increase federal outlays, whereas programs with negative subsidy rates increase federal collections, thus decreasing outlays.

3. In CBO’s judgment, Fannie Mae and Freddie Mac are effectively part of the government. Hence, in its baseline budget projections for the coming 10 years, CBO accounts for the GSEs’ operations as though they are being conducted by a federal agency. CBO measures the cost of the GSEs’ mortgage guarantees on a fair-value basis by effectively using market prices for those guarantees (as described in the section titled “Comparing the Budgetary Costs of VA’s Mortgage Guarantee Program With the Costs of Other Federal Mortgage Guarantee Programs”). In this report, FCRA estimates of the budgetary costs of loan guarantees made by Fannie Mae and Freddie Mac are provided solely for the purpose of comparing the GSEs’ guarantees with those of VA and FHA.

4. See Department of Veterans Affairs, Born of Controversy: The GI Bill of Rights (accessed August 8, 2021), www.va.gov/opa/publications/celebrate/gi-bill.pdf (112 KB).

5. Public Law 78-346.

6. See Department of Veterans Affairs, “VA History” (updated May 27, 2021), www.va.gov/HISTORY/VA_History/Overview.asp.

7. See Department of Veterans Affairs, Veterans Benefits Administration Reports, Annual Benefits Report Archive (accessed August 6, 2021), www.benefits.va.gov/REPORTS/abr/archive.asp, and VBA Annual Benefits Report, Fiscal Year 2020 (updated June 2021), www.benefits.va.gov/REPORTS/abr/.

8. See Department of Veterans Affairs, VBA Annual Benefits Report, Fiscal Year 2020 (updated June 2021), www.benefits.va.gov/REPORTS/abr/.

9. See Department of Veterans Affairs, “Eligibility Requirements for VA Home Loan Programs” (accessed June 9, 2021), https://go.usa.gov/xFheM.

10. For loans over $144,000, VA will guarantee up to 25 percent of the loan amount.

11. As of 2020, the balance of the mortgage eligible for a 25 percent guarantee is no longer limited for borrowers with their full entitlement.

12. Because of the unique nature of VA’s underwriting requirements, originators either specialize in VA-guaranteed mortgages or they set up a specialized group within the company that focuses only on those mortgages.

13. For example, VA may require the borrower to make a down payment in the amount of the difference between the sales price of the home and the appraised value established by VA.

14. See Department of Housing and Urban Development, FHA-Insured Single-Family Mortgage Market Share Report, 2020—Quarter 4 (accessed June 14, 2021), https://go.usa.gov/x7evx.

15. See Laurie Goodman, Edward Golding, and Michael Neal, Fast Prepayments of VA Mortgages Are Increasing Costs to Veteran and FHA Mortgage Borrowers (Urban Institute, June 2019), https://tinyurl.com/y2pfrd33.

16. See Department of Veterans Affairs, Veterans Benefits Administration Reports, Annual Benefits Report Archive (accessed August 6, 2021), www.benefits.va.gov/REPORTS/abr/archive.asp, and VBA Annual Benefits Report, Fiscal Year 2020 (updated June 2021), www.benefits.va.gov/REPORTS/abr/.

17. Refinancings rose to nearly 66 percent of total VA guarantees in 2020, driven in part by the low interest rates resulting from the coronavirus pandemic in the United States.

18. For more details about Fannie Mae and Freddie Mac, see Congressional Budget Office, Fannie Mae, Freddie Mac, and the Federal Role in the Secondary Mortgage Market (December 2010), www.cbo.gov/publication/21992.

19. See Ginnie Mae, 2020 Report to Congress (January 2021), https://go.usa.gov/xFtmu.

20. See Congressional Budget Office, “Federal Programs That Guarantee Mortgages” (July 2021), www.cbo.gov/about/products/baseline-projections-selected-programs#5. Although CBO estimates the cost of Ginnie Mae’s guarantees, the agency does not calculate a separate budgetary cost for VA and FHA loans guaranteed by Ginnie Mae. The partial guarantee offered by VA (as compared with the full FHA guarantee) creates additional risk for Ginnie Mae because the issuer has to cover any losses not covered by VA.

21. Subsidy costs for VA’s loan guarantees are paid from mandatory appropriations. The program’s administrative expenses are covered by discretionary funds.

22. A present value is a single number that expresses a flow of income or payments in terms of an equivalent lump sum received or paid at a specified time. The present value depends on the rate of interest—the discount rate—that is used to translate future cash flows into current dollars.

23. See, for example, Congressional Budget Office, Estimates of the Cost of Federal Credit Programs in 2021 (April 2020), www.cbo.gov/publication/56285, and How CBO Produces Fair-Value Estimates of the Cost of Federal Credit Programs: A Primer (July 2018), www.cbo.gov/publication/53886.

24. For a discussion of the fair-value approach, see Congressional Budget Office, Measuring the Cost of Government Activities That Involve Financial Risk (March 2021), www.cbo.gov/publication/56778.

25. See Laurie Goodman, Ellen Seidman, and Jun Zhu, VA Loans Outperform FHA Loans. Why? And What Can We Learn? (Urban Institute, July 2014), https://tinyurl.com/y2o6mdqr.

26. See Office of Management and Budge, Budget of the U.S. Government, Fiscal Year 2022: Federal Credit Supplement (February 2021), www.whitehouse.gov/omb/supplemental-materials/.

27. CBO estimates defaults from VA-guaranteed mortgages using data obtained from the Federal Housing Finance Agency’s National Mortgage Database (see https://go.usa.gov/x7eeB). Because that database does not have complete information about losses from those defaults, CBO used its own model to forecast such losses. (That model is derived from data on FHA guarantees, with adjustments to reflect VA’s partial guarantee.) As a result, CBO used a definition of defaults for VA that is consistent with its modeling of FHA guarantees.

28. See Congressional Budget Office, “Budget and Economic Data: Historical Data and Economic Projections” (July 2021), www.cbo.gov/data/budget-economic-data#4.

About This Document

This report by the Congressional Budget Office was prepared at the request of the Chairman of the House Committee on the Budget. In keeping with CBO’s mandate to provide objective, impartial analysis, the report makes no recommendations.

Mitchell Remy wrote the report with guidance from Sebastien Gay. Elizabeth Bass, David Burk (formerly of CBO), Michael Falkenheim, Heidi Golding, Paul B. A. Holland, Edward G. Keating, David Newman, Jeffrey Perry, Delaney Smith (formerly of CBO), Natalie Tawil, and David Torregrosa provided useful comments on earlier drafts of the report.

Helpful comments were also provided by Michael Bright of the Structured Finance Association, Michael Fratantoni of the Mortgage Bankers Association, Laurie Goodman of the Urban Institute, and Theodore Tozer of the Milken Institute. (The assistance of external reviewers implies no responsibility for the final product, which rests solely with CBO.)

Mark Doms, Wendy Edelberg (formerly of CBO), Mark Hadley, Jeffrey Kling, and Robert Sunshine reviewed the report. Loretta Lettner was the editor, and R. L. Rebach and Jorge Salazar were the graphics editors. The report is available on CBO’s website (www.cbo.gov/publication/57024).

CBO seeks feedback to make its work as useful as possible. Please send any comments to communications@cbo.gov.

Phillip L. Swagel

Director

September 2021