Refundable Tax Credits

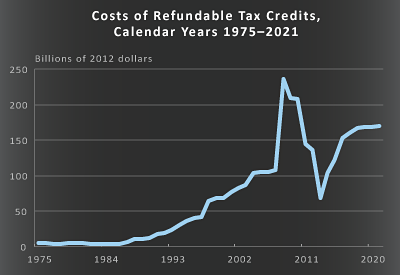

The number and cost of refundable tax credits have grown considerably since 1975. Federal costs (in 2013 dollars) peaked at $238 billion in 2008, but costs will fall to $149 billion in 2013 before reaching $213 billion in 2021.

Summary

The U.S. tax code contains many preferences that lower or eliminate the amount of taxes owed. Those preferences include deductions, exclusions, and tax credits, which can be either refundable or nonrefundable. Refundable tax credits differ from other preferences in a significant way: Whereas other preferences reduce the amount of taxes owed to the government, refundable credits can result in net payments from the government. Specifically, if the amount of a refundable tax credit exceeds a filer’s tax liability before that credit is applied, the government pays the excess to that person or business. In the federal budget, the portion of refundable credits that reduces the amount of taxes owed is counted as a reduction in revenues, and the portion that exceeds people’s tax liabilities is treated as an outlay; the total federal cost is the sum of those two components.

In 1975, the first refundable tax credit—the earned income tax credit (EITC)—took effect. Since then, the number and cost of credits have grown considerably. This report reviews the evolution and federal costs of refundable tax credits, their effects on the economy and the tax system, the administrative challenges in providing subsidies, and the transparency of such credits in the federal budget.

Total Costs of Refundable Credits Grew Considerably Between 1975 and 2010; Although Costs Will Decline Between 2010 and 2013, They Will Rise Again Thereafter

The number of credits peaked at 11 in 2010 before dropping to 6 in 2013. Their total costs reached a high of $238 billion in 2008. (The $238 billion and other annual costs discussed in this report are expressed in 2013 dollars.) In 2013, the costs will drop to $149 billion, CBO estimates, mostly for the EITC and the child tax credit. By 2018, three more credits will have expired, and the child tax credit and the EITC will have been scaled back (see figure below).

Those cutbacks in refundable tax credits will be more than offset, however, by new health-related subsidies provided through the tax system. Starting in 2014, a new refundable tax credit will be available to some people for the purchase of health insurance through newly created exchanges. The cost of that credit will be about $110 billion by 2021, CBO and the staff of the Joint Committee on Taxation project, bringing the total cost of refundable tax credits in that year to $213 billion—roughly the same as the costs in 2009 and 2010, even though the number of refundable tax credits will have fallen by more than half between 2010 and 2021.

The First Refundable Tax Credits Were Directly Tied to People’s Earnings, but Newer Credits Are Subsidizing Spending on Health Insurance and Higher Education

Not only have the number and costs of refundable tax credits grown over the years, but the nature of those credits has evolved. Eligibility for the first refundable tax credit—the EITC—was based primarily on the recipient’s earnings, adjusted gross income, and the number of children in his or her home. However, many of the newer refundable tax credits are not limited to people with earnings but are instead used to compensate people for expenditures on items such as health insurance and higher education.

The Growth of Refundable Credits Affects the Economy and the Tax System

Credits affect the allocation of resources by favoring certain activities or goods. Credits that decline in value as income rises prompt some people to work fewer hours. However, credits that increase as earnings rise, such as the EITC at certain income levels, provide an incentive for some people to work more. The EITC also draws people into the labor force by increasing their after-tax income. On balance, the latter effect appears to dominate.

In addition, the growth of refundable tax credits has contributed to a decline in average tax rates among households in the bottom 40 percent of the income distribution. That decline is most notable for individual income tax rates, which between 2007 and 2009 became increasingly negative for low-income households (that is, on average, those households received money back from the federal government instead of owing income taxes). Most of those households, however, pay federal payroll taxes.

Refundable tax credits also affect the administration of taxes. By adding more complicated rules, more tax forms, and more computations, the credits increase the costs incurred by taxpayers in complying with the tax code and by the government in administering those laws.

Subsidies Delivered Through the Tax System Could Alternatively Be Provided Through Spending Programs, but Administrative Considerations Are Important

Most refundable tax credits were created to meet social policy goals, such as providing income support for low-income households, expanding health insurance coverage, or increasing college enrollment. But those goals could instead be pursued through spending programs (such as the Supplemental Nutrition Assistance Program, the Temporary Assistance for Needy Families program, Medicaid, the Children’s Health Insurance Program, and the Pell Grant program).

The choice between using the tax system and relying on spending programs hinges largely on administrative considerations, such as the effectiveness in reaching the target population, timeliness, and the ability to ensure compliance with rules. Each of those considerations affects the costs incurred by the federal government and the burdens imposed on people who are eligible for benefits and on the third parties who might be asked to provide evidence of applicants’ eligibility.

Delivering assistance to low-income families using either approach has advantages and disadvantages. In some cases, it is simpler to distribute assistance to low-income workers through the tax system: Most of those workers already file tax returns to claim refunds of income taxes withheld during the year even if they do not owe any taxes, and they can generally claim a credit by attaching one more form to their return. By comparison, claiming assistance through spending programs can be more time-consuming and intrusive for beneficiaries, especially if they must take time off from work to apply for the benefit in person at a government agency. But spending programs can more easily reach people who do not have to file tax returns and who are already receiving certain benefits from other government agencies. In many instances, caseworkers attached to those programs assist claimants by determining eligibility for them.

The two approaches differ in other ways. Spending programs can be designed to provide assistance as the need arises, whereas people typically file tax returns only once a year, which makes it more challenging to provide timely assistance during the year. Overpayments are generally higher for refundable tax credits than for subsidies operated through spending programs, primarily because the Internal Revenue Service cannot verify that applicants meet all eligibility requirements before benefits are paid. However, additional verification steps raise the administrative and compliance costs of spending programs relative to those of the tax system.

The Full Costs of Refundable Credits Are Not Readily Visible in the Federal Budget

Some analysts have suggested that the scope of federal budgetary commitments is masked because as much as half of the cost of all refundable tax credits (as well as the full costs of other tax preferences) has been recorded as a reduction in revenues, thereby making the budget appear smaller. Only the outlay portion of each refundable tax credit is easily identified in the budget in a separate line item. The remaining costs are not presented individually; they are, instead, reflected in the total amount of revenues recorded. That presentation makes the readily identifiable budgetary costs of refundable tax credits appear smaller than the full costs of those credits. As a result, providing Congressional review and oversight is more difficult for the credits than for spending programs.

This report was prepared by Janet Holtzblatt of CBO’s Tax Analysis Division and Grant Driessen, formerly of CBO.